Personal Wealth Management / Politics

What Canada’s Election Means for Global Investors

Politics will likely be gridlocked, but other headwinds weigh on Canadian stocks.

After a contentious campaign, incumbent Canadian Prime Minister Justin Trudeau won reelection in Monday’s vote, though his Liberal Party lost some ground and fell far short of a majority. Trudeau is now likely to head a minority government, perhaps with the lukewarm voting support of the left-leaning New Democratic Party. The likely upshot is gridlock—typically bullish, especially for developed economies. Yet Canadian stocks still face other country-specific headwinds that mitigate this positive political development.

The Liberals won 157 seats in the 338-seat House of Commons—down from their 177 entering the election and below the 170 needed for a majority.[i] The Conservatives will be the main opposition with 121 seats. Bloc Québécois—Quebec’s separatist party—and the New Democrats round out the top four with 32 seats and 24 seats, respectively.[ii] Despite maintaining control, the Liberals’ showing was the weakest for a victorious party in Canadian history—their 33% share of the national popular vote actually trailed the Conservatives’ 34%.[iii] (Canada votes by constituency, much like the US House of Representatives and British Parliament, with the candidate who wins the most votes in each “riding” winning the seat.) In many parliamentary systems like Britain’s or Germany’s, this would mean coalition talks to form some kind of unity government that combines to a majority of seats. But coalitions are rare in Canada—and one looks unlikely to form right now. Instead, Trudeau seems likely to lead a Liberal minority government with the tacit voting support of the New Democrats (and perhaps other parties) on select issues.

As is the case for many incumbents, Trudeau’s support has waned over the past four years—especially with a handful of recent scandals stealing headlines. Now entering his second term as Canadian premier, Trudeau doesn’t enjoy the same mandate he did in 2015, when he was a popular young newcomer—forcing him to work with other parties. The New Democrats have some ideological overlap with the Liberals, but the two parties have big differences, too. One example: disagreements over economic policy, particularly in regards to energy. The New Democrats have taken a tough stance on environmental issues, and they campaigned on stopping pipeline expansion, ending federal subsidies for fossil fuels and providing incentives for alternative energy sources. The Liberals’ approach has been squishier. Despite promoting itself as environmentally friendly, Trudeau’s government nationalized and advanced a trans-mountain pipeline to support Alberta’s big oil industry, which has struggled to ship crude to refineries and ports, particularly in British Columbia. While such disagreements aren’t likely to lead the New Democrats to block the Liberals from forming a minority government, passing major legislation will require a lot of horse trading and compromise—likely leading to watered-down results.

From an investing perspective, stocks typically prefer when legislatures struggle to pass big new laws. Sweeping legislative changes tend to increase uncertainty, create new winners and losers, yield unintended consequences and discourage risk-taking. So, the Canadian political backdrop looks like a plus for its markets. Yet politics are only one driver. Other factors—like equity market sector composition—matter, too.

Canadian stocks skew heavily towards Energy and Financials—which is heavily connected to Energy, as Canadian banks have significant loan exposure to domestic Energy companies. The two total 53.5% of listed Canadian stocks, far exceeding the world’s 20.5%.[iv] In our view, the Energy firms poised to do best in the current market environment are the biggest, globally minded producers with diversified revenue streams and lower production costs. Canadian producers—which face higher extraction costs and lower prices for Canadian oil blends due to their dirty nature—don’t fit the bill.

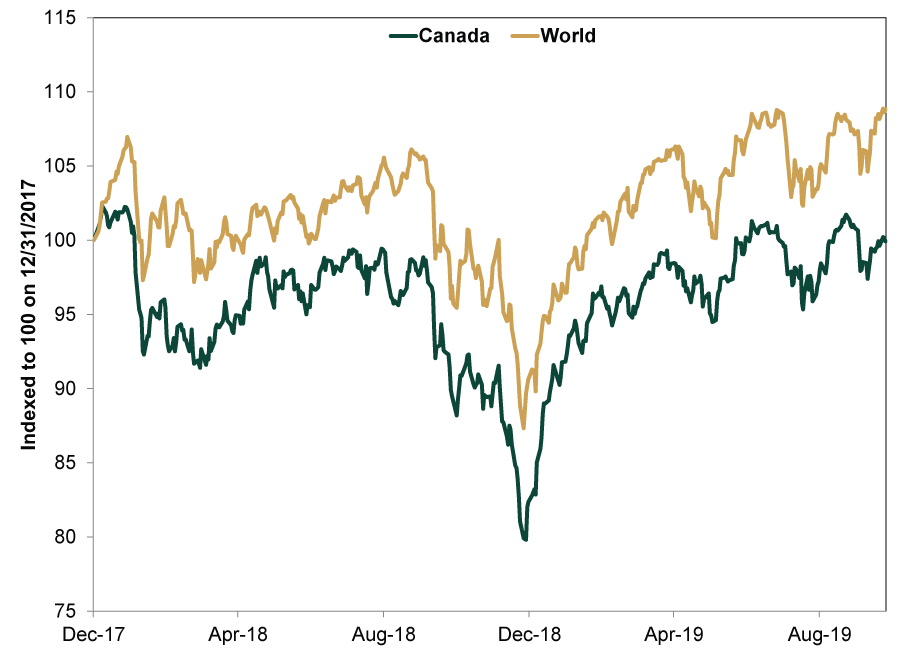

Though Canadian stocks are slightly outperforming global stocks year to date, this seems due largely to sentiment and last year’s Q4 global stock market correction.[v] Canadian stocks dropped more sharply than global stocks last year. Categories that fall the most tend to bounce back the highest, and Canadian stocks rebounded strongly off the correction’s bottom in early 2019. We didn’t think that would last, which recent months have illustrated. Since June 30, Canadian stocks are down -0.2%, whereas global stocks are up 1.9%.[vi] Going forward, we believe Canada’s market composition-related headwinds will keep weighing on local stocks.

Exhibit 1: MSCI Canada vs. MSCI World Since 2018

Source: FactSet, as of 10/23/2019. MSCI Canada and MSCI World Index returns with net dividends, in USD, from 12/31/2017 – 10/22/2019. Indexed to 100 on 12/31/2017.

[i] Source: CBC News, as of 10/22/2019. https://newsinteractives.cbc.ca/elections/federal/2019/results/

[ii] Ibid.

[iii] Ibid.

[iv] Source: FactSet, as of 10/24/2019. MSCI Canada Investible Market Index (IMI) and MSCI World IMI Index Energy and Financials sector weights as of 10/23/2019. Investible Market Indexes used as they are the broadest available measure, covering roughly 99% of listed equities.

[v] Source: FactSet, as of 10/24/2019. MSCI Canada Index and MSCI World Index returns with net dividends, USD, 12/31/2018 – 10/23/2019. In USD, returns are 20.7% and 19.2%, respectively; in Canadian dollars, returns are 15.7% and 14.3%, respectively.

[vi] Source: FactSet, as of 10/24/2019. MSCI Canada Index and MSCI World Index returns with net dividends, USD, 6/30/2019 – 10/23/2019. In Canadian dollars, returns are -0.1% and 2.1%, respectively.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today