Personal Wealth Management / Market Analysis

No Silver Bullet

Silver is spiking, but history shows investors don’t get much from chasing shiny returns.

Silver is up 17.5% year to date,[i] nearly matching gold and leading some pundits to suggest the lesser precious metal makes a better investment due to its supposed relative value and safe haven characteristics. We touched recently on why gold isn’t great as a long-term investment (or short-term portfolio hedge), but with silver squeaking into the spotlight, we should note it isn’t either.

As Exhibit 1 shows, silver has its (occasional) moments, but they are few and far between. The last time silver seemingly garnered so much attention was in 2011, but it was a flash in the pan. Prior to that, silver spiked in 1979. Yes, there was double-digit inflation then (notably absent now), which precious metals allegedly hedge against. (Spoiler alert: They don’t actually do so, at least not reliably.) But the Hunt Brothers were also trying to “corner” the silver market at the time—that is, buy up so much silver that they would control supply—and the price. Which, it didn’t work.[ii]

Exhibit 1: Quick, Silver!?

Source: FactSet, as of 9/12/2019. Dollars per troy ounce of silver, 1/1/1970 – 9/11/2019.

2011’s run was also eye-popping, but with the hallmarks of a bubble. It, too, didn’t last. Then, the Fed was ramping up its second round of quantitative easing, sparking fears it would ignite runaway inflation. Many saw silver as a cheaper, more accessible hedge than gold—and one with more potential given silver’s wider range of industrial uses. Like most bubbles, expectations far exceeded reality. Outside those two episodes, silver has mostly languished over the last 50 years.

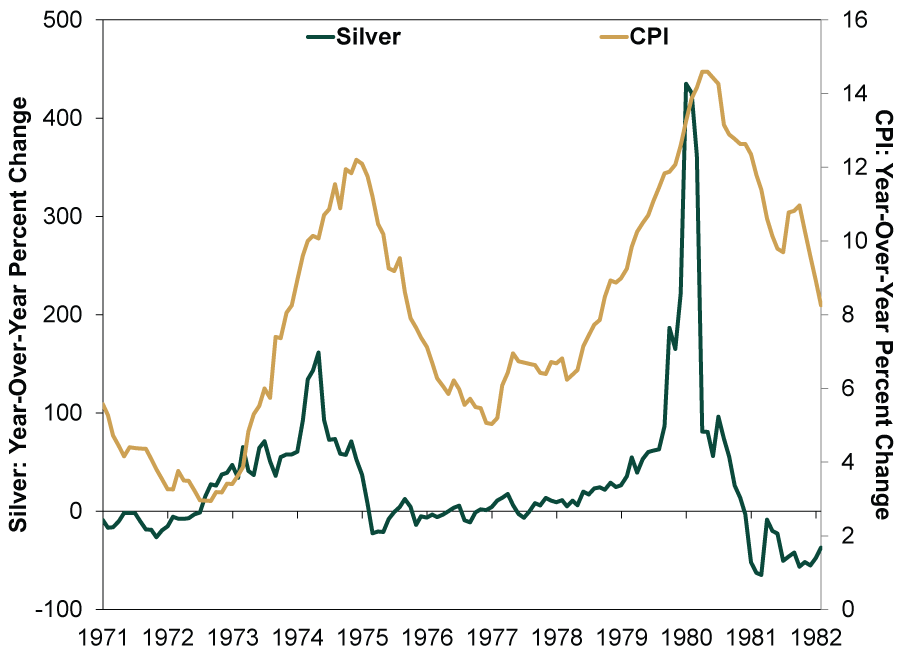

The alleged reasons to own silver today still don’t hold up. Snapping up silver as an inflation hedge seems quite odd to us, considering fast-rising inflation doesn’t look imminent. Fast inflation generally requires fast-rising money supply. This seems difficult to envision when most major yield curves globally are flat or slightly inverted. This isn’t the sort of environment where broad money supply surges. Two, like gold, silver is a poor inflation hedge. As Exhibit 2 shows, the CPI inflation rate was in the double digits during the mid-1970s. While silver did well initially, it fell in 1975 – 1976 when inflation was still running hot. In 1980, when CPI rose 12.4% y/y, silver fell -51.9%.[iii] Not quite how an inflation hedge should behave, in our view.

Exhibit 2: As an Inflation Hedge, Silver Doesn’t Deliver

Source: FactSet and Federal Reserve Bank of St. Louis, as of 9/5/2019. Dollars per troy ounce of silver and headline consumer price index (CPI), using month-end data, January 1971 – December 1981.

Silver is just a commodity. Like any other, its price depends on supply and demand in the mid to longer term, with sentiment-driven fluctuations in the near term. Besides bullion sitting in a vault somewhere,[iv] silver is used more than gold, mostly for electronics (switches and circuits), its reflective properties (solar panels and mirror coatings) and for purification (as an antibacterial disinfectant). The World Bank puts 2018 silver consumption around 29.3 thousand tons, around where it was the prior few years.[v]

On the supply side, miners produced 24.3 thousand metric tons of silver in 2018, with another 4.3 thousand tons recycled for reuse, also according to the World Bank.[vi] So total new silver supply last year was about 28.6 thousand tons, down slightly from the 29-plus thousand ton production (and recycling) levels the previous few years.

With demand higher than supply in 2018, how did that work out for silver’s return? Not so great. Silver fell -8.3% last year.[vii] Now, that is just one year, but we point it out for two reasons. First, demand exceeding supply doesn’t necessarily equal higher prices in any given year. This shouldn’t be too surprising, since markets are forward-looking and influenced by sentiment in the near term. Second, and more critically in our view, a good chunk of silver’s demand is for investment purposes. The World Bank estimates this at around a fifth of “consumption” the last few years. But silver in and of itself isn’t a productive asset—it doesn’t generate earnings—making sentiment a key driver. Silver may see speculative bursts now and then, but it lacks long-term growth drivers.

Sentiment is slippery—impossible to time. Without a big supply disruption (will anyone corner the market soon?) or broad demand drivers others don’t see, we don’t think silver makes much sense for long-term investors.

[i] Source: FactSet, as of 9/12/2019. Dollars per troy ounce of silver, 12/31/2018 – 9/11/2019.

[ii] They got to about two-thirds of all privately held silver on earth.

[iii] Source: FactSet and Federal Reserve Bank of St. Louis, as of 9/5/2019. Dollars per troy ounce of silver and headline consumer price index (CPI), December 1979 – December 1980.

[v] “Commodity Markets Outlook,” Staff, World Bank, April 2019. https://www.worldbank.org/en/research/commodity-markets

[vi] Other figures differ slightly, for example: the US Geological Survey and the Silver Institute. Also note: 1 million troy ounces converts to 31.1034768 metric tons.

[vii] Source: FactSet, as of 9/5/2019. Dollars per troy ounce of silver, 12/31/2017 – 12/31/2018.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The Golden Paradox2026-03-24

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today