Personal Wealth Management /

Lessons From the Golden Bear

How attractive is gold when it comes to investing over the long term?

GOOOOOOOOOOOOOOLD!!!! It doesn't seem that long ago to us that the shiny yellow metal was all the rage. Some saw gold prices reaching 5,000 ... and beyond! Folks couldn't seem to get enough. Ads touted gold as a "safe haven"—offering growth and shelter from (wrongly) perceived risks. Some even debated whether you could replace bonds with gold and get equity-like growth with little volatility![i] You can still find some of that talk today, but you may have to go looking a bit. So why has gold seemingly lost some of its shine? Ironically, for the same reason these hyperbolic calls were common back then. You see, while performance was hot back in 2011, gold has since cooled dramatically. Like it entered a big bear market. Now, we aren't here to say "we told you so!" or even forecast where gold goes from here. But rather, to point out the lessons this turn of events has to offer about gold generally.

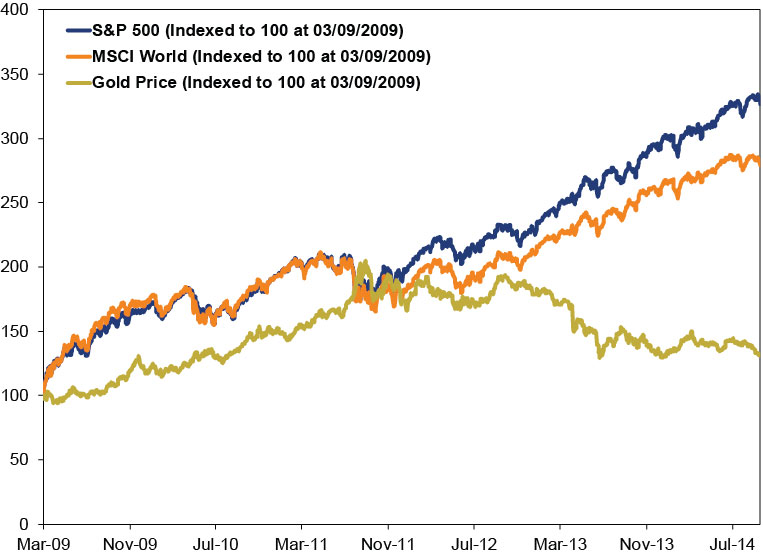

Gold's recent weakness isn't an isolated incident—it has been falling for over three years. From its record high on September 6, 2011, gold has dropped -36%, while the S&P 500 and MSCI World Index have risen 80% and 59%, respectively.[ii] Dating back to the beginning of this bull market, gold has risen only 31% compared to the S&P 500's and MSCI World's respective 226% and 179%.[iii] However, that doesn't mean when gold falls, stocks rise—the two aren't negatively correlated. After all, both stocks and gold fell after the panic initially hit in 2008. Both rose in 2009 and 2010. (Exhibit 1) Divergence didn't persistently start until late 2011. Gold isn't a consistent or reliable buffer against equity market volatility because it doesn't move contrary to stocks with consistency. In other words, even if you foresee a correction or bear market, buying gold may not be a good tactic.

Exhibit 1: Gold's Price Compared to the S&P 500 and MSCI World, 03/09/2009-09/25/2014

Source: FactSet, as of 09/26/2014. Gold prices, S&P 500 Total Return Index, MSCI World Index with Net Dividends, 03/09/2009-09/25/2014.

But gold's relatively feeble performance in this bull does reveal some irony. People believe gold serves as a meaningful hedge against all sorts of perceived risks—from geopolitical turmoil to inflation[iv]—but it clearly hasn't been one. Many thought growing fears over the tensions between Ukraine and Russia in March would goose gold. And gold did go up a wee bit! But then it turned down anew and is presently lower than before the whole Ukrainian situation started in February. As for turmoil in places like Syria and Libya, which began in early 2011, aside from a rise in early 2011, gold has sold off more or less throughout. When ISIS and Iraq first bombarded headlines, people also suggested gold as a safe alternative. It dropped. (And all throughout stocks have continued to rise-despite fears these types of regional conflicts would knock them down. Another irony!) Going back further in time-gold has either fallen or lacked luster during other regional conflicts, while stocks have climbed higher. (Exhibit 2) If you fear regional conflicts, it seems you are better off buying stocks than gold.

Exhibit 2: Regional Conflicts-Gold vs. Stocks

Source: FactSet, as of 09/29/2014. Change in S&P 500 Price Level Index and gold prices.

