Personal Wealth Management / Market Analysis

Flashing Perspective on Eurozone Manufacturing

Manufacturing weakness takes attention away from the eurozone’s still-growing services sector.

Amid last week’s US yield curve inversion chatter, weak survey data out of Europe added to the dour mood. IHS Markit’s March flash manufacturing purchasing managers’ indexes (PMIs) for the eurozone—and Germany in particular—stoked further worries about slowing global growth. In our view, these concerns are overwrought—especially when you put manufacturing data in their proper context.

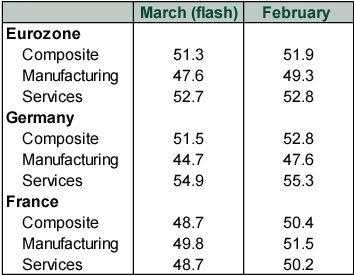

Across the board, March’s flash numbers trailed February’s.

Exhibit 1: IHS Markit Recent PMIs

Source: FactSet, as of 3/25/2019.

However, this doesn’t necessarily mean the eurozone expansion is faltering. PMIs are monthly surveys reporting how many businesses expanded. Readings above 50 mean the majority reported growth; readings below 50 imply contraction. Though PMIs are timely snapshots, they aren’t perfect.[i] They estimate only growth’s breadth, not its magnitude. Moreover, in surveys, sentiment can affect the numbers more than in “hard” economic datasets measuring output quantity or value.

Still, headlines treated March’s results as more proof of a wobbling global expansion and brewing troubles in Germany. The numbers are consistent with recent weaker industrial data in the eurozone and across the developed world.

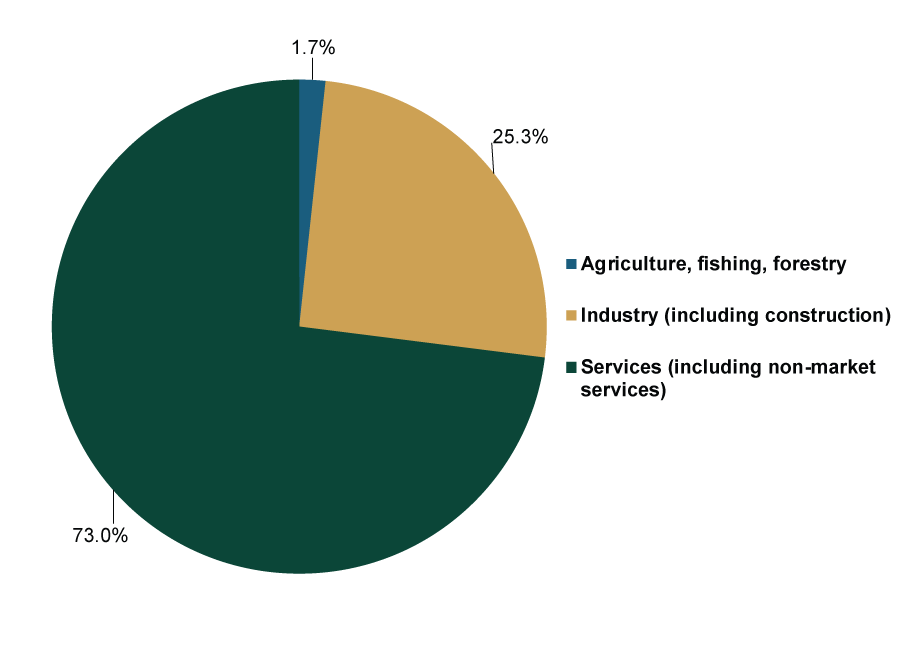

We won’t argue all is rosy in factory land, but the concern seems disproportionate to the actual economic impact. For most developed world nations—including those in the eurozone—the services sector, not heavy industry, comprises the majority of GDP. This is true in supposed industrial powerhouse Germany, where only about one-fourth of GDP comes from manufacturing.[ii] Hence, services industries have a much larger influence on GDP’s direction and magnitude than manufacturing.

Exhibit 2: Eurozone 2017 GDP, Sector Breakdown

Source: ECB and Eurostat, as of 3/22/2019.

