Personal Wealth Management / Market Analysis

Your Annual Reminder Not to Sell in May

An antidote to markets' mythological summertime blues.

Hello readers, it's May, and you know what that means-pundits across the financial internets are bombarding the world with reasons they should or shouldn't follow that tired seasonal adage, "Sell in May and Go Away." Our take is the same as ever: Don't do it. Seasonal tropes like Sell in May, the January Effect, the Santa Claus Rally and Financial Hurricane Season are hogwash. Their occasional hits are coincidence without causality. The turn of a calendar page is never reason to buy or sell. We've spilled many pixels on Sell in May over the years-see here, here, here, here, here, here and here. Here are some more pixels and pictures-pictures that show just how much investors can miss by sitting out the summer.

"Sell in May" has many iterations, but most involve selling sometime in May and returning sometime in autumn. The original saying, "Sell in May and go away, and come back at St. Leger Day," refers to brokers' tendency to take the summer off back in the old days, returning around the time of Britain's St. Leger Day horse race in September. Courtesy of the Stock Trader's Almanac, that morphed into selling on April 30 and getting back in on October 31, after Financial Hurricane Season (September and October). Regardless of the timeframe, the underlying belief is this: Stocks are a bummer in the summer, so best to just get out, go on vacation, and laugh maniacally at everyone else when markets inevitably slide. The very scant supposed evidence for this is the fact returns from April 30 - October 31, on average, trail returns from October 31 - April 30. Add in some cherry-picked years where selling in May would have worked-most recently, 2011 and 2008-and the adherents consider the case closed.

But it isn't. For instance: Some say Sell in May worked last year, citing the correction's May 21 start date and the S&P 500's -9.1% decline from Memorial Day through Labor Day.[i] But that's cherry picking dates, friends, and using the benefit of hindsight. Follow the increasingly standardized April 30 - October 31 blueprint, and you'd have missed a 0.8% S&P 500 total return. And lost out on transaction costs and potentially taxes, depending on account type.

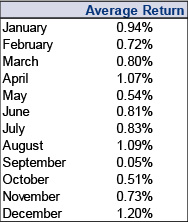

May is just a month. So are the other 11. The May through October window is an arbitrary six-month stretch, no more special than any other six-month stretch. All rolling six-month stretches have positive average long-terms. So does May. So does every month but September, which is skewed by four data points (1930, 1931, 1937 and 2008). The May-October period happens to be the weakest six-month stretch, but that's a statistical quirk, nothing more. And it misses the point, because a 4.12% return is still up and nothing an equity investor should aim to avoid.

Exhibit 1: Average Monthly Returns, 1926 - 2015

Source: Global Financial Data, Inc., as of 4/28/2016. S&P 500 Total Return Index.

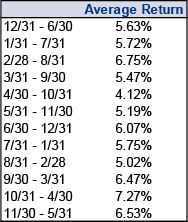

Exhibit 2: Average Rolling Six-Month Returns, 1926 - 2015

Source: Global Financial Data, Inc., as of 4/28/2016. S&P 500 Total Return Index.

1926 isn't an arbitrary start date-it's when verified market data begin, thanks to the dedicated folks on the Cowles Commission. But for kicks and grins, if we go back all the way to 1800, using the less-reliable-less-liquid-but-still-entertaining-and-sorta-useful-for-illustrative-purposes dataset of antique returns, May is still positive, and there still ain't no such thing as the summertime blues.[ii]

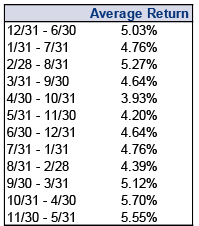

Exhibit 3: Average Monthly Returns, 1801 - 2015

Source: Global Financial Data, Inc., as of 4/28/2016. S&P 500 Total Return Index.

Exhibit 4: Average Rolling Six-Month Returns, 1801 - 2015

Source: Global Financial Data, Inc., as of 4/28/2016. S&P 500 Total Return Index.

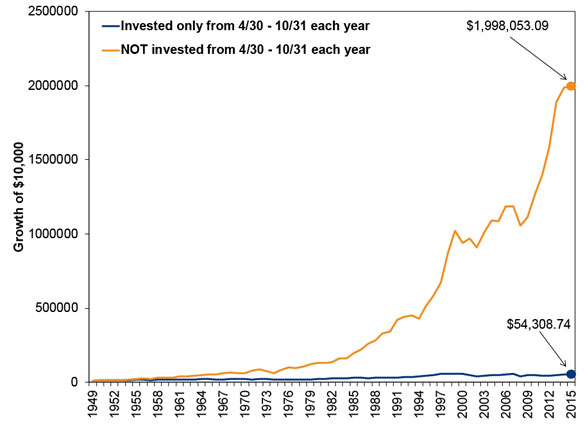

One chart we encountered claimed to show owning the S&P 500 in only the May - October window of each year since 1950 would have lost you money, taking $10,000 down to $8,071, while investing in only the other six months would have caused that $10,000 to soar to $626,764. But we crunched the numbers, again using S&P 500 total returns, and we got wildly different results.

