Personal Wealth Management / Market Analysis

Where Trade Talks Stand

Despite trade war fears, tariffs remain tiny and negotiations to resolve them are ongoing—setting up bullish upside surprise.

Just a few weeks ago, tariff talk—and fears of a disastrous trade war tanking stocks and the global economy—were all the rage. Flash forward to today, though, and you may see a different picture: In late July, the US and EU reached a verbal agreement deepening bilateral trade relations. And now, rather than tariff terror, trade deal talk is in the air. Monday, negotiators announced progress in crafting a new North American Free Trade Agreement (NAFTA). And while there wasn’t much concrete progress, US and Chinese officials at least talked. This, in our view, is just the latest illustration of a wide, bullish gap between sentiment and reality on trade. If tariffs remain small and used mostly as a negotiating ploy before giving way to even freer trade—proving fears false—stocks should shine.

Perhaps the best example: The US and Mexico reached a preliminary deal to overhaul NAFTA, with a final deal including Canada possible by Friday. Many thought NAFTA renegotiations would stall ahead of Mexico’s new government entering office December 1, but dealmakers from the incoming Mexican administration have joined talks in a consulting role, speeding the process. Over the weekend, US and Mexican negotiators surmounted several sticking points, including reaching agreement on automobile “rules of origin”—what share of cars’ parts are sourced in North America. They apparently also hammered out an energy chapter further integrating North American energy production and trade. Work remains on investor-state dispute resolution and a sunset clause, though most believe there is room for compromise. The deal allows them to move forward and have Canada rejoin talks, putting together a final accord, possibly before December. Which you can feel free to read as “around November” or “just after the US midterm elections, in which President Trump is using trade as an issue to motivate his base.”

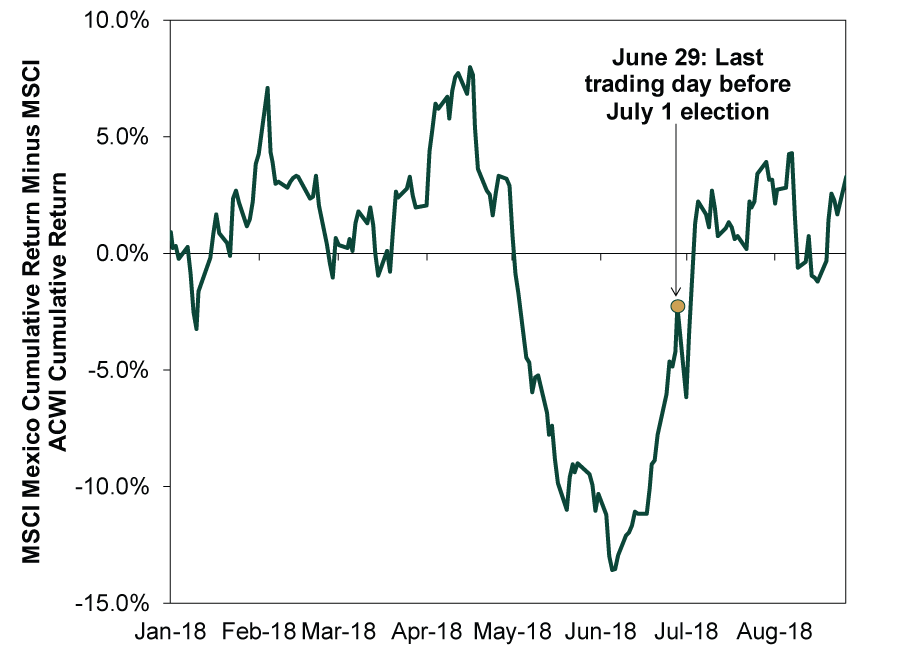

While the deal could still fall apart and has plenty of detractors, markets seem to enjoy the better-than-feared outcome of NAFTA imploding. As talks progressed and news leaked of an approaching deal, Mexican stocks jumped. Exhibit 1 shows Mexican stocks have returned to outperforming the MSCI All-Country World Index after NAFTA and election fears weighed on returns this spring. With election uncertainty falling and trade fears easing, Mexican markets have rebounded.

