Personal Wealth Management / Market Analysis

This Week in Arbitrary Milestones

The media reaction to some recent, largely meaningless milestones, seems like a sign of improved sentiment.

It seems recent December milestones have the media feeling jolly. The third revision to Q3 US GDP growth revealed the quickest expansion in 11 years. "Wow!" said some long-pessimistic pundits. Also! The Dow Jones Industrial Average reached 18,000 for the first time. "It doesn't get much better than this," another pundit proclaimed. But! US total debt breached the $18 trillion level for the first time ever too. You might expect noise. You got ... crickets? Not that we're complaining! Though arbitrary milestones tell you nothing about the future, the media's reaction can indicate the prevailing sentiment. Today, positive news is accepted for what it is. A near-constant (false) fear isn't riling up the punditry. Sentiment overall seems rightfully optimistic.

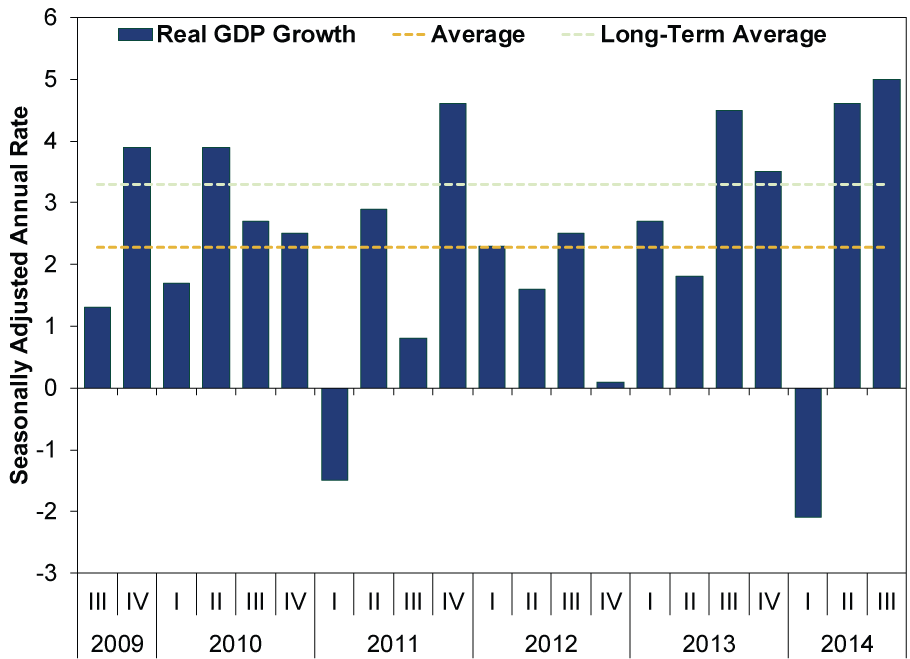

While we believe the US economy warrants optimism, it isn't for the reasons headlines are espousing. Consider the GDP revision. The BEA announced GDP rose at a 5.0% seasonally adjusted annual rate, boosted primarily by consumer spending and business investment. Boom-ish! Not only the fastest in this expansion, the fastest since 2003. In our view, the revision just reinforces the US economy's acceleration we've noted here for a while now. (Exhibit 1)

Exhibit 1: US GDP Growth

Source: US Bureau of Economic Analysis, as of 12/24/2014. US real GDP growth Q3 2009 - Q3 2014. Long-term average, Q2 1947 - Q3 2014.

However, many "experts" continue drawing future conclusions on past information, suggesting there's momentum that'll drive the US economy forward based on big growth rates like Q3's. Even though the third take on summertime data won't say much about how autumn, let alone 2015, growth play out. Don't get us wrong, several forward-looking economic indicators suggest optimism about the US economy is warranted. The Conference Board's Leading Economic Index rose 0.6% m/m in November-the ninth rise in 11 months. No US recession has begun while LEI was high and rising in its 50+ year history. Likewise, in November, the New Orders component of the Institute for Supply Management's Manufacturing (66.0) and Services (61.4) were both well above the 50 level, indicating over half of firms surveyed reported expansion. These are indications growth likely continues ahead, not a hot GDP read. Keep focused on what counts, not what's hot-watching backward-looking indicators and rather arbitrary growth levels to figure out where forward-looking stocks are going is a dangerous practice.

