Personal Wealth Management / Market Analysis

Foreign Opportunity

The world outside the US is doing better than investors appreciate.

With the Obama administration on its way out and the Trump administration about to begin, most investors seem fixated on the US. However, America isn't the world, and much is happening outside our borders-a lot of it positive. Heading into 2017, many foreign economies are in much better shape than investors appreciate, setting up a bullish surprise.

Let's start across the Atlantic. While sentiment has warmed some, investors still struggle with old euro crisis ghosts, from a shaky Italian banking system (hello, Monte dei Paschi!) to the rise of populists in France, Germany, the Netherlands and elsewhere. These fears have created an uncertainty fog, which not only weighs on sentiment but also shrouds a little-noticed fact: The eurozone has grown for two and a half years and has been gathering steam lately.

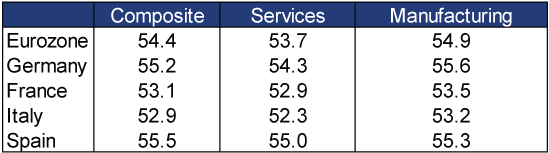

The 19-member bloc grew 0.3% q/q (1.4% annualized) in Q3, and it wasn't just economic powerhouse Germany (0.2%).[i] Continuing its solid run of late, Spanish GDP grew a robust 0.7% q/q while Ireland grew 4.0%. (Gross National Product, a gauge many consider more telling for the Emerald Isle as it limits the skew from multinationals domiciled there for tax purposes, also rose a stellar 3.2% q/q.) Italy climbed 0.3%, and even Greece(!) rose 0.8%. Of the eurozone's 19 nations, 18 grew in Q3-the exception being tiny Luxembourg, which contracted by less than 0.1% q/q. Recent purchasing managers' index (PMI) data, which measure the breadth of growth, are good too: Markit's December eurozone composite PMI reached 54.4, its highest reading since May 2011. (Reads above 50 indicate growing firms outnumber contracting firms). PMIs for the eurozone's four biggest economies-Germany, France, Spain and Italy-all bested 50.

Exhibit 1: December Eurozone PMIs

Source: FactSet, Markit, as of 1/11/2017.

Other numbers show growthy economic conditions. Broad money supply (M3) rose 4.8% y/y in November, accelerating from October's 4.4%, while lending to households and businesses (2.1% y/y and 1.8% y/y, respectively) accelerated-signs capital is available and moving. Not only does this suggest banking fears are overdone, this capital greases the wheels for future growth. December headline CPI rose 1.1% y/y, speeding up from November's 0.6%. While rising prices aren't an economic driver-they are an after-effect of money supply and economic growth-inflation's approach toward the ECB's target of 2.0% could prompt the central bank to consider tapering its quantitative easing (QE) program and/or moving away from negative interest rates. Removing these minor headwinds-and the potential boost to sentiment-bodes well for European markets. Expectations for European stocks are still pretty darn low, and considering the eurozone is in much better shape than believed, it wouldn't take much to positively surprise investors-a bullish development.

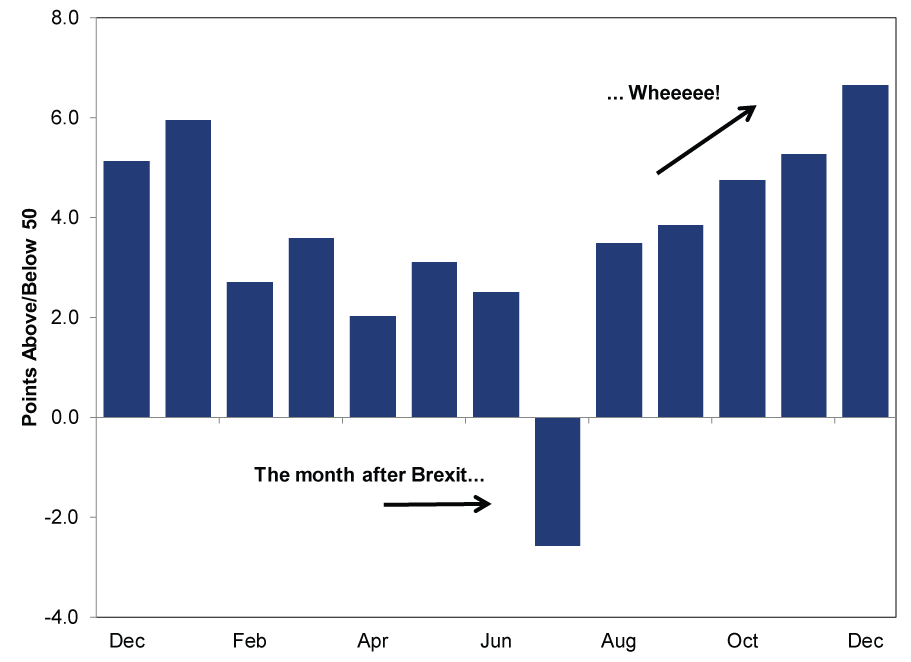

Across the Channel in the UK, fears over Brexit-related possibilities linger, as many investors overlook data showing sound growth. UK Q3 GDP rose an upwardly revised 0.6% q/q (2.3% annualized), as Services (up 1.0% q/q)-the largest sector-drove growth. Q3 reflects the first full quarter post-Brexit, so it appears the economy didn't get the memo about the vote triggering recession. Markit/CIPS' UK composite PMI provides an idea of how fleeting Brexit's impact on business was.

Exhibit 2: Markit/CIPS UK Composite PMI in 2016

Source: FactSet, as of 1/12/2017. December 2015 - December 2016.

PMI include sentiment measures, and June's referendum threw many business leaders for a loop, so July's contractionary reading isn't surprising: Firms took a wait-and-see approach in the vote's immediate aftermath. When they realized the world wasn't fundamentally different, business as usual continued. Other metrics confirm this sentiment blip hasn't impacted output. November industrial production rose 2.1% m/m-led by mining (8.2%) and manufacturing (1.3%), each contributing nearly a percentage point to headline growth-rebounding from October's -1.1%. Output's choppy pattern is in line with the trend predating Brexit by years. Recent months have shown UK consumers are healthy, and while official spending data aren't out yet for December, the British Retail Consortium's latest retail report suggests that continued as 2016 closed.

Western Europe isn't growth's sole domain, either. China is expanding at a mid-6% y/y rate. Though officials say they're comfortable with slower growth-so long as social stability isn't compromised-the world's second-largest economy shows few (if any) signs of suffering an economic "hard landing." India boasts one of the world's fastest growth rates (7.3% y/y in Q3), and notwithstanding recent demonetization rollout issues (which could impact short-term growth rates), the country is benefiting from incremental economic reform. In Japan, the data remain rather meager. November trade (exports -0.4% y/y and imports -8.8% y/y) was weak, as were personal consumption expenditures (-1.5% y/y). That said, more investors now appreciate the failure of "Abenomics" and the BoJ's "Qualitative and Quantitative Easing" program to reinvigorate domestic demand. Should this continue, sentiment towards Japanese stocks could catch up with reality. There are still weak spots to be sure (e.g., commodity-reliant economies like Brazil and Russia), but overall, growth outside the US is nothing to sneeze at.

Throughout this cycle, investors have often feared slow (or slowing) economic growth or sputtering weak spots, overlooking a core tenet of how markets operate: Absolutes matter less than how reality compares to expectations. Presently, that disconnect seems widest abroad, which could present a case for foreign as 2017 progresses.

[i] Source: Eurostat, as of 1/12/2017.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

-

Market Analysis What the Latest Global Flash PMIs Reveal2026-03-31

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today