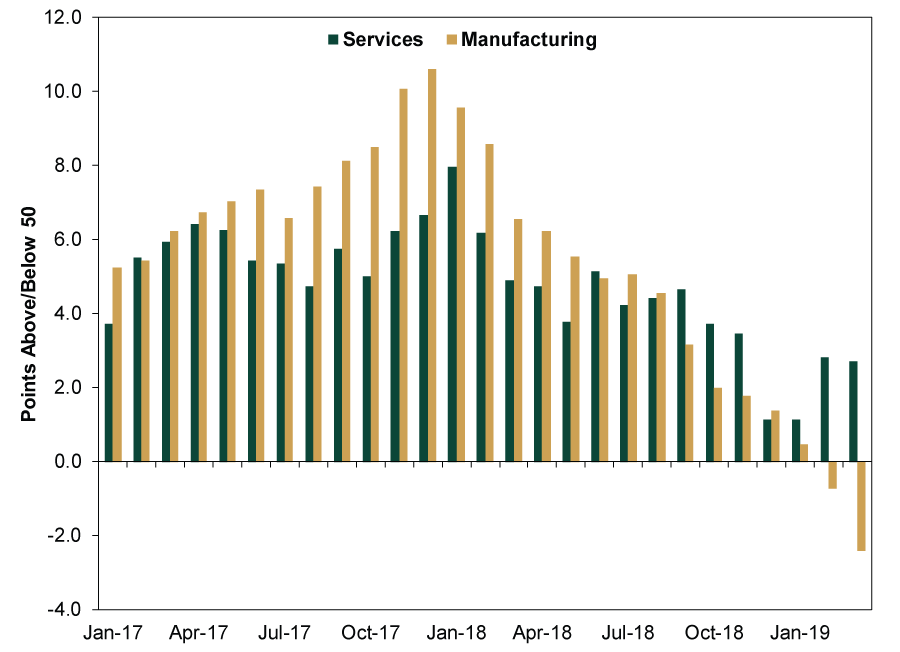

March’s flash services eurozone PMI signals growth—as it has for years. Moreover, the services New Orders subindex accelerated in March. Today’s orders are tomorrow’s production, suggesting the eurozone’s biggest industry likely continues expanding in the near future, driving growth overall. (Exhibit 3) Consider Germany, the eurozone’s largest economy. Despite the German flash manufacturing PMI hitting a six-and-a-half year low, IHS Markit acknowledged: “The domestic market remains strong, which continues to be reflected in wage pressures and robust growth across the services sector of the economy…” This strength may go little-noticed by financial media, but it has existed for years—reason to be bullish, in our view.

Exhibit 3: Underappreciated Eurozone Services Growth

Source: FactSet, as of 3/22/2019. IHS Markit eurozone manufacturing and services PMIs, January 2017 – March 2019 (flash).

Moreover, the eurozone’s manufacturing weakness seems likely to be short-lived. Weak Chinese private sector demand, driven by the government’s crackdown on the shadow banking industry, is likely the primary culprit, as evidenced by the large drop in new export orders. As we recently explained in our commentary, “Some Perspective on the Alleged 'Industrial Recession,'” the Chinese government’s efforts to rein in private lenders turned the screws on China’s private sector, starving them of capital—driving a sharper-than-expected slowdown. Weakening Chinese demand hurt exporters globally. However, China recently announced a slew of fiscal and monetary stimulus measures to help boost domestic demand and channel funding to its millions of small and midsized firms, the country’s economic engine. While stimulus typically takes time to work its way through the economy, we believe it will help Chinese demand recover—which should boost eurozone exports. Outside weak Chinese demand, auto sector weakness—driven by the EU’s new auto emission standards—has remained a headwind for the past several months. But, recent industry reports suggest this headwind may finally be dissipating. With the eurozone economy likely to keep climbing thanks to its services- and consumption-based growth, a manufacturing bounce-back could help boost sentiment—which remains far more dour than warranted, in our view.

[i] IHS Markit’s “flash” estimates typically reflect about 85% - 90% of total survey responses.

[ii] Source: DeStatis, as of 3/25/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis CPI Sheds Light on Britain’s Price ‘Cap’ Conundrum2026-05-20

-

Market Analysis The Investment Implications of Record-Low Consumer Sentiment2026-05-19

-

Market Analysis More Positive Surprise in Japan’s Q1 GDP2026-05-19

-

Behavioral Finance Investing Lessons From the Indianapolis Motor Speedway2026-05-18

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today