Personal Wealth Management / Market Analysis

Chart of the Day: The Eurozone’s Journey From the Abyss

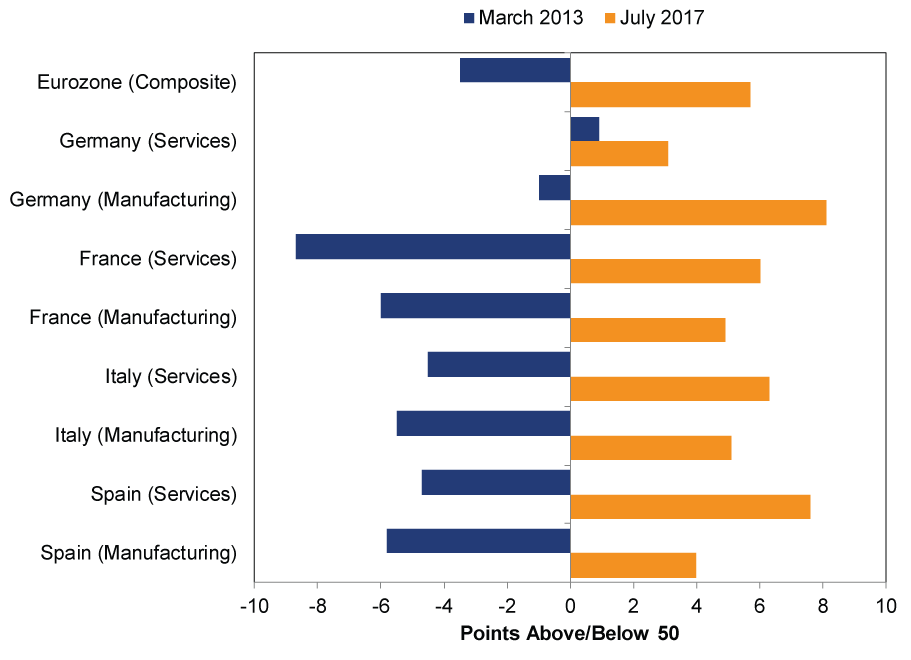

July PMI data show how far the eurozone has come since its recession's end.

After several years of being overlooked, it seems like the eurozone is finally getting a little love from the financial press. Headline writers admit the "Eurozone Recovery Is Even Better Than It Looks" and acknowledge the much-maligned monetary union is leading other developed economies' growth rates. Yet this isn't breaking news: The eurozone has grown 17 straight quarters and the "recovery" moniker has been officially wrong since 2015. While growth hasn't been even-some countries officially entered "expansion" territory more recently than others-it is increasingly broad-based. But the growing awareness is a sign sentiment is improving, which we think should help fuel eurozone stocks.

To highlight how far the eurozone has come, consider how the just-released July purchasing managers' indexes (PMI) figures compare to those from March 2013: the last PMI report before the eurozone began its 17-quarter growth streak.

Exhibit 1: IHS Markit's Eurozone PMIs, March 2013 vs. July 2017

Source: IHS Markit, FactSet, Fisher Investments Research. IHS Markit composite eurozone PMI, Final Services PMI for Germany, France, Italy and Spain and Final Manufacturing PMI for Germany, France, Italy and Spain for March 2013 and July 2017.

As we have written, PMIs aren't perfect econometrics (no stat is). They are monthly surveys showing a snapshot of a country's private sector. Readings over 50 mean more responding businesses grew than contracted that month; readings below 50 suggest more shrank. While PMIs don't show the magnitude of the growth/contraction, they give a quick and rough sense of how different sectors of the economy are doing.

In March 2013, at the depth of the eurozone's recession, most businesses across the eurozone's four big economies were struggling. If the numbers didn't provide compelling evidence, the media hammered the point home. With questions about Cyprus's future in the eurozone percolating, folks bemoaned Europe's "non-stop economic decline" and that any optimistic recovery projections were "beyond the realm of likely probabilities."

Fast forward four years, and some of those same analysts are wondering when the ECB will pull its "accommodative" monetary policy. While the ECB's "help" was always overstated in our view-it was unnecessary and likely dampened growth a bit-this change in tone does suggest warming sentiment overall. Heck, the eurozone's expansion is even garnering envy from its developed world neighbors!

Because of the eurozone's earlier struggles in the global expansion and bull market, the gap between sentiment and reality is much wider relative to other places. This is one of our primary reasons for our bullishness toward Europe and why we expect eurozone stocks to do well for the rest of the year.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27 -

Market Analysis Will Lower Capital Requirements Send Banks Higher?2026-03-26

-

Politics This Week in Gridlock: Europe Edition2026-03-26

-

Expert Commentary Ken Fisher on Measuring Inflation, Currency Reset, Commodities, and more2026-03-25

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today