Personal Wealth Management / Economics

So Much for Runaway UK Inflation

Lookie there, the weak pound didn’t wreak havoc after all.

Three years ago, when Meghan Markle was a working television actress and Baby Yoda wasn’t even a glint in Lucasfilm’s eye, pundits seemed collectively sure of one thing: With the British pound at generational lows following the Brexit vote, inflation was sure to skyrocket and torpedo the UK’s economic expansion. As CPI inched up in late 2016 and 2017, the coverage got steadily noisier, and we risked running out of creative ways (and charts!) to explain why the fear was likely overblown. So it was with a smirk and a chuckle that we greeted Wednesday’s big non-Megxit UK news that inflation hit … wait for it … a three-year low in December. At just 1.3% y/y, headline CPI is now below most central banks’ inflation targets. Not to say we told you so, but chalk this up as yet another example of why investors shouldn’t accept headline fears at face value.

The logic behind expecting higher inflation after the pound plunged, at a surface level, was sound enough. When your currency weakens, it can raise the price of imported goods, presuming exporters want to preserve their own profit margins and demand at home is strong enough to support a price increase. The UK imports a ton of food and consumer products. But as we explained at the time, extrapolating this to perma-high inflation seemed wrong. For one, Japan’s recent experience proved currency fluctuations affect export prices much less than people presume. Two, the CPI basket includes goods and services, which are more insulated from currency movements. Three, the inflation rate is the year-over-year change in the CPI index. So even if the pound stayed at 2016’s lows, the impact on prices wasn’t likely to last much longer than a year, as the weaker pound would soon be part of the new baseline. Back in 2011, CPI topped 5% briefly, alongside a weak pound. Prices started easing long before the pound enjoyed a sustained recovery. It was simple math.

