Personal Wealth Management / Market Analysis

Some Things Are Happening in Brazil

With political intrigue and a putrid economy, why are Brazilian stocks up in 2016?

Brazil is having a moment right now. Many Brazilians are angry and calling for the president's impeachment. That president seems to be trying to protect her predecessor from criminal charges related to a huge corruption scandal that has rocked the country for the past two years. The economy is a mess. And yet, after a -17% drop to start 2016, a strong rally dating back to January has Brazilian stocks up year-to-date .[i] What gives? There is no simple answer, but current developments in Brazil demonstrate how political, economic and sentiment drivers all intertwine, teaching an important lesson: Markets sometimes do what seems counterintuitive, especially over short periods.

Let's start with the big story in Brazilian politics. The corruption scandal involving Brazil's state-owned energy behemoth Petrobras-dubbed "Operation Car Wash"-has gradually ensnared some of Brazil's biggest public figures over the past two years. Historically, Brazil's politicians have largely escaped justice for their transgressions. The Car Wash probe may mark a major shift in this leniency (we will explain the "may" momentarily), as investigators have doggedly pursued more and more powerful figures-CEOs, Senators and other politicians. Earlier this month, authorities snared their biggest figure yet: Luiz Inácio Lula da Silva (more commonly known as Lula[ii]), Brazil's former-and very popular-president.

Against this backdrop, current President Dilma Rousseff is facing calls for her impeachment based on a trifecta of allegations: that she was involved in Petrobras' underhanded dealings; used illicit funds to finance her 2014 reelection campaign; and mismanaged federal accounts. Though an initial impeachment movement failed in December 2015,[iii] chatter has renewed, particularly after her mentor, Lula, got dragged into the scandal. This week, Rousseff offered Lula a cabinet position as her chief of staff-given his still-substantial popularity, Rousseff may be hoping her mentor can convince Congress to stave off impeachment proceedings. However, many interpreted the appointment as an attempt to protect Lula from the Justice Department's reach, as only the Supreme Court can charge cabinet members with crimes. That interpretation was seemingly confirmed after secretly recorded conversations were released on Wednesday, prompting a judge to suspend Lula's nomination. (This is why we said Car Wash "may" mark a major shift away from Brazilian politicians' historical tendency to dodge justice.) But in the latest development, Congress took the first step in the impeachment process on Thursday by forming a special committee.

The political situation would be an interesting story about judicial independence's evolution in an emerging country were it not for the economic situation. Brazil's commodity-reliant economy is struggling desperately, and many figure reforms and stimulus can't pass with the government embroiled in scandal. GDP contracted -3.8% in 2015 (-1.4% q/q in Q4 2015), Brazil's worst annual contraction since 1990-a far cry from when the country was poised to be a "global player." Though industrial production rose 0.4% m/m in January, it's one small uptick after seven straight monthly declines. The mining subsector, which comprises a large swath of Brazilian economic activity, slipped -2.7% m/m, the fourth straight fall. Other gauges reflect the country's deep struggles. The services sector plunged -5.0% y/y in January, with all subsectors falling. Retail sale volumes similarly dropped -1.5% m/m (-10.3% y/y)-a sign of struggling Brazilian consumers. One of the major headwinds consumers face: double-digit inflation-the highest in over a decade-and the corresponding high interest rates.

With all the political and economic turmoil, Brazil's stock market outperformance may seem odd. The MSCI Brazil is up 15.3% year-to-date after 2015's -41.4% plunge.[iv] Do markets know something about Brazil that the headlines and data are missing? Maybe yes, maybe no. Stocks often bottom before the economy does, and with all the well-known turmoil in Brazil right now, it could be a "blood in the streets" moment. However, Brazilian stocks' recent outperformance may be a false dawn, too. There seems to be a lot of optimism and hope simply removing Rousseff will flip Brazil's fortunes, presuming a successor could succeed in enacting reforms necessary to aid the economy. It looks slightly reminiscent of regime changes elsewhere in Emerging Markets, where a new government generates excitement, driving temporary outperformance. But staying power is the real question. See India: though current Prime Minister Narendra Modi's administration seems to be doing better at meeting campaign promises than his predecessors, the country has a long legacy of talking big but delivering lackluster results.

