Personal Wealth Management / Market Analysis

Survey Says … Growth!

You might not know it from the media coverage, but January PMI surveys show the US and UK services sector grew.

In today's upside-down financial press, what's fair seems to be foul. For instance, a January survey reported more businesses grew than didn't in the US' robust "non-manufacturing" sector, which includes industries ranging from Retail Trade and Mining to Health Care and Construction. The UK's own burgeoning services sector experienced a similar January. Sounds grand, right? Not if you read the news coverage. Headlines bemoaned services growth at its slowest pace in two years in the US, while another pundit declared the "UK's economic recovery is a shadow of its former self." All this left us a wee bit confused, especially when the media attempted to pin stock market volatility on reported output last month. While old January data don't mean much for forward-looking stocks, this also overlooks the larger point: The latest non-manufacturing and services PMIs show growth. That so few recognize this speaks to how dour sentiment is.

For the US, the Institute for Supply Management's Non-Manufacturing Purchasing Managers' Index (PMI) slowed to 53.5 in January-down from December's 55.8. In the UK, Markit/CIPS' Services PMI rose a tad from December's 55.5 to 55.6. PMIs are business surveys asking whether activity in various categories rose or fell in a given month, and readings over 50 indicate more respondents grew than contracted once all the categories were aggregated. While PMIs have limitations-they don't tell you the magnitude of growth and they're surveys-many use them as a quick-and-dirty proxy for business growth since they hit within days of month-end.

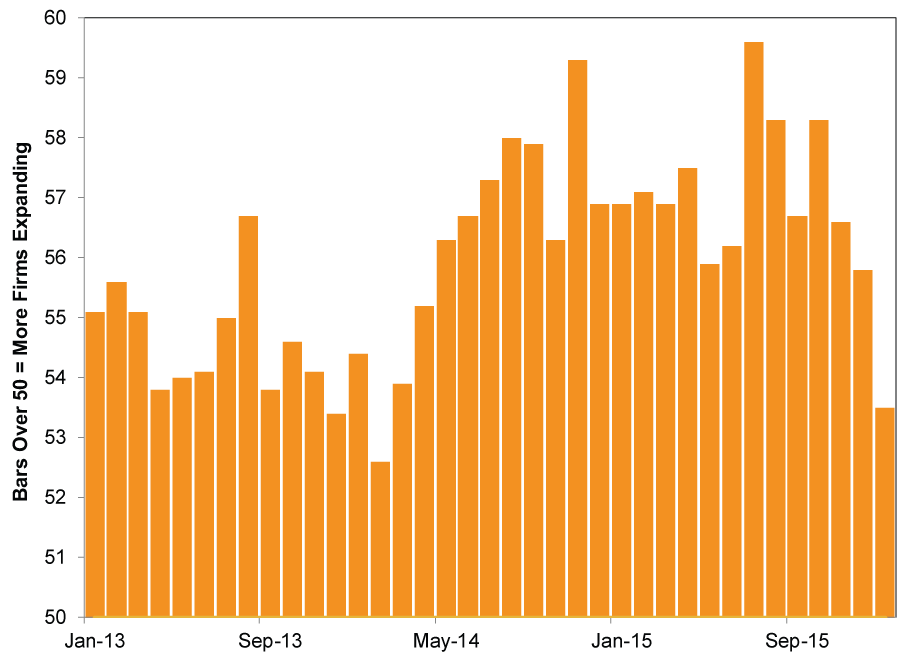

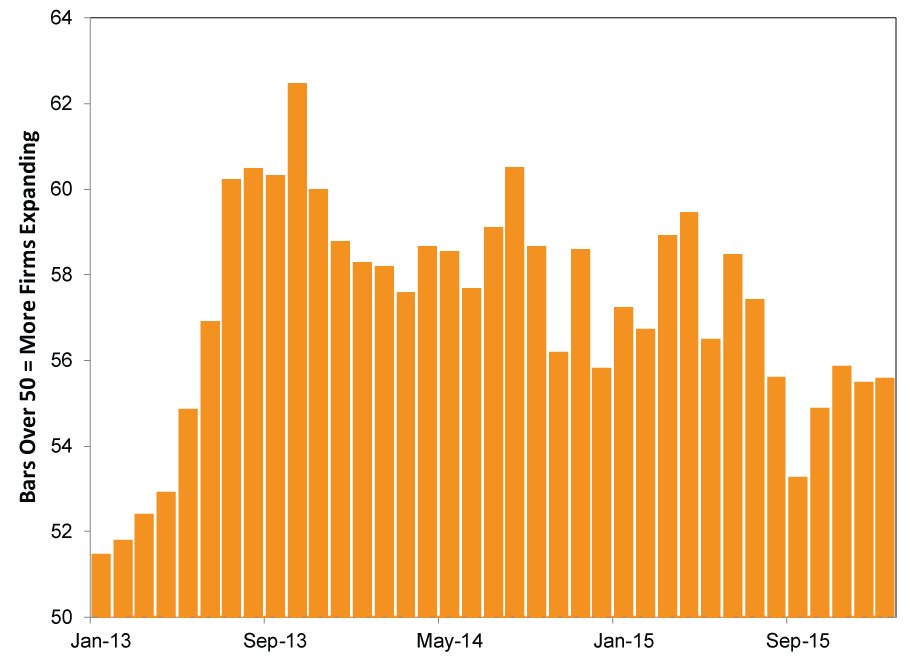

Considering both surveys were well in expansion, we're a little perplexed by the near-uniform gloom. Even though ISM's non-manufacturing PMI is at its slowest level since February 2014[i], it still indicated growth-as does Markit/CIPS' Services PMI. And while monthly data can be pretty darn volatile, the longer-term trends suggest nothing out of the ordinary for both the ISM and Markit/CIPS PMIs. (Exhibits 1 and 2)

Exhibit 1: ISM US Non-Manufacturing PMI Since January 2013

Source: St. Louis Federal Reserve, as of 2/3/2016.

