Personal Wealth Management / Market Analysis

Timely Takeaways From Q2’s Plunging Earnings

Q2’s S&P 500 earnings season is a timely lesson in how markets work.

Q2’s earning season is wrapping up, and—likely surprising no one—the results were awful. Yet they also weren’t anywhere near as bad as analysts projected before firms began reporting. While we don’t think the big positive surprise is necessarily why the S&P 500 is hitting new highs, we do think it illustrates some important investing concepts.

With 478 S&P 500 companies reporting as of today, blended Q2 earnings—combining actual results and remaining estimates—fell -32.5% y/y, the largest decline since Q1 2009.[i] Yet this was much better than the -44.1% y/y decline analysts expected at June’s end.[ii] In aggregate, actual reported earnings were 22.4% above the latest estimates—a record amount.[iii] The previous record occurred in Q1 2010.

Three sectors reported year-over-year growth in Q2 earnings: Health Care, Utilities and Tech. Unsurprisingly, this is getting heaps of attention as pundits keep touting alleged COVID winners. There is also talk about how COVID-19 has accelerated trends—including cloud computing and drug development—which may benefit some sectors more than others. While that may or may not turn out to be true, guessing at how any event prompts long-term shifts is sheer speculation and, in our view, not a great investing thesis. We think what matters for sector leadership going forward is how more cyclical drivers evolve and how that compares to expectations.

The more significant aspect of Q2’s earnings results, in our view, is the extent of positive surprise across the board: 83% of companies beat consensus expectations, another record and well above the 72% 5-year average.[iv] We think it speaks volumes about the difficulty analysts have had pinning down the exact extent of lockdowns’ damage and just how much sentiment overshot to the downside during the bear market. If ever you needed evidence that bull markets begin in pessimism, we think this is it.

Downward Revisions to Earnings Trailed Stocks

Analysts’ difficulty estimating earnings doesn’t seem too dissimilar to economists’ attempts to pin down GDP’s downturn. While most knew Q2 would be bad, GDP estimates were all over the place—from down less than -1.5% annualized to -67%, per FactSet, as of June’s end.[v] Now, the median forecast, which some take as the “consensus,” wasn’t too far off. Q2’s annualized GDP decline was -32.9% vs. the -32.2% consensus estimate.[vi] But that means half of economists overestimated how bad the quarter would be—a sign of just how depressed sentiment was—which stocks already anticipated.

So it went with earnings. US stocks peaked February 19 and kept plunging until March 23, losing a third of their value.[vii] The record-quick bear market’s onset preceded US lockdowns by a month and ended just a few days after California became the first to issue statewide stay-at-home orders. In less than five weeks, stocks priced in what would become the sharpest economic contraction in history. In a case of uncanny timing, the market’s low point arrived the day before the first piece of data—IHS Markit’s March flash purchasing managers’ indexes—hinted at the economic damage. Markets were efficient enough to be able to extrapolate the economic impact from the lockdowns.