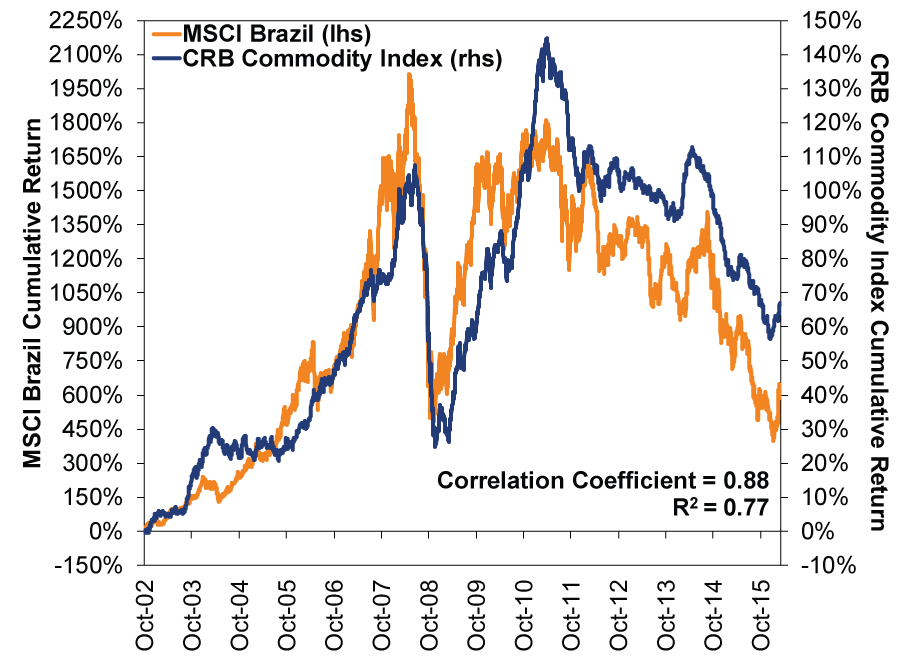

In Brazil's case, simply changing the president vastly oversimplifies the country's issues. For one, impeachment proceedings, should they advance, likely won't be resolved quickly-they may drag on for a long while, adding to uncertainty. And even if the most high-minded, noble politician[v] replaced Rousseff, he or she couldn't wave their hand and enacts ensible reforms. Brazil's Congress is fractured and gridlocked, so consensus-building would be pretty difficult. Consider, also, how closely Brazil's economy and markets track commodity prices. During the commodities-led bull market from 2002-2007, Brazil returned an astounding 1454%.[vi] By comparison, the S&P 500 rose 101% over the same period.[vii] Similarly, Brazil mirrored commodities' bounce-back following the 2008 bear market. However, the country's equities also peaked right around commodities' most recent peak in early 2011-it has been a slide since then. (Exhibit 1)

Exhibit 1: Brazil Tracks Commodities Pretty Closely

Source: FactSet and Standard and Poor's, as of 3/17/2016. MSCI Brazil and S&P GSCI Index, from 2/28/2006 - 3/15/2016. Correlation coefficient and R2 are statistical measures showing how related two items are.

In countries needing liberalization, economic reforms influence relative returns. But you can't look at this in a vacuum-you must note cyclical drivers, too, as they often swamp structural issues in the short run. Brazil's situation today is a timely, if extreme, reminder of cyclical drivers' power-an important consideration for investors to remember. Reforms mostly affect stocks through the gap between actual reforms and expectations of reform. We've argued for years Japanese outperformance was built on sand, given high expectations for Abenomics and the likelihood it would underdeliver in the reform category. Absent that, Japan needs strong cyclical tailwinds to drive growth, which it lacks. Brazil is in the same boat presently, with investors' impeachment hopes up, and no clear alternative to Rousseff in place with a mandate for big reform. Meanwhile, the cyclical backdrop for commodity-heavy nations is the linchpin, and oversupply remains presently.

For investors, Brazil serves as a prime example of capital markets' complexity. There are so many different drivers at work simultaneously, and what the media highlights is important, but it also doesn't tell the whole story. The Rousseff-Lula intrigue will garner the most attention, but a gridlocked legislature likely impacts what the government can do much more. "Brazil's deepest recession since the 1930s" makes a great headline but doesn't mean Brazil will continue struggling-though a persistent global commodity glut might. The rally back is instructive in the sense that it shows the near-term influence of sentiment's often counterintuitive nature. But we would suggest the next market lesson Brazil teaches is the unsustainability of sentiment-driven rebounds when forward-looking fundamentals stink.

[i] Source: FactSet, as of 3/16/2016. MSCI Brazil Index with net dividends, 12/31/2015 - 3/15/2016.

[ii] Like their world-famous soccer counterparts (see: Pelé, Ronaldo, Kaká, Neymar), Brazilian politicians seem to prefer single-word name as well.

[iii] The Supreme Court called it unconstitutional.

[iv] Source: FactSet, as of 3/16/2016. MSCI Brazil index with net dividends, 12/31/2015 - 3/16/2016. Returns are in US dollars.

[v] An oxymoron, we know.

[vi] Source: FactSet, as of 3/16/2016. MSCI Brazil from 10/09/2002 to 10/9/2007.

[vii] Source: FactSet, as of 3/19/2015. S&P 500 Price Level from 10/09/2002 - 10/09/2007.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today