Personal Wealth Management / Market Analysis

Oil Drum Doldrums

The oil bear resumes with longstanding oversupply issues unresolved.

Last year, Energy was the MSCI World's best-performing sector and ended 2016 on a relative upswing as investors cheered OPEC-led oil production cuts attempting to alleviate a supply glut. There was just one small thing folks didn't anticipate: surging US shale oil production, which has offset OPEC's weak efforts. By June 21, crude was down over -20% from a February high, and Energy stocks are down -10.1% year to date-the world's worst sector.[i] Last year's outperformance? Largely gone. Energy is now lagging cumulatively over the last year and a half-and is only ahead by a fraction of a percentage point since January 20, 2016-oil's low.[ii] With hindsight, it's clear 2016's Energy outperformance was a countertrend rally in a longer-term slide. Although sentiment is catching up with reality, with a fundamental supply overhang unlikely to dwindle anytime soon, we think it's still too early to load up on Energy stocks.

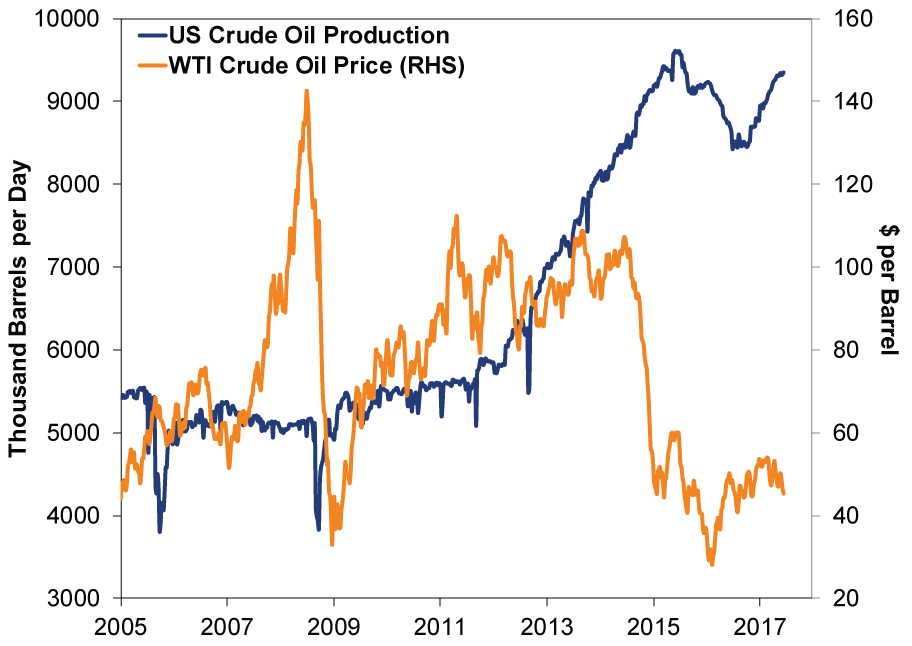

Oil's latest downturn is an extension of a much larger slide that began mid-2014. (Exhibit 1) But our story begins long before then, in the 2000s, when sky-high oil prices incentivized US producers to invest in the technology[iii] they'd need to tap America's vast shale oil reserves. Shale oil was expensive and difficult to access, but nosebleed oil prices made it worth the cost. It took a few years, but by 2012, the efforts were bearing fruit, and US oil production was soaring. For a while, oil bounced in a high range, as demand was also growing at a fast clip. But as China's infrastructure buildouts slowed and Emerging Market growth rates cooled, so did energy demand growth. Meanwhile, supply kept soaring. By 2014, supply growth far exceeded demand growth, sending prices plunging to just $26 a barrel in January 2016.

Exhibit 1: Oil's Wild Ride

Source: US Energy Information Administration and Federal Reserve Bank of St. Louis, as of 6/23/2017. Weekly US Field Production of Crude Oil and Crude Oil Prices: West Texas Intermediate (WTI) - Cushing, Oklahoma, 1/2/2009 - 6/16/2017.

