Personal Wealth Management / Market Analysis

Diverging to Normal

Do diverging global central bank policies really spell trouble for the bull market?

So after six-plus years of most major economies' monetary policy moving mostly in the same direction, things are changing. Europe is loosening with quantitative easing. Canada, Australia and India cut rates. Brazil hiked. The US and UK are on hold but eyeing tightening at some indeterminate, allegedly data-dependent point. Pundits have cooked up a catchall for this: "divergent monetary policy," and we are told it is very dangerous because it could make currency markets go haywire, disrupt the global expansion and rock stocks. All of which seems kinda bizarre if you consider that uncoordinated monetary policy isn't unusual or at all bad for stocks. Those who fear it today essentially fear a return to the (very benign) norm.

Before the financial crisis, the idea of globally coordinated monetary policy didn't exist outside academia. But in 2007, the Fed, ECB and BOE launched coordinated liquidity efforts to battle a banking squeeze after some Bear Stearns and BNP Paribas funds got into subprime-related trouble. More coordination followed in 2008 as Ben Bernanke, Jean-Claude Trichet and Mervyn King had graveyard-shift conference calls and turned their collective fire hose on the crisis-something many credit with preventing even worse trouble. An infatuation with coordinated central banking was born. Add to that nearly six years' worth of bull market with allegedly loose monetary policy globally, and many now believe coordination is the norm and probably necessary for stocks to rise.

History doesn't support this view. Prior to 2008, what people today call "divergent" policy was the norm-central banks did whatever they thought necessary to stoke growth or cool inflation. Most assumed this was good, because who would want a big country to make deliberate policy errors simply to move in the same direction as everyone else? Better to have each country functioning more or less fine, regardless of the direction of interest rates, and trust a bunch of growing nations will add up to global growth (and rising markets).

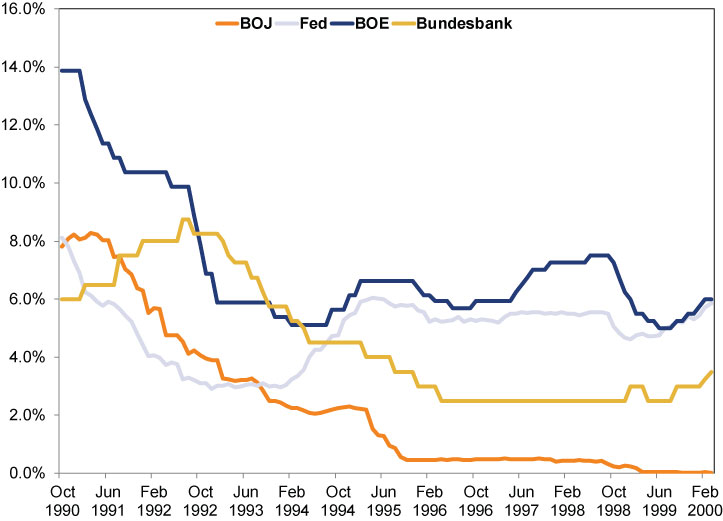

Take the mid-to-late 1990s, a rip-roaring great time for stocks. Britain started tightening in 1994 and again in 1997, while the US, Germany and Japan held steady (Exhibit 1). Yet history's longest bull market charged on: UK stocks did great, US stocks were dynamite and global markets roared higher. Capital flows didn't go haywire. Stocks cared more about the impact of monetary policy on local economies than the direction of interest rates. Economically, the US was in a Goldilocks scenario, Britain was growing but not overheating, and Europe was doing fine-that's what mattered. Yes, Asia had a currency crisis around this time, but not because the US and UK were moving in different directions. It had far more to do with some inadvisable, unsustainable currency pegs in Thailand, Russia, Korea and Indonesia. They were all pegged to the dollar, which strengthened in the mid-late 1990s despite Greenspan keeping rates on hold.

Exhibit 1: Policy Rates - 1990 Bull Market

Source: St. Louis Federal Reserve, Bank of England and Bundesbank, as of 2/10/2015. US Effective Federal Funds Rate, Japan Overnight Call Money/Interbank Rate, UK Bank Rate, German Discount Rate, October 1990 - March 2000 (monthly rates).

