Personal Wealth Management / Economics

The Resiliency of US-China Trade Ties

Shrill rhetoric and tariffs haven’t upended the US-China trade relationship.

Our political analysis is intentionally nonpartisan. We favor no politician nor any party and assess developments solely for their market and economic impact.

China dominated financial headlines last week, especially on the regulatory front, which has drawn many investors’ focus. But if you can look past this, another story involving America and China is quietly emerging—one that undercuts the longstanding fear of a trade war upending global growth. Those concerns still lurk with the chilly relations between the two economic superpowers—see recent high-level talks to discuss “guardrails” for the US-China relationship—occasionally stirring fear anew. However, for all the damage the US-China trade spat was supposed to inflict, reality wasn’t as dire as projected. Trade relationships proved more durable than many feared.

Despite some post-election expectations of a more dovish tone towards China, President Joe Biden’s approach has looked a lot like former President Donald Trump’s. In early June, the Biden administration expanded on Trump’s executive order prohibiting Americans from investing in certain Chinese companies with Chinese military ties (perhaps most notably, Huawei). A couple weeks later, the administration banned the import of raw materials used in solar panels—a move tied to human rights concerns in Xinjiang. It then closed the month by opening trade talks with Taiwan—which Chinese views as a breakaway province—for the first time since 2016. The primary difference between the Trump and Biden administrations’ approaches: The latter has tried building a consensus among allies to pressure China on a range of geopolitical and sociological issues.

On the tariff front, the Biden administration hasn’t lifted any Trump-era duties. Upon her Senate confirmation in March, US Trade Representative Katherine Tai said the US wouldn’t do so right away. As she acknowledged: “No negotiator walks away from leverage, right?”[i] In our view, the status quo’s survival reinforces the importance of watching what politicians do, not what they say. We saw plenty of headlines claiming Biden’s presidency would break from Trump’s “protectionist” policy—but at least as it pertains to China, that hasn’t happened yet.

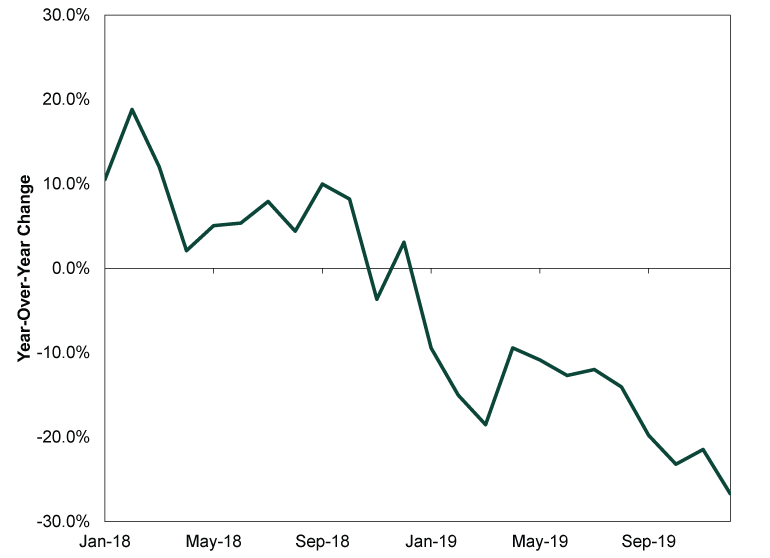

That said, however, that oft-feared protectionist policy wasn’t as economically damaging as feared. At first glance, the US-China trade tiff seems to have had an obvious negative impact on commerce. From January 2018 (when Trump fired the opening salvo in the “trade war”) to December 2019 (when both sides reached a trade agreement), US imports of Chinese goods fell. (Exhibit 1)

Exhibit 1: US Imports of Chinese Goods, January 2018 – December 2019

Source: Census Bureau, as of 7/28/2021. Year-over-year percent change in monthly US imports of Chinese goods, January 2018 – December 2019.

But reality is more complicated. One major overlooked factor, in our view: China was enduring a broader economic slowdown. Annual GDP growth slowed from 6.6% in 2018 to 6.1% in 2019, and that deceleration showed up in several data series. In 2018, exports (9.9%) and imports (15.8%) rose.[ii] The next, exports rose just 0.5% while imports contracted -2.7%.[iii] On a country basis, 2019 Chinese exports to the US fell -12.9%—a big drop after 2018’s 10.8% growth.[iv] But the dramatic reversal wasn’t unique to the United States that year: Exports to Japan also contracted and shipments to South Korea and Germany slowed—all major trading partners. Now, trade tensions with the US likely didn’t help. But in our view, the primary detractor from Chinese growth: policymakers’ efforts to rein in the country’s “shadow banks” and bring more activity into traditional financial markets. That crackdown cut smaller, private companies’ credit access—weighing on economic growth. Furthermore, the country has long been trying to shift from a heavy industry and export-driven economy to one focused at home—particularly in services, Tech and consumption.