Exhibit 5: Growth of $10,000 Two Ways

Source: Global Financial Data, Inc., as of 4/28/2016. S&P 500 Total Return Index.

Yes, sitting out the Sell-in-May window would have generated far higher returns than investing only from 4/30 - 10/31, but again, the summer stretch isn't negative. Investing in summer only still more than quintupled your hypothetical money. That is a moneymaker, not a money-loser.

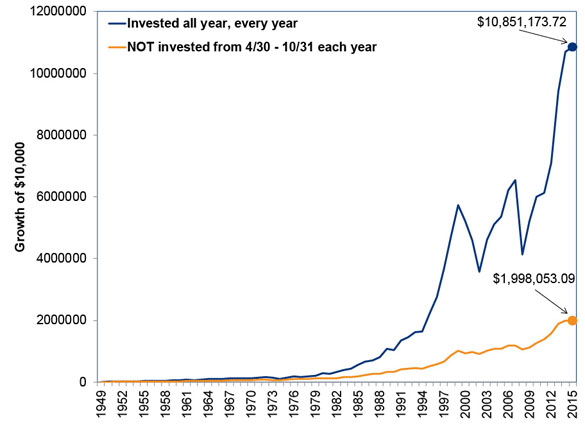

Which, of course, means you miss big returns over time if you follow Sell in May to the letter. Those missed returns are far, far greater than the $44,308.74 implied by Exhibit 5, because you also miss the potential for those gains to compound over time. That adds up. A lot. Exhibit 6 shows just how much.

Exhibit 6: Selling in May Hurts

Source: Global Financial Data, Inc., as of 4/28/2016. S&P 500 Total Return Index.

Yes, if you invested $10,000 on 12/31/1949, the opportunity cost of being a "Sell in May" devotee since then is $8,853,120.63. Or, if you prefer, 46.9 median US homes. Or 32.8 Ferrari 458 Italia convertibles. Or 7,370.72 round-trip tickets from San Francisco to Paris. Or 10,943.3 Vail season passes. Or 273.2 years of room and board at the average US private university. Or 170.45 years' worth of the US median household income. Ouch.

Some say this is the year to sell in May because it's an election year, citing May's not-so-great average return in election years since 1952. But the average 0.07% S&P 500 total return in election-year Mays from 1952 on means election-year Mays are quite variable, not uniformly weak. Returns were positive 11 of 16 times. The spectrum ranges from -6.3% (1956) to 2.79% (1952), with a median of 1.3%. But last we checked, "Sell in May and come back in June" isn't a thing. Using the traditional May - October window, election years average 3.31%. Toss out 2008, when "Sell in May" would have avoided a -29.28% decline that had much more to do with an accounting rule-driven financial crisis than with anyone running for office, and the average rises to 5.48%.[iii]

Now, maybe Sell in May does work this year. Broken clocks and all. But short-term moves are impossible to predict, and selling now because short-term volatility might strike at some point in the next six months is not a recipe for success. That astronomical growth of $10,000 in Exhibit 6 includes all manner of pullbacks, corrections and even bear markets. We aren't fanatical buy-and-holders, as it does make sense to take cover if you are darned sure-based on strong fundamental evidence-a bear market is forming. But other than that, if your long-term goals require market-like returns over time, then you should own stocks no matter what month it is. That's how you get market-like returns.

[i] FactSet, as of 5/3/2016. S&P 500 Total Return Index, 5/22/2015 - 9/4/2015.

[ii] Which is good, because there ain't no cure, as we all know.

[iii] Everything in this paragraph comes from Global Financial Data, Inc., as of 4/28/2016. S&P 500 Total Return Index.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q2 Market Recap, June US Jobs, Trade Deal Update

2026-07-03

2026-07-03 -

Market Analysis Why El Niño Doesn’t Necessitate Portfolio Shifts2026-07-01

-

Market Analysis Declaring Fed Independence Fears False2026-07-01

-

Market Analysis Reader Mailbag: June 20262026-06-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today