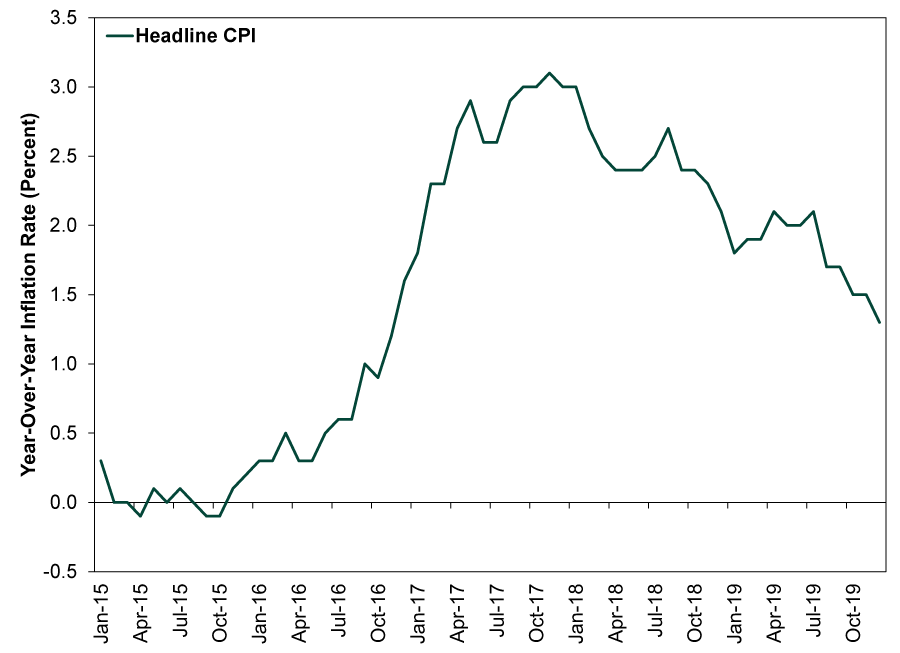

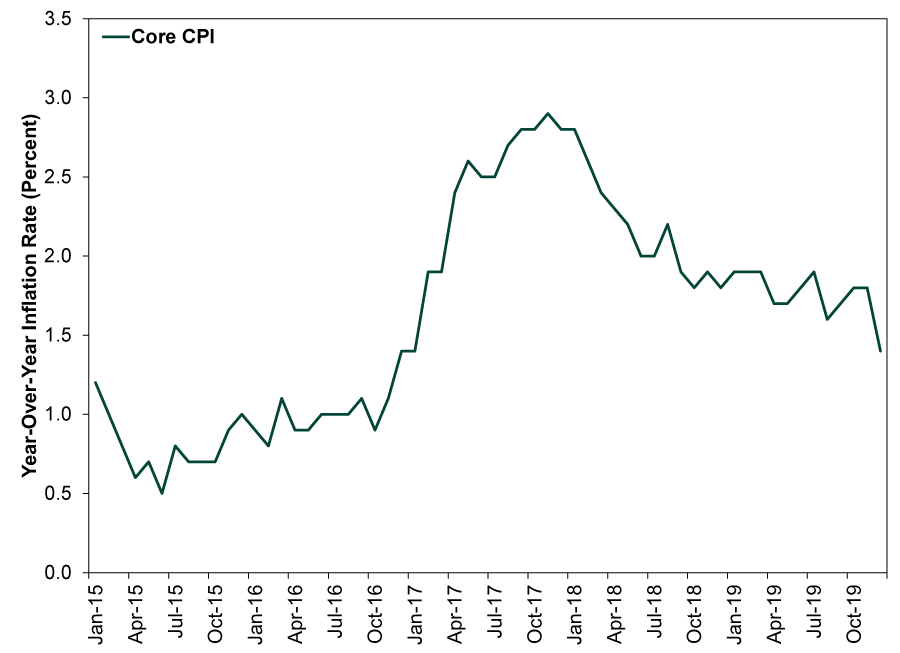

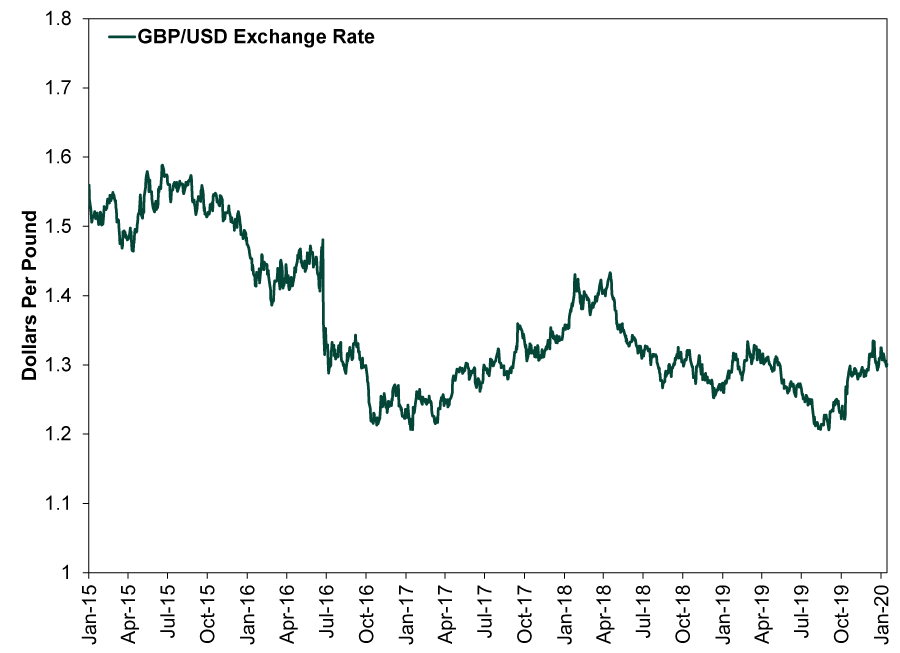

That is largely how things played out. The headline inflation rate peaked at 3.1% y/y in November 2017, then began a fitful slide to December’s 1.3%. Excluding energy and seasonal food, “core” inflation peaked at 2.9% in November 2017 and finished 2019 at 1.4%. Note that this improvement occurred even though the pound retested its lows last summer and is still quite a bit weaker than before the Brexit vote.

Exhibit 1: Inflation Didn’t Run Away

Source: FactSet, as of 1/15/2020. UK Consumer Price Index, year-over-year percentage change, January 2015 – December 2019.

Exhibit 2: Neither Did Core Inflation

Source: FactSet, as of 1/15/2020. UK Consumer Price Index Ex. Energy and Seasonal Food, year-over-year percentage change, January 2015 – December 2019.

Exhibit 3: The Pound Stayed Rather Weak

Source: FactSet, as of 1/15/2020. US dollars per British pound, spot rate, 1/1/2015 – 1/14/2020.

This isn’t mere trivia. When people feared high inflation, the narrative held that high prices would sink consumer spending, ending growth in the UK’s consumer-driven economy. Echoing this expansion’s early days, this was the impetus behind nonstop post-Brexit referendum calls for the UK to “rebalance” its economy away from consumption and beef up exports. If it didn’t, many theorized UK stocks would suffer as the country sank into recession or stagflation.

But that didn’t happen either. Consumer spending hasn’t fallen in any quarter since the Brexit referendum. GDP has contracted just once, in Q2 2019—an after-effect of the shifting Brexit deadline, unrelated to inflation. In 2017, as prices rose, consumer spending grew 1.8%.[i] GDP grew 1.9%, matching 2016’s growth rate.[ii] UK stocks didn’t take the world by storm, but they didn’t crash either. Actually, in 2017, they basically matched global returns.

So the next time you hear about some economic development bringing a catastrophic chain reaction, take a few minutes to think it all the way through. Trace the entire chain of logic. See if each link holds up. Explore potential counterarguments. See if they have more merit. See if similar developments elsewhere in the world had a similar impact. Read MarketMinder! And remember the case of the UK’s not-so-runaway inflation.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Economics A Summertime Check-in on US Consumers2026-07-23

-

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today