Personal Wealth Management / Market Analysis

Thankful the World Over

There is much to be thankful for, not just in the US, but globally too.

Thanksgiving is an American holiday, a time when we in the States give thanks for the many blessings in our lives. Family. Friends. Health. Turkey.[i] But we have our own Thanksgiving tradition here at MarketMinder: A global celebration of the bullish backdrop underpinning stocks-reasons investors the world over can celebrate right along with Americans, no matter their definition of football.

Overall Positive Political Scene

This year's US midterm elections all but assured continued government gridlock-a positive for stocks many miss. Forget party affiliation. (Especially, we'd advise, at the dinner table.) Whether you celebrated or mourned the Republicans taking the Senate and adding to their House majority, the White House is still controlled by the Democrats-gridlock! The likelihood contentious legislation potentially dinging stocks or the economy becomes law is low, a plus for stocks. Since 1928, 86.4% of midterm election year Q4s-and the following Q1 and Q2 have been positive-well above the average quarter's 67.8% frequency of positivity.[ii] While the identical frequency figure is coincidental, gridlock's positivity is causal.

The UK's political backdrop is also positive. Scotland voted to remain in the UK, mitigating a headwind. Determining further devolution will take time, but this is less of an issue than Scottish independence, particularly from an investor sentiment standpoint. And 2015 is an election year, implying there won't be many major policy shifts. Gridlock in both the US and UK is a plus for two major economies that don't require significant economic reforms.

In the eurozone, France's nominally Socialist government is moving in a market-friendly direction with a pro-business-leaning cabinet and a declaration they won't enact any new taxes next year. Greece saw successes in its privatization program. Spanish labor market reforms are bearing fruit. Wednesday, the lower house of the Italian parliament took a step toward labor reforms. While none of these developments alone are revolutionary or transformative, they likely benefit the region's competitiveness some and are a structural plus.