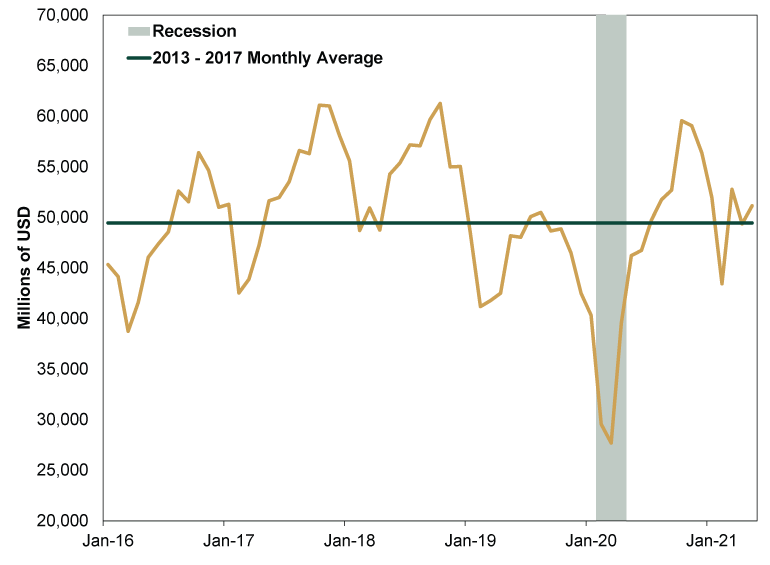

Taking a broader look, the trade spat doesn’t look to have much altered US total trade (exports plus imports) with China. Since the US Census Bureau doesn’t seasonally adjust monthly trade figures, we averaged monthly US total trade with China from 2013 – 2017 (about $49.4 billion).[v] Though monthly total trade dipped below its average for most of 2019—driven largely by the aforementioned Chinese economic slowdown—commerce appears back in line with its normal pattern today. (Exhibit 2)

Exhibit 2: US Total Trade With China, January 2016 – May 2021

Source: US Census Bureau, as of 7/28/2021. Monthly US imports and exports of Chinese goods, not seasonally adjusted, in millions of dollars, January 2016 – May 2021.

Now, the pandemic has obviously skewed the data in a major way since early 2020—both to the downside and upside. After lockdowns decimated economic activity globally and sent total trade reeling, the trade in goods soared, with demand for “stuff” (e.g., personal protective equipment and electronics products for working from home) skyrocketing as people adjusted to COVID living. Although there is no way to know what the data would look like in a non-pandemic environment,[vi] we think it is tough to argue the US-China trade conflict has hurt commerce in a major way—especially as tariffs remain in place.

US-China trade’s resilience isn’t a huge shock to us. As we wrote throughout 2018 and 2019, tariffs, both threatened and implemented, lacked the scale to wallop either economy. They were always more political negotiating tool than new economic policy, in our view. Moreover, companies found ways to dodge them. According to recent Fed research, there was a steady difference between US-reported import values and China-reported export values in the decade leading up to 2018.[vii] But at the trade conflict’s onset that year, the former fell more sharply than the latter. According to the Fed, two reasons are likely behind this: US importers underreported Chinese imports to evade US tariffs and Chinese exporters overreported exports due to changes in tax incentives in China.[viii] Besides that tactic, some businesses routed goods through nearby third countries (e.g., Vietnam) to avoid a “made in China” label—and thereby avoiding duties.

Now, it is possible relations between the US and China worsen under the Biden administration. Maybe America and its allies rally together and ratchet up the pressure on China to make big changes on sociological issues. Maybe China turns more aggressive and strikes back with harsh retaliatory measures. But remember: According to the popular narrative, Trump’s “trade wars” were supposed to upend the global trade order. They haven’t. We caution investors against thinking this time is different under the Biden administration.

[i] “New Trade Representative Says U.S. Isn’t Ready to Lift China Tariffs,” Bob Davis and Yuka Hayashi, The Wall Street Journal, March 28, 2021.

[ii] Source: FactSet, as of 7/29/2021.

[iii] Ibid.

[iv] Ibid.

[v] Source: US Census Bureau, as of 7/29/2021. Average monthly US total trade with China, in millions of dollars, January 2013 – December 2017.

[vi] Though we wish we could!

[vii] “What Happened to the US Deficit With China During the US-China Trade Conflict?” Hunter L. Clark and Anna Wong, Liberty Street Economics, June 21, 2021.

[viii] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Quick Hit: What to Make of Jobs Data’s Persistent Swings2026-04-07

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 30 - April 32026-04-06

-

Expert Commentary US Inflation, Fed Minutes, Consumer Sentiment | 3 Things You Need to Know This Week

2026-04-06

2026-04-06 -

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today