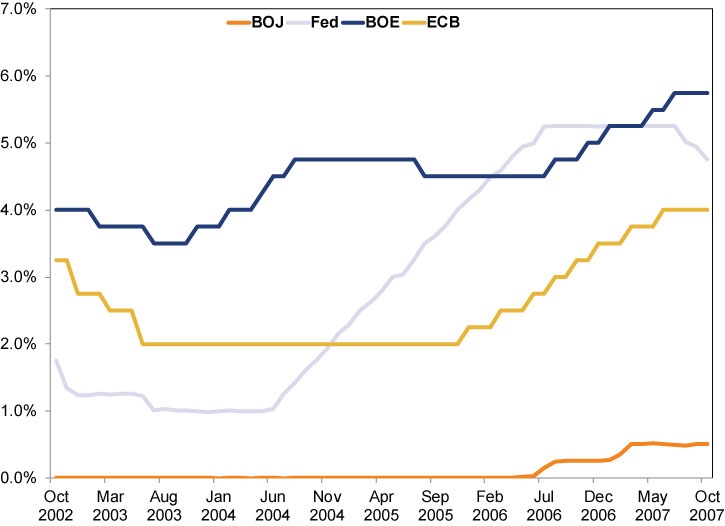

In the 2002-2007 bull market, the BOE was first to tighten. (Exhibit 2) It hiked in November 2003, when the Fed and ECB were holding at 1% and 2%, respectively. But the MSCI World still finished the year up 33.1%[i] and the world economy rose 3.8%. The Fed started tightening in July 2004, roughly a year and a half before the ECB. By the time the ECB started hiking in January 2006, the BoE had already cut rates once and was sitting on hold. None of this killed the global economy or bull market. Turned out policy decisions were just more or less appropriate for each area[ii], allowing their economies to continue growing and thriving until the financial crisis's onset in October 2007 as mark-to-market accounting wreaked havoc. (An event that had nothing to do with monetary policy.)

Exhibit 2: Policy Rates - 2002 - 2007 Bull Market

Source: St. Louis Federal Reserve, Bank of England and ECB, as of 2/10/2015. US Effective Federal Funds Rate, Japan Overnight Call Money/Interbank Rate, UK Bank Rate, ECB Main Refinancing Operation, October 2002 - October 2007 (monthly rates).

Some might say it's different this time because quantitative easing (QE) is a thing now-we're in uncharted unconventional territory. Perhaps. But QE wasn't coordinated, either. The Fed started in January 2009 and went on-and-off through November 2014. The BoE did on-and-off QE from March 2009 through November 2012. The BOJ started in October 2010 and is still going.[iii] Now, whether you take a conventional view of QE and believe it stimulated growth by boosting the monetary base and reducing long-term rates-or whether you believe, as we do, that QE was tightening because it flattened yields and depressed growth in the quantity of money-the uncoordinated starting and stopping didn't wreak havoc. Countries just responded individually to whatever pills (happy or bitter) their central banks gave them. We don't see why it would be any different now with the ECB launching its full-fledged QE program in March.

Granted, the one time short-term interest rates diverged during this bull wasn't too pretty-but 2011's volatility didn't have much (if anything) to do with the ECB's decision to hike rates to 1.25% that March while the Fed, BOE and BOJ were near their zero lower bounds. That had much more to do with dread of imminent eurozone collapse as Ireland, Portugal and Greece got bailed out. Premature tightening arguably did hurt the eurozone, which lapsed back into recession in Q4 2011, but we'd suggest not interpreting one monetary screw-up as evidence policies shouldn't diverge ever. Central banks have messed up occasionally since the dawn of central banking. Coordinated policy doesn't exempt them from this any more than divergent policy promotes it.

Heck, Europe's early 1990s currency crisis happened largely because policies were coordinated! Back then, the EU's exchange rate mechanism (ERM) forced everyone to synchronize monetary policy to keep exchange rates in harmony as euro adoption approached. Because the deutschemark had outsized influence in the ERM currency unit, countries had to tighten as Germany tightened to prevent runaway inflation after reunification. But most other European economies were weak after the 1990 - 1991 recession and would have benefited from loosening. Forced tightening as they defended currency pegs, only to discard them later, wreaked havoc.

What we have today is a world that's going back to normal. Individual central banks are doing whatever they need to based on what's going on at home (overly discussed language in the Fed's last statement not withstanding)-with one less developed-world currency peg, thanks to Switzerland. In our view, if more central bankers get these decisions right than wrong, that's a good thing for economies and stocks-regardless of whether everyone moves in unison.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] FactSet, as of 2/11/2015. MSCI World Index returns with net dividends, 12/31/2002 - 12/31/2003.

[ii] That US yield curve inversion in 2006 notwithstanding. And it remains an open question whether that would have proved a blip amid a longer-term expansion, similar to when the yield curve inverted in 1995, 1996 and 1998, if the implementation of mark-to-market accounting in November 2007 hadn't derailed the bull.

[iii] And heck, this isn't their first foray into QE. That ran from 2001 - 2006, and while that went on, other global central banks went from cutting rates in the 2001 recession to hiking in the middle of the 2002 - 2007 global expansion.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News How investors should think about oil and stocks in the Iran war – in 3 simple steps2026-03-23

-

Expert Commentary PMIs, Denmark Snap Election, Tax Season | 3 Things You Need to Know This Week2026-03-23

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 16 - March 202026-03-23

-

Market Analysis Why “War Winner” Trades Are Off Base2026-03-20

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today