Exhibit 1: Mexican Stocks Rebound as Talks Improve

Source: FactSet, as of 8/28/2018. MSCI Mexico return with net dividends minus MSCI All-Country World Index with net dividends, both in USD, 1/2/2018 – 8/27/2018.

Though the US and China each implemented a second round of long-discussed tariffs last week, we think the bigger news is that Chinese and US trade officials talked—the first time since May. While they made little headway, that officials spoke is a positive step. Ahead of talks, President Trump downplayed deliberations, saying he had “no time frame” for ending the dispute, adding “I’m like them; I have a long horizon.” Trump’s tariffs are purportedly to stop intellectual property transfers, reduce subsidies and open up Chinese markets, but we believe they are also about prodding Beijing to pressure North Korea to advance denuclearization. According to most reports, North Korea hasn’t acted much following Trump’s meeting with dictator Kim Jong-un. Also last week, Trump canceled Secretary of State Mike Pompeo’s trip to Pyongyang. Meanwhile, China has filed WTO complaints and is targeting its tariffs to maximize political pressure on the president. Officials are also reportedly readying non-tariff countermeasures. So it is slow-going with China, although many still expect Trump and Chinese President Xi Jinping to meet later this year, with trade high on the agenda. That meeting is scheduled for ... November.

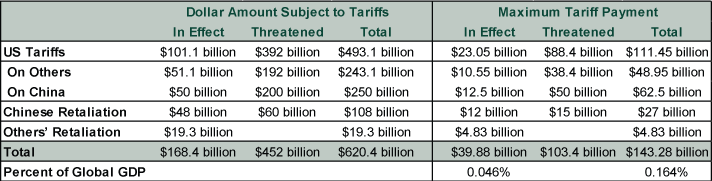

The lack of progress here isn’t disastrous. As Exhibit 2 shows, each side has levied about $12 billion in tariffs so far. While not great for exporters (and consumers), at a fraction of a percent of GDP, it is hardly likely to cripple the global economy—or markets. And that is if all the tariffs are paid at face value—unlikely. Substitution and tariff avoidance mean Exhibit 2’s estimate likely overstates the actual impact.

Exhibit 2: Tariffs Threatened and Enacted as of August 23

Source: IMF, US Trade Representative, China Ministry of Commerce, the American Action Forum, CNN, Politico and the Peterson Institute for International Economics, as of 8/23/2018. The IMF’s estimate of nominal global GDP, in US dollars, is $87.5 trillion as of April 2018.

Headlines continue screaming about the negative fallout from trade tensions, but this mostly just affects sentiment. Fundamentals, as evidenced by recent purchasing managers’ index (PMI) data, remain solid. The US’s latest flash manufacturing and services PMIs for August are in the mid-50s,[i] showing growth likely persists, as figures above 50 denote expansion. Strong new order growth also suggests demand remains robust despite pervasive trade fears. July Chinese PMI data were weaker, in the low 50s,[ii] but that could be because of tightening credit conditions as much as deteriorating trade. Besides, new orders suggest further growth here, too. Moreover, China has begun stimulus measures, which economic indicators likely don’t yet reflect. Progress in trade negotiations could help relieve worries and buoy stocks. But even if deals elude negotiators, we think tariffs presently enacted or under consideration remain too tiny to alter stocks’ upward trajectory. We believe the gap between this reality and the far-flung fear is quite bullish.

[i] Source: IHS Markit, as of 8/23/2018. Flash US Composite Output Index, August 2018. Although we generally cite the Institute for Supply Management’s PMI data for the US—it has a longer history—Markit’s “flash” estimates covering about 85% – 90% of total survey respondents are more timely. Markit’s preliminary August data are out, but ISM’s latest is for July.

[ii] Source: Caixin, as of 8/3/2018. China Composite PMI, July 2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

-

Market Analysis The Investment Implications of Record-Low Consumer Sentiment2026-05-19

-

Market Analysis More Positive Surprise in Japan’s Q1 GDP2026-05-19

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—May 11 - May 152026-05-18

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today