Personal Wealth Management / Market Analysis

Around the World in All-Time Highs

Are recent all-time highs a warning sign the bull's end is nigh?

Stock indexes worldwide continue climbing to new heights. The FTSE 100 hit a new high this week, its first in 15 years. The Nasdaq is a rounding error from 5,000, itself a rounding error from its early 2000 record. The Nikkei 225 isn't close to an all-time high, but it too is near levels last seen in April 2000.[i] The MSCI World, S&P 500 and Germany's DAX have added to records set earlier in this bull market, too. This record-breaking flurry has spurred comparisons to the early 2000s, when the tech bubble popped. Nasdaq, FTSE and Nikkei price levels might be similar, but today's environment doesn't resemble 2000's-all-time highs are just what you get in a rip-roaring global bull market. They aren't evidence of a bubble or bull market about to die.

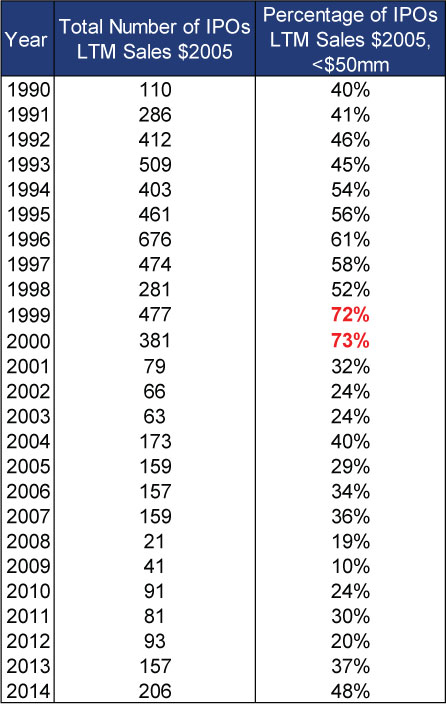

The Nasdaq's current climb toward 5048 doesn't resemble the last one. In 2000, technology was ushering in the "New Economy." Pundits cheered the 1990s' growth, saying, "there is no end of that success in sight." A CNN roundtable debated whether "boom and bust" was over forever. "Dot-Com" initial public offering (IPOs) hit fever pitch, with mom and pop investors clamoring to get in. Yet many of these companies were slop, pushed by investment banks to take advantage of rising investor optimism. As a New York Times article noted, "instead of repelling investors, a lack of profits, past performance or history of any kind appears to be an enticement these days." According to the University of Florida's Professor Jay Ritter, 72% and 73% of IPOs in 1999 and 2000 had less than $50 million in sales. 2014? 48%. (Exhibit 1)

Exhibit 1: IPOs Categorized by the LTM (Last Twelve Months) Sales, 1990-2014

Source: Professor Jay R. Ritter, University of Florida. In 2005 dollars. Data accessed 2/25/2015.