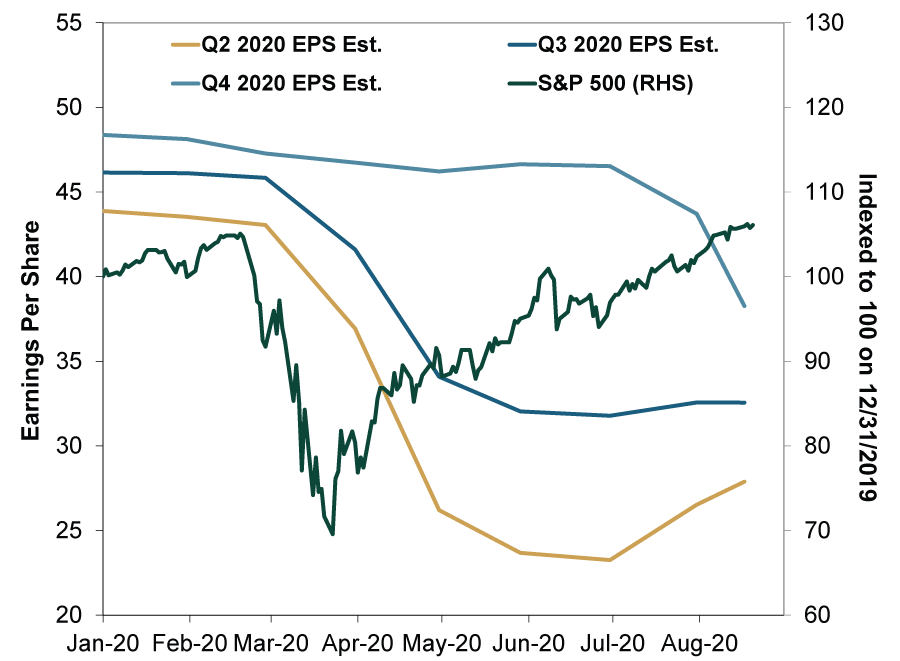

That includes the impact on earnings. As Exhibit 1 shows, the S&P 500’s aggregate Q2 earnings estimate (yellow line) started its big descent in March and continued declining through July. Analysts’ downward revisions were a lagging indicator to stocks (green). Stocks recovered not because they ignored incoming data—still a pervasive narrative and lingering fear for so many—but because they conceived of the bad news before almost everyone. Markets fathomed the extent of the downturn and registered the likely impact, allowing them to look further ahead—past companies’ official results and dire warnings.

Exhibit 1: Stocks Anticipated Plunging Earnings

Source: FactSet, as of 8/20/2020. Analysts’ S&P 500 aggregate consensus earnings estimates for Q2, Q3 and Q4, December 2019 – August 2020, and S&P 500 total return index, 12/31/2019 – 8/20/2020.

With Q2 in the rearview, analysts are refining (read: reducing) their Q3 and Q4 earnings forecasts, as Exhibit 1 also shows. This is leading to talk of a prolonged earnings slump, fueling the stocks are ignoring reality thesis. In our view, this betrays a fundamental misunderstanding of how markets work. Stocks have demonstrated they price widely available information quite efficiently, including analysts’ projections. Q2 illustrated that in spades. Since stocks move mostly on the gap between reality and expectations, year-over-year earnings declines the next couple of quarters shouldn’t present a material speedbump for stocks unless they are hugely worse than expected. We don’t see anything today rendering that likely.

Markets See Eventual Recovery

In our view, stocks are looking further into the future, toward the far end of the 3 – 30-month window they typically assess. When lockdown-induced uncertainty was greatest in February and March, stocks focused on the very near end of that range, with the recession’s depth and length their primary concern. Once they got a general idea of that, they were able to move on, looking to the spring’s reopenings, the summer’s economic green shoots and an eventual recovery to pre-lockdown levels of economic activity. At this juncture, what matters isn’t earnings in Q3 or Q4, but a return to normalcy and growing profits in 2021, 2022 and beyond. We think that is what stocks are looking to now, making it crucial for investors to keep a longer perspective rather than get hung up on backward-looking data’s ups and downs on the way there.

It is one thing to hear stocks are the ultimate leading indicator, but it is another to witness that in action. As Q2’s earnings saga shows, stocks have a remarkable ability to divine what is ahead. So instead of presuming the market must be wrong if stocks are up when news seems bad, remember stocks have generally already considered that bad news and drawn their own conclusions.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

See Our Investment Guides

The world of investing can seem like a giant maze. Fisher Investments has developed several informational and educational guides tackling a variety of investing topics.

Related Resources

-

Politics France Falls Into Political Purgatory … Again2025-09-12

-

Expert Commentary Fisher Investments Reviews Fed Rate Cuts2025-09-12

-

Expert Commentary Should Investors Hold Cash on the Sidelines?2025-09-11

-

Market Analysis Putting Stagflation Claims in Actual Context2025-09-11

Learn More

Learn why 185,000 clients* trust us to manage their money and how we may be able to help you achieve your financial goals.

*As of 6/30/2025

New to Fisher? Call Us.

Contact Us Today