Personal Wealth Management / Economics

Why Unemployment Data Shouldn't Sway Your Market Outlook

Looking at employment data to forecast the economy or markets? Look elsewhere—in our view, jobs data tell you more about the past than the future.

Good news! US unemployment rose to 4.0% in June from 3.8% in May.[i] Yep, you read that right: Rising unemployment was good news. Though it sounds bad, calculation quirks can drive unemployment higher for positive reasons. We believe June is an example—a stark change from early 2009, when the reverse was true. Back then, unemployment at 9 – 10% drove fears of joblessness (which many presumed was higher than statistics claimed) whacking consumer spending. Since consumption is 69% of US GDP, many worried this would impede recovery.[ii] Today, by contrast, folks often cite jobs data—like June’s report or initial unemployment claims' hitting their lowest in almost 50 years on Thursday—as a reason to be optimistic about stocks or the economy. However, in our view, forecasting economies and markets using unemployment data is backwards. The data are late lagging, saying more about the past than the future.

Investors’ chronic focus on unemployment is understandable but, in our view, misplaced. GDP data, consumption, industrial production, purchasing managers’ indexes and most economic data are abstract, hard to relate to. If you or your child, neighbor, friend or third cousin[iii] lose (or get) a job, that seems more real. Moreover, it seems intuitive that more employed people means more spending and, hence, economic growth and corporate profits—boosting stocks. Yet history and how businesses operate suggest it is more the reverse.

Before going further, let us discuss what the unemployment rate is—and isn’t. It isn’t the percentage of the population out of work. It is the percentage of the labor force. To be in the labor force, the government says you must either be employed or jobless and actively seeking work in the last four weeks. Hence, if an unemployed person gets discouraged and doesn’t look for a couple months, he or she isn’t counted as unemployed. However, when a growing economy gives discouraged workers hope—and they start looking—they return to the labor force, boosting unemployment even if payrolls rise. That happened in June, when 204,000 people rejoined the labor force while nonfarm payrolls rose by 213,000—the reason we called rising unemployment good news. This isn’t unique to America—most developed countries, including eurozone nations, the UK and Japan, compute rates this way.

Calculation quirks aside, jobs data lag economic growth. Consider the cycle from a business owner’s perspective. If recession hits, you might have to lay people off. Hiring is costly, so you probably want to be careful about it. The Society for Human Resources Management showed firms spent an average of $4,425 recruiting each new hire last year.[iv]

A big investment! If you can meet demand with your current staff, you probably should. This is why virtually every recovery in modern US history has initially been “jobless.” Then, as economic growth continues, sales typically improve. At some point, short staffing becomes a drag—effectively forcing you to hire to keep meeting customer demand. So you ramp up hiring. But you don’t want to overdo it and have to lay people off. So you wait until you are really confident sales will stay strong before you approve those hiring plans. Once business owners reach this stage, jobs start a-comin’. This is basically where America’s job market is now—and has been for some time. At some point, the cycle will turn and recession will hit. That pressures businesses, who must cut costs. After you paring elsewhere, they may have to resort to layoffs. In this narrative, you can see jobs following the economy rather than leading it.

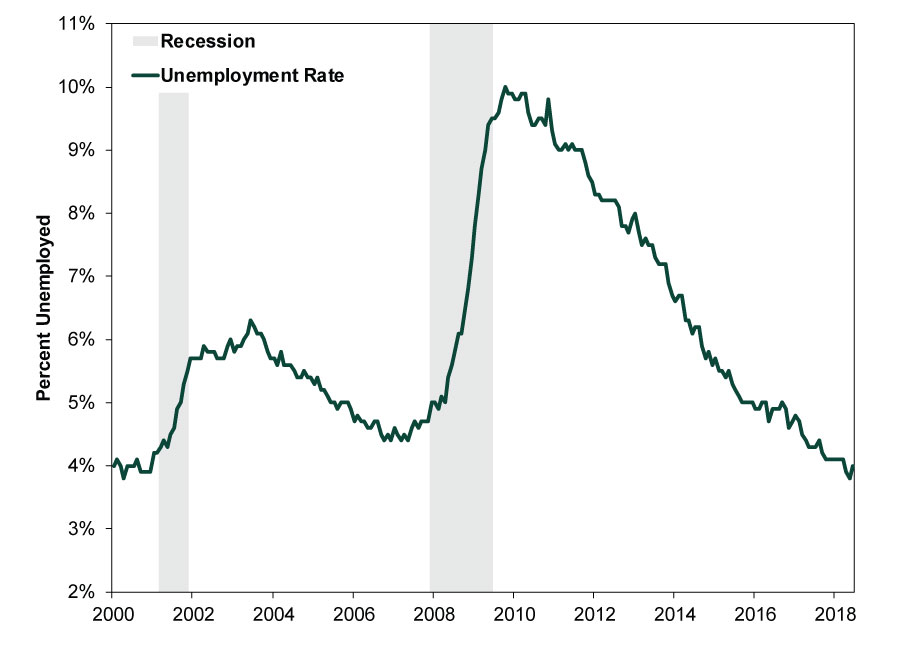

Historical data back this up. Unemployment often rises during a recession, peaking shortly after. Low unemployment typically precedes downturns—after economic growth has prompted years of hiring. Consider the two recessions since 2000. Both began amid low unemployment. Eagle-eyed readers may notice unemployment rising before the recession shading begins, but that doesn’t make rising unemployment a market timing tool—bear markets generally begin before recessions. Moreover, given how volatile unemployment can be in good times and bad, it is only clear in hindsight whether any rise is a new trend or temporary. More noteworthy, unemployment soared after recessions hit—and continued rising after they ended. Only after growth resumed did businesses start hiring, enabling unemployment to begin its jagged tumble, occasionally blipping higher even as payrolls steadily rose, due to the labor force’s comings and goings.

Exhibit 1: US Unemployment Since 2000

Source: Federal Reserve Bank of St. Louis, as of 7/18/2018. US unemployment rate, January 2000 – June 2018. Recession shading based on National Bureau of Economic Research recession dating.

The same is true in Europe—changes in unemployment lag the economy.

Exhibit 2: Eurozone Unemployment Since 2000

Source: Eurostat, as of 7/18/2018. Eurozone unemployment rate, January 2000 – May 2018. Recession shading based on Centre for Economic Policy Research recession dating.

With unemployment quite low today, you might fear it is flashing warning signs. But again, the data aren’t predictive. Unemployment can bounce around low levels for years before a recession. There are many out of the workforce in America and the eurozone who could re-enter, keeping unemployment rates stable while growth persists.

Stocks look forward, assessing how economic fundamentals may impact corporate profitability in the next 3 – 30 months. Because jobs data lag, they are little help in determining future corporate earnings. So we think investors are best off leaving jobs out of their forecasting toolkit, looking instead to forward-looking indicators like The Conference Board’s Leading Economic Indexes, yield curves, loan growth, money supply, new orders data from purchasing managers’ indexes and more.

[i] Source: US Bureau of Labor Statistics, as of 7/18/2018. May and June 2018 headline US unemployment rates.

[ii] Source: US Bureau of Economic Analysis, as of 7/20/2018.

[iii] Even your father’s brother’s nephew’s cousin’s former roommate, to quote Dark Helmet of Spaceballs.

[iv] Source: Society for Human Resource Management, as of 7/18/2018. 2017 Talent Acquisition Benchmarking Report.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics US Data Stronger Under the Hood Than Many Realize2026-03-16

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 9 - March 132026-03-16

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today