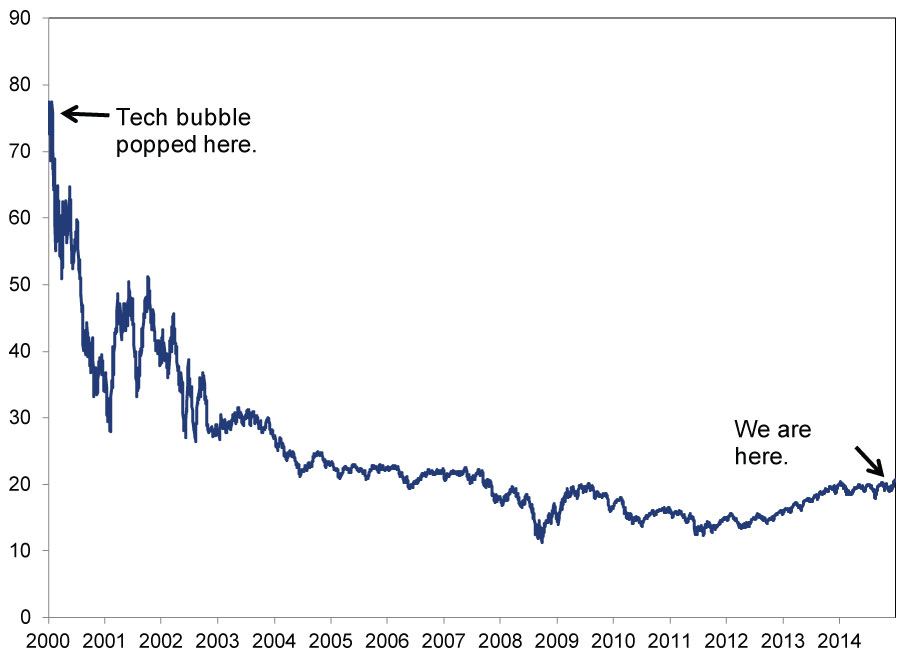

Valuations aren't near 2000's levels, either. The Nasdaq's forward price-to-earnings ratio (P/E) is a fraction of what it was then (Exhibit 2). So are its trailing P/E (101.5 vs 24.4)[ii] and price-to-sales ratio (10 vs. 2.6)[iii]. Sentiment isn't extreme.

Exhibit 2: Nasdaq's 12-Month Forward P/E

Source: FactSet, as of 2/25/2015. Nasdaq Composite Index, Price-to-Earnings Ratio, 2/29/2000 to 2/24/2015.

But these are all facts about the public equity markets, and some suggest the bubble is in private firms-mostly based on what some consider eye-popping valuations of a handful of start-ups. But even if you assume these valuations are truly shocking, if you must dig that deep for froth, things probably aren't very frothy. Euphoria is widespread at peaks.

While all-time highs stir some investors' suspicions stocks are pricey, stocks don't seem wildly overvalued. Those 15-year-old FTSE 100 and Nasdaq records aren't ceilings. No level is! Bull markets don't die because of gravity. A bull ends in one of two ways. It loses steam in euphoria-like in 2000-as reality can no longer match sky-high expectations. Or a shocking negative wipes trillions off the roughly $75 trillion global economy, like 2008. Absent the wallop from a well-intended but poor-in-practice accounting rule and the haphazard government actions that followed, many global indexes could have surpassed their 2000 highs much sooner.

Index levels say much more about index construction than they do the outlook for the stocks that comprise them. Consider: The FTSE's 100 London-listed companies don't adequately represent the whole UK market-and there are often constituency changes. More than half of FTSE 100 companies in 2000 aren't in it now. Telecom and Tech dominated the index in 1999. Today, Energy rules-and Energy stocks have struggled for years, likely delaying hitting this "milestone."[iv] But also! The FTSE 100 level folks are pointing to is the price index, which excludes dividends, an important consideration for return. The FTSE 100 Total Return Index first surpassed its 2000 peak on 1/27/2006, closing the 2002 -2007 bull at a record 3,889.16.[v] That level was breached over four years ago, and it is 35% higher now. But it's still 100 companies. The 465-company strong FTSE All Share Ex. Investment Trusts currently sits 86% above its 2000 high and 41% above 2007's mark.[vi]

Similarly, Germany's DAX includes dividends-and has racked up 13 new highs[vii] since mid-January, but it's all of 30 stocks, just liked the flawed Dow Jones Industrial Average. Japan's Nikkei 225 covers more, but like the Dow, it is price-weighted-a fatal flaw. That it is near a big round number last seen during the tech bubble is trivia. And even then it's true only in yen-in dollars, the Nikkei is still -22% below its April 2000 close.[viii] It has been well documented here that the US S&P 500 Total Return index and the global MSCI World Total Return index have notched dozens of all-time highs in this bull-a few more lately, too. If record levels indicate stocks are high, why do these gauges keep sailing through them? Why did they do the same in the 1990s and 2000s? Drawing literally any future conclusion from this-or some purely numerical similarity with 2000-is a behavioral investing error. We're sorry to say so, but sadly it's true: Market levels won't predict what markets will do.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Still nearly 50% below its late-1980s peak.

[ii] Source: FactSet, as of 2/25/2015. From 2/29/2000 and 2/23/2015.

[iii] Ibid.

[iv] Meeeeeeeeh. We use this term with totally vanilla ambivalence.

[v] Source: FactSet, as of 2/25/2015. FTSE 100 Total Return Index, as of 10/31/2007.

[vi] Source: FactSet, as of 2/25/2015. FTSE All-Share x Investment Trusts Total Return index. From 9/4/2000 - 2/24/2015 and 10/31/2007 - 2/24/2015.

[vii] Source: FactSet, as of 2/25/2015.

[viii] Source: FactSet, as of 2/25/2015. Nikkei 225 Price index in USD. From 3/31/2000 - 2/23/2015. And also trivia.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News Bourse : pourquoi l’impact de la guerre en Iran sera moins important que prévu – par Ken Fisher2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 4/1/2026

New to Fisher? Call Us.

Contact Us Today