The Global Economy's Healthy

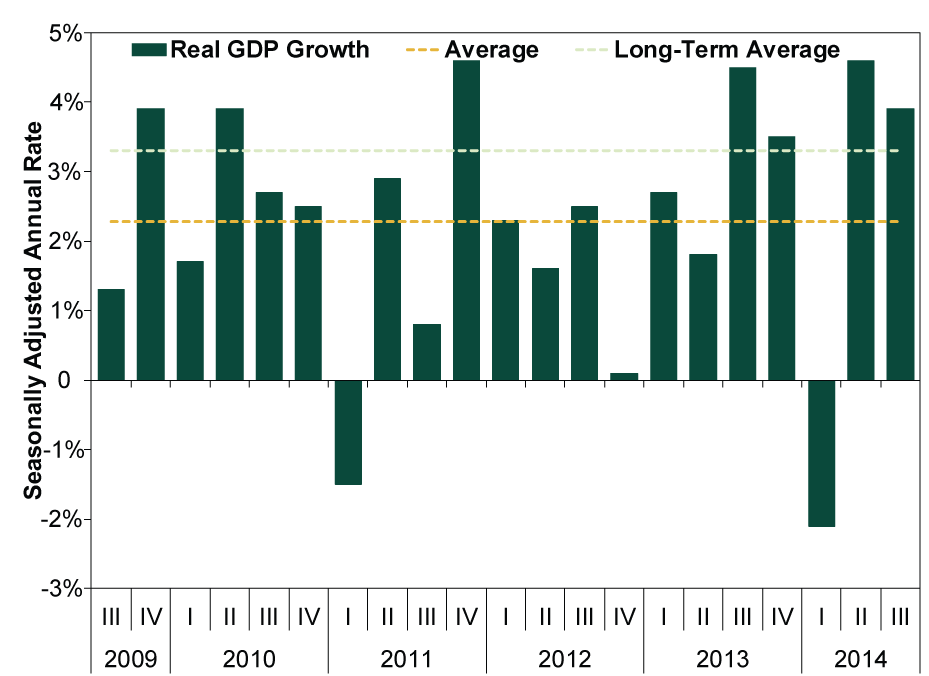

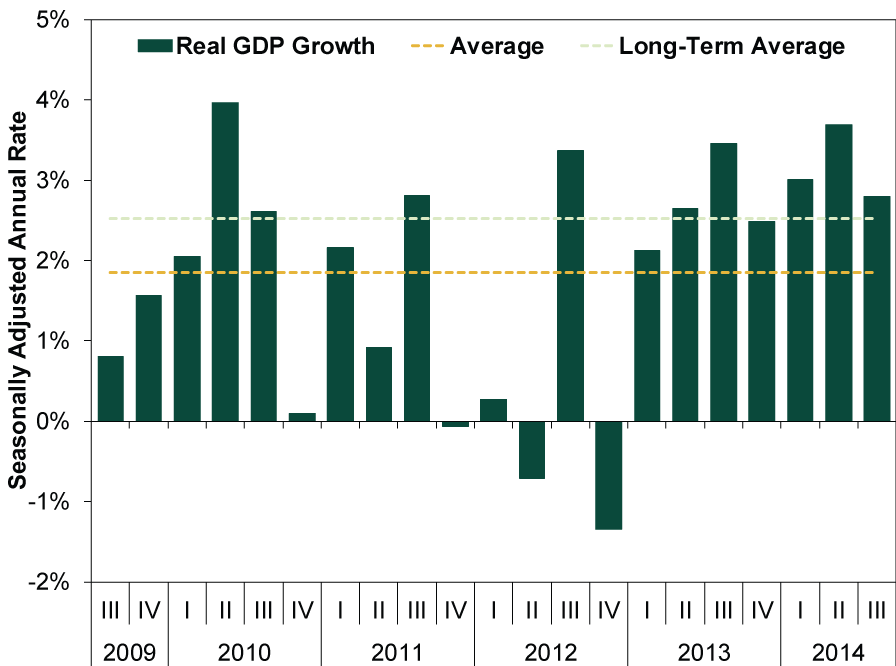

The UK and US economies have been leapfrogging each other in recent quarters for the title of fastest-growing developed economy. The second estimate of US Q3 GDP showed upwardly revised growth, to a 3.9% seasonally adjusted annual rate from 3.5%, led by consumer spending and business investment. The UK posted a still-respectable 2.8% annualized growth in Q3, with consumer spending leading. Both economies have grown at clips exceeding their long-term averages in four of the last five quarters (Exhibit 1 and Exhibit 2).

Exhibit 1: US GDP Growth

Source: US Bureau of Economic Analysis, as of 11/26/2014. US real GDP growth Q3 2009 - Q3 2014. Long-term average, Q2 1947 - Q3 2014.

Exhibit 2: UK GDP Growth

Source: Factset, as of 11/26/2014. UK real GDP (seasonally adjusted, annualized), Q3 2009 - Q3 2014. Long-term average, Q2 1955 - Q3 2014.

This trend doesn't seem to be abating. The Conference Board's October US Leading Economic Index (LEI) rose 0.9%, the eighth rise in the past 10 months. In its 50-year history, no US recession has begun while LEI was rising. And with only one negative contributor in October's report (stock prices[iii]), the US looks poised to continue growing. While September UK LEI fell a bit (-0.4%), it's the first dip since January and the more-telling components (e.g., the yield spread) were still positive.

October manufacturing and Services purchasing managers' indexes (PMIs) are expanding for both the US and UK, with forward-looking new orders indexes expansionary across the board. US and UK retail sales both rose in October, 0.3% and 0.8%, respectively. While November eurozone flash PMI slowed, it remains expansionary, alluding to more tepid-but-positive growth after Q3's 0.2% q/q eurozone GDP growth. Conditions in the currency bloc aren't robust, but they are better than dour expectations-good enough for stocks, in our view.

Mixed Bag of Sentiment

Despite these reasons to be bullish, investor sentiment, while warming, is still middling. Valuations aren't extreme, showing a lack of euphoria. And skepticism hasn't totally vanished. Consider:

- China hard landing fears, now more than four years old, remain.

- The eurozone succumbing to a lost decade, a deflationary depression or worse.

- Japan's very country-specific issues somehow spilling globally.

These are all bricks in today's Wall of Worry. Most of them are old fears, cud long chewed over by investors-sapping their surprise power and ability to knock the bull off course.

QE Is Done in the US and UK

After almost six years, the Fed announced it would end its quantitative easing (QE) bond buying this month-a long-awaited positive, in our view. As we've said often, QE has been an economic depressant, not a stimulant. The Fed sought to incentivize borrowing by pushing down long-term interest rates. But lower long rates flatten the yield curve, making lending less profitable for banks. It isn't surprising loan and broad money supply growth have been slow in this expansion. And though many feared QE's end would be a negative-some even suggested delaying its termination when some slight volatility hit in October-markets have long dealt with the program's conclusion.

When former Fed chair Ben Bernanke alluded to tapering QE in May 2013, long-term interest rates rose-markets anticipated QE's end. Stocks wiggled, in what many labeled a "taper tantrum," presuming this was a small taste of what would come when the taper actually did. But since May 2013, the US market is up 34%. World stocks 22%.[iv] So much for the taper tantrum. Today, despite a year-to-date decline, 10-year rates are still above where they were then. And since January, when tapering actually happened, lending is up.

Shale Oil Revolution

While recently falling gasoline prices have grabbed eyeballs and inspired debate about their merits and pitfalls, overall rising global oil supply-thanks largely to the US's shale oil revolution-has been an overlooked story. The US's shale oil revolution have led to a boom in petroleum exports and fewer imports, lowering global energy prices-a deflationary pressure that isn't negative.

More broadly, the US's shale oil story is a prime example of innovation at work-entrepreneurial spirits who employed new oil extraction techniques were rewarded for the risks they took. It is like mobile computing. Cloud computing. A much more mature, broader-scale version of the 3D printing tale. It is innovation in action, a reminder secular stagnation theories of perma-malaise are bunk.

There is a lot for investors to celebrate this holiday season. So give thanks. Relax. And by all means stop reading this, it's a holiday.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] Tofurky?

[ii] Source: Global Financial Data, as of 11/5/2014. S&P 500 Total Return Index, 12/31/1925 - 9/30/2014.

[iii] You can't forecast stocks with stock returns. Also, we'd note that stock prices included in LEI are the average daily close. The S&P 500 rose in October.

[iv] Source: Factset. S&P 500 total returns and MSCI World Index returns with net dividends, 04/30/2013 - 11/25/2014.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today