Personal Wealth Management / Market Analysis

What a Gold Rush

What does gold’s recent fall mean for mongers’ precious metal?

Monday, gold dropped its farthest in a single day since the early 1980s, falling -8.7%—over $100 an ounce. The daily dive continued a more than 25% decline from its record high in September 2011. To be sure, many asset classes can experience (sometimes significant) short-term volatility, and that doesn’t make them bad long-term investments. But in our view, this episode really only shows gold for what it is: a commodity. And like all commodities, gold’s long-term performance is driven by supply and demand—not many of the common myths like gold’s an effective inflation hedge or safeguard against financial woes up to and including zombie apocalypse.

Commodities like gold tend to be very volatile, so it doesn’t really surprise us much to see that volatility strike. Since Monday’s big drop, gold’s snapped back—upward volatility regaining some ground. The big swings have spawned a number of theories regarding its cause—ranging from blaming recent, disappointing (to some) Chinese economic data, lower inflation rates and Cyprus’s potentially selling its gold reserves. (Many fear if Cyprus sells gold as part of its bailout deal, other countries—potentially with more reserves—will do the same.) Possibly one or all of these items (or something else entirely) affected gold’s price by zapping demand some, but more than likely they’re just speculation.

Speculation seems an apt word to use when discussing gold. Looking back through the years, it appears the only way to do well with gold is to be able to time it really well. As a long-term investment, gold’s more volatile and lower returning than stocks—a poor combination. Yet some persist in believing tales of gold’s magical economic properties. But many of these theories have significant holes. For instance, that inflation-hedge theory.

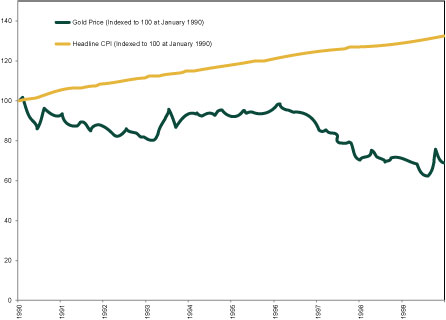

To be an inflation hedge, you might think gold should track the inflation rate pretty closely. But in the 1990s gold lagged inflation quite a bit—meaning if you were invested in gold at the time, your investment likely lost quite a bit of value (in nominal terms, as gold fell over the decade, and even more so when inflation is accounted for).

Exhibit 1: Gold v. Inflation in the 1990s

Source: St. Louis Fed. Gold price shown is the average monthly price.

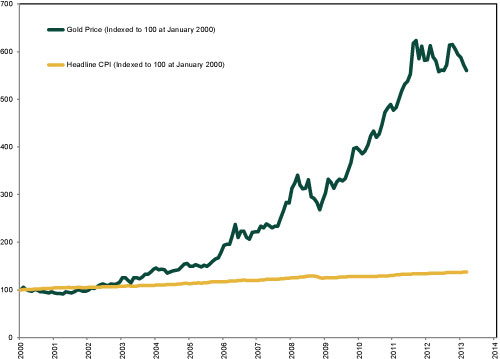

But in the 2000s, gold rapidly outpaced inflation—even though the 2000s’ average CPI was 2.6%, slightly lower than the 1990s’ 3.0%.i Pretty bizarre behavior if gold’s an effective inflation hedge.

Exhibit 2: Gold v. Inflation in the 2000s

Source: St. Louis Fed. Gold price shown is the average monthly price.

You could similarly debunkmost any myth regarding gold. The overall fact is gold’s performance, like just about anything in a market economy, hinges on supply and demand. Supply rather gradually increases over the long run, but demand can fluctuate a lot. Gold demand is underpinned by relatively few things: Jewelry, central bank and government reserves, collectibles and investment demand. That last category can be quite fickle in the short term and can easily send gold prices on a wild ride.

For those watching without owning gold, the gyrations are interesting and notable, but with few industrial uses, the direction of the overall economy isn’t a reliable predictor for gold prices—nor are gold prices a reliable predictor of the world economy.

i Source: Federal Reserve Bank of St. Louis. Average monthly headline CPI rate for 1/1/1990 – 12/31/1999 and 1/1/2000 – 12/31/2009.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Market Analysis Why the SOX “Bear Market” Isn’t Foreboding2026-07-21

-

Politics Blunting Burnham?2026-07-21

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today