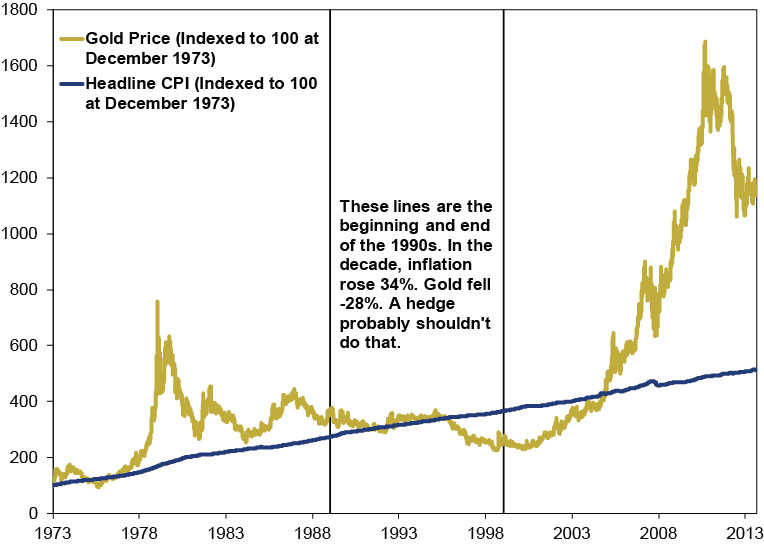

Some argue you still need gold to hedge against inflation. After all, they claim, look at what central banks have done to pump up the economy. They shout, "Money printing!"—claiming surging inflation is inevitable. But these claims have existed throughout this golden bear, and they largely get quantitative easing (QE) backwards. QE was disinflationary, not hugely inflationary. The Fed also didn't print money. It created reserve credits, and the difference is not semantic. Banks must make new loans to monetize reserve credits, and QE actually discouraged that. Now, maybe one gets it and figures the rising lending we've seen since QE's unwinding began means the inflation fear will now become reality. While we do believe there will be an uptick in inflation rates as lending becomes more plentiful, we don't believe it necessarily spikes. Besides, gold has a spotty record as an inflation hedge. From December 1973 through mid-November 2005, gold returns cumulatively trailed the change in headline CPI. They have burst back above since, but consider: That big performance burst comes during a period of benign overall CPI. It fell during the 1990s modest inflation. Gold fell -28% for the decade of the 1990s, while headline CPI cumulative rose +34%. In general, gold just doesn't track inflation all that closely-a telltale sign of an ineffective hedge. (Exhibit 3)

Exhibit 3: Gold vs. Inflation, 12/31/1973-08/29/2014

Source: Federal Reserve of St. Louis, as of 09/29/2014. Gold prices and Headline Consumer Price Index (CPI), 12/31/1973-08/29/2014.

Gold is not a safe haven or inflation hedge-and it doesn't have any other magical qualities. It is a commodity—and its long-term performance is driven by supply and demand. Supply is largely limited and predictable. It increases over the long term at an incremental pace of about 1% annually. But demand—comprised of relatively few things like jewelry, collectibles, central bank and government reserves and investment demand—fluctuates a lot, which can make gold a pretty volatile asset class. From this you should glean that gold cannot be deemed a "stable store of value" or something with "inherent value." Gold's glitter is all in the eye of the beholder. Should buyers see less gleam, gold is convertible into fewer dollars.

So whatever you think gold's future direction will be, taking account of history's lessons would seem to show you probably shouldn't base that call on inflation's direction or some "safe haven" mythology. Not to mention it is extremely difficult for investors to time when to buy and sell it. And that matters a lot with gold considering its long-term returns trail stocks, while its volatility exceeds stocks. That makes for a weak case to buy gold for the long term.

Stock Market Outlook

Like what you read? Interested in market analysis for your portfolio? Why not download our in-depth analysis of current investing conditions and our forecast for the period ahead. Our latest report looks at key stock market drivers including market, political, and economic factors. Click Here for More!

[i] You can't. This is impossible over any meaningful period.

[ii]FactSet, as of 09/26/2014. S&P 500 Total Return Index, MSCI World Index with Net Dividends, Gold Prices, 09/06/2011-09/25/2014.

[iii] FactSet, as of 09/26/2014. S&P 500 Total Return Index, MSCI World Index with Net Dividends, Gold Prices, 03/09/2009-09/25/2014.

[iv] And many more-market corrections, bear markets, recessions, etc.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

In The News What ‘IPO’ really stands for — and whether you should be buying SpaceX and the AI giants2026-06-23

-

Market Analysis Today in Brexit, Day 3,652: Brexit Turns 102026-06-23

-

Expert Commentary 3 Things You Need to Know This Week | Global PMIs, US PCE Inflation, Annuities

2026-06-22

2026-06-22 -

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—June 15 - June 192026-06-22

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today