Personal Wealth Management / Financial Planning

Trade-Offs of Target-Date Funds

Investors should consider much more than their retirement date when creating an investment plan—so why are funds solely focusing on just that so popular?

Since the dawn of capital markets, folks have searched for that silver bullet financial product to meet their every need for all time. History overwhelmingly shows they may as well search for the Holy Grail or a unicorn, but the quest continues. These days, many believe they’ve found the answer in target-date funds (TDFs)—mutual funds investing in a combination of stocks and bonds that gradually dial down the percentage invested in stocks as the target date nears.

In recent years, TDFs have rapidly gained popularity in 401(k)s and other retirement plans as their set’n’forget reputation lures investors and plan administrators looking for an easy fix. The appeal is understandable: No strategizing—just add money! But those who rely on TDFs for a comfortable retirement might end up falling short of their long-term goals.

TDFs’ alleged convenience and drawbacks stem from the same source: the funds’ mechanics. TDFs operate according to “glide paths”—they reallocate every few years to include more fixed income investments as they approach the target date, which investors typically match with their planned retirement date. Say an investor’s looking to retire in 2040—27 years from now—and his TDF has a starting allocation of 60% stocks and 40% bonds. In 5 years, that allocation might change to 50%/50%, in 10 years to 40%/60%, in 15 to 30%/70% and you get the idea. In theory, by the time that investor retires, his or her TDF could be 100% bonds or cash equivalents.

Problem is, this approach rests on a fatal flaw: It assumes an investor’s time horizon ends when retirement starts. It doesn’t! Time horizon refers to the length of time folks need to be invested to reach their financial goals. Retirement is simply when they start relying on their investments instead of a job for income (assuming that’s one of their objectives). Not allocating their investments correctly post-retirement (or, for that matter, in the run-up to it) could increase the risk of running out of money.

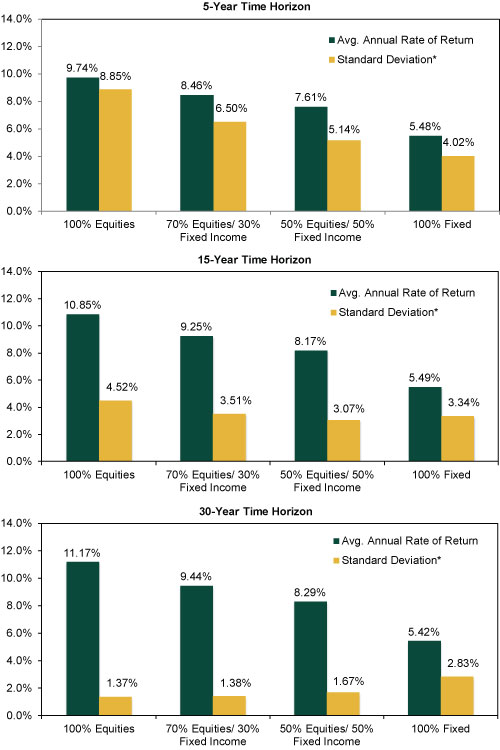

Long-term goals vary from person to person, but generally, they tend to include providing for them and their families over their entire retirement. With life expectancy lengthening over time, the average new retiree could need his or her money to last decades. This could very well require achieving equity-like returns well after retiring—and significant equity exposure even through the twilight of their working years! Sitting in a fund whose equity exposure shrinks when investors may need equity-like growth most likely won’t get these folks where they need to be.

This leads us to the other fundamental problem with TDFs. Their tactical approach accounts only for time invested and retirement date, not an investor’s personal circumstances, needs and long-term goals. Long-term goals, cash flow needs, overall financial situation and time horizon are just a few of the major factors investors should consider when determining their optimal investment strategy. Do they need regular income after they’re through working? Do they want to travel? Maintain a certain standard of living? Gift to their kids? Grandkids? A charity? Pay for weddings and college educations? Plus, what if something unexpected comes up, like a big medical expense? TDFs don’t factor in any of these considerations. They aren’t tailored to an investor’s unique needs.

Even if a TDF’s prospectus claims it provides sufficient retirement income for a given period, there are no guarantees. What if the TDF plan provides enough income to live comfortably for 10 years after retirement, but the investor goes on to live for another 17? Running out of money is one of the biggest risks investors face in retirement. TDFs frequently raise this risk—exactly the opposite of the sleep-at-night comfort many claim to provide.

How? TDFs assume owning more fixed income and fewer equities as time goes on is an automatic positive. Perhaps, if an investor’s time horizon is short enough or if the likelihood they achieve their goals are increased by experiencing less short-term volatility, it’s the right move. But if an investor needs their money to last 20-plus years after age 65, history suggests otherwise. Over lengthy periods, stocks have historically performed better than bonds, increasing the chances investors with higher equity exposure (as their cash flow needs and other considerations allow) meet their retirement goals. But each time a TDF’s allocation adds bonds and removes stocks, the investor likely decreases their long-term return potential.

Exhibit 1: Stock Versus Bond Performance in 5-, 15- and 30-Year Time Horizons

Source: Global Financial Data, Inc.; as of 01/28/2013.i *Standard deviation is a measure of volatility, representing the degree of positive and negative fluctuations in the average annual performance return for the 5-, 15-, 30-year rolling time periods between January 1926 and December 2012.

And what of inflation? Prices, particularly for products retirees often consume like health care, grandkids’ education expenses and more tend not to fall over time. That means even more growth is needed. Reducing equity exposure and boosting fixed income doesn’t reduce risk—it simply shifts the type of risk you’re taking. TDFs trade volatility risk for interest rate, reinvestment and inflation risk. The funds are not taking less risk as time passes, they are taking different risk!

Before putting your retirement plan on autopilot, it’s crucial to consider the destination—and whether the fund is actually on a map to get you there. Just because a TDF may seem dandy at first glance, doesn’t mean it or its future changes will match an investor’s needs as time goes on—or that an investor even has the discipline to reap what long-term potential it might have. Investors looking for the most bang for their bucks in retirement would do well to critically assess a TDF’s underlying assets and glide path—and, most importantly, consider their long-term goals, time horizon and other available investment approaches to find what best suits their needs.

i Average rate of return from 1926 through 12/31/12. Equity return based on Global Financial Data, Inc.'s S&P 500 Total Return Index. The S&P 500 Total Return Index is based upon GFD calculations of total returns before 1971. These are estimates by GFD to calculate the values of the S&P Composite before 1971 and are not official values. GFD used data from the Cowles Commission and from S&P itself to calculate total returns for the S&P Composite using the S&P Composite Price Index and dividend yields through 1970, official monthly numbers from 1971 to 1987 and official daily data from 1988 on. Fixed Income return based on Global Financial Data, Inc.'s USA 10-year Government Bond Index.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today