Exhibit 2: Markit/CIPS UK Services PMI Since January 2013

Source: FactSet, as of 2/3/2016.

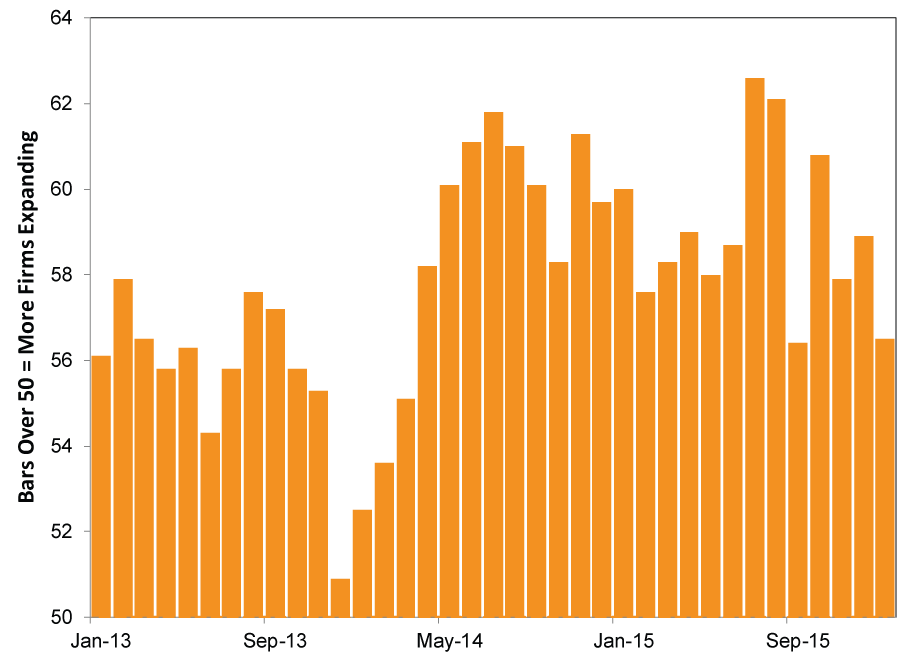

Most confusing? Attempts to pin early-Wednesday volatility on these surveys. The weakest parts of the ISM survey were employment and output-late-lagging and coincident, respectively. Stocks look forward, and the only really meaningful forward-looking piece of PMI surveys is the new orders component. Today's orders are tomorrow's production-and that's economic growth, in a nutshell. Both Markit/CIPS and the ISM surveys show new orders are chugging along. Markit/CIPS reports that "new businesses rose at the sharpest rate since last July" for its UK Services PMI. The ISM's Non-Manufacturing New Orders subindex hit 56.5, suggesting future production-ergo, more growth- is likely. (Exhibit 3) Selling stocks based on what already happened last month, without any regard for the one piece that says things look good ahead would be odd. Very odd. We'd be shocked if people did it, which speaks to the pitfalls of pinning volatility on any one thing.

Exhibit 3: ISM Non-Manufacturing New Orders Index Since January 2013

Source: St. Louis Federal Reserve, as of 2/3/2016.

It also speaks to the perils of taking media spin on economic data at face value. Consider the following quotes about ISM's report:

Service Industries in U.S. Grow at Slowest Pace in Two Years:

"Manufacturing weakness seems to be spreading to the services side of the economy. There's definitely no decoupling here. It's a shaky outlook."

US Recession Odds Rise to 40 Percent: Deutsche Bank Economist

"The service side follows the manufacturing side. I just don't look at the fact that manufacturing is a small part of the economy. It doesn't matter. If there's anything we learned in the last business cycle, it's size doesn't matter."[ii]

Now, as we wrote on Tuesday, we find the handwringing about the ISM's Manufacturing report a bit overstated as well, especially since the current contractionary streak is pretty small, miles away from what you get in a recession. Plus, new orders rose-one data point, but noteworthy, and manufacturing isn't a leading indicator, nor does it have some inherent gravitational pull on services. But beyond that, these quotes seem far removed from those who are actually surveyed: the businessesthemselves. Straight from the January 2016 Non-Manufacturing ISM Report on Business:

"We have experienced a slight increase in business activity since the start of the new year. Our new job orders have increased about 10 percent and the job awards about 12 percent." (Professional, Scientific & Technical Services)

"Sales have improved. We are feeling more optimism, but remain concerned about the impact of global unrest." (Retail Trade)

Granted, these are just two quotes. Some businesses-like those in Mining-likely feel much more pressure than others. But reality also isn't as bad as fears the US economy is teetering toward recession.

Yes, in January, it appears service sector growth may have slowed. But slowing growth is not contraction-a point often lost by pundits, particularly amid market volatility. But it has not been lost in this bull market and expansion, which have proven time and again that slowing growth doesn't squash stocks. Ultimately, the largest segments of the UK and US economies are growing just fine, despite how pundits try to spin it. In our view, there is a big gap between perception and reality-a bullish disconnect. As folks start appreciating the good, stocks should grind higher.

[i] For those scoring at home, this is an entirely arbitrary date that doesn't coincide with recession.

[ii] Actually, the reality is that loan losses on subprime and mortgage-backed securities were too small to render the recession we got. But, mark-to-market accounting magnified them massively to the tune of multi-trillions worth of writedowns. Multi-trillions is not too small.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today