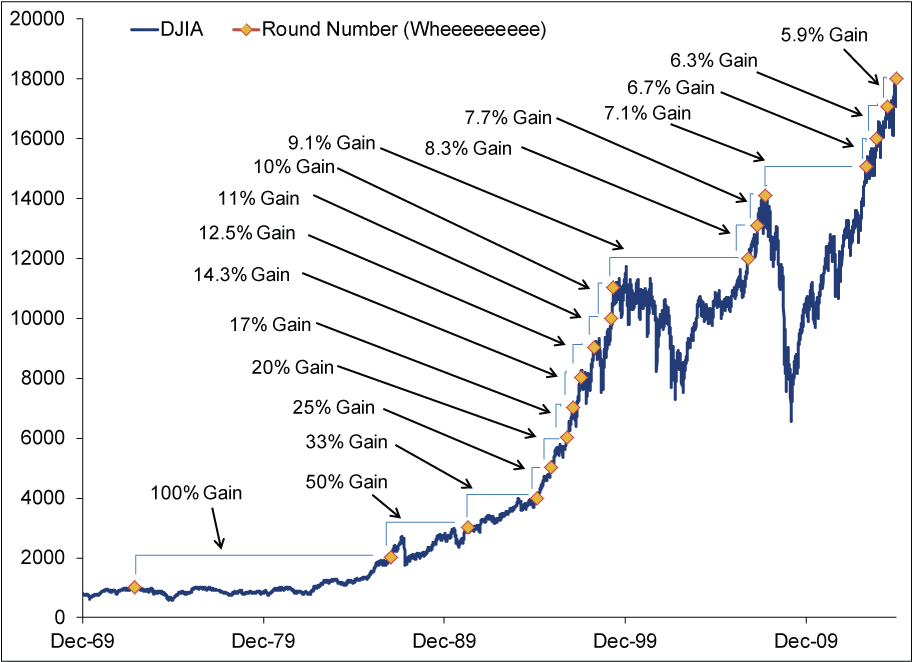

Also not relevant for stocks' direction: Dow Index levels. While it makes for nice market trivia, "Dow 18,000" just means a flawed, price-weighted index of 30 randomly chosen stocks hit another nice round number. This isn't evidence of the fabled Santa Claus Rally-we're sorry, Virginia, Santa Claus Rallies are fiction. Others marvel at how quickly the Dow jumped from round number to round number, suggesting a rally like this may never repeat. For example, some note it only took the Dow 172 days to go from 17K to 18K-the fifth-fastest thousand-point rise. It took 15 years to go from 1K to 2K ! Yet this shouldn't be a shocker. A jump from 17K to 18K is less than 6%. A 1K to 2K move is 100% (Exhibit 2).

Exhibit 2: The Dow's Round Numbers

Source: FactSet. As of 12/23/2014. Dow Jones Industrial Average Price Level from 12/31/1969 - 12/23/2014.

Certainly, some moves take longer than others, particularly when bear markets hit. For example, 1,462 days passed between Dow 14K and 15K due to 2008's financial panic. But during bull markets, stocks pass lots of new numbers as they climb higher-and they're likely to advance 6% faster than 100% (just sayin'). One hundred or one thousand Dow points aren't what they used to be (not that they ever meant much in isolation). DJIA 18K is just as arbitrary as 2,082: the S&P 500 Price Index's closing price on Tuesday, which was also an all-time high. Both mean nothing about the future.

On the flipside, the US hit another arbitrary milestone-gross federal debt crossed over $18 trillion-yet few headlines are bemoaning the country's future prospects because of it. Now, we're not saying concern is warranted-we've long argued US debt isn't as onerous as many folks think. Heck, the government itself owns $5.04 trillion of that debt, which means it is both an asset and a liability on its balance sheet. That cancels. Now, $18 trillion, $13 trillion-neither are small numbers. But scale them! Interest payments are less than 8% of tax revenue, half the level of the go-go 1980s and 1990s. The US has as little trouble financing itself today as in recent years. Which isn't a change.

What has changed is the media coverage. Consider how headlines treated other instances when debt passed a big number: At $15 trillion, US Debt Is Now Equal to Economy. National Debt Passes $16 Trillion: Should You Worry? U.S. Debt Tops $17 Trillion for First Time! These stories are the tip of the iceberg. Many books for many years have been written on US debt, like this one claiming it was an anchor on US growth ... at $4 trillion in 1993. This time? While $18 trillion got a little bit of ink, coverage has been nowhere near where it was in the past-a sign of growing optimism. Folks rationally aren't seeing ghosts in federal debt.

This is all part of a bull market's natural maturation. Dire pessimism gave way to skepticism. Which is now ceding more and more territory to optimism. Yet irrational euphoria-extreme optimism built on sand-seems largely absent. To us, more investors are finally correctly seeing-and believing-that the bullish backdrop long underpinning stocks is real. Even if the specific stats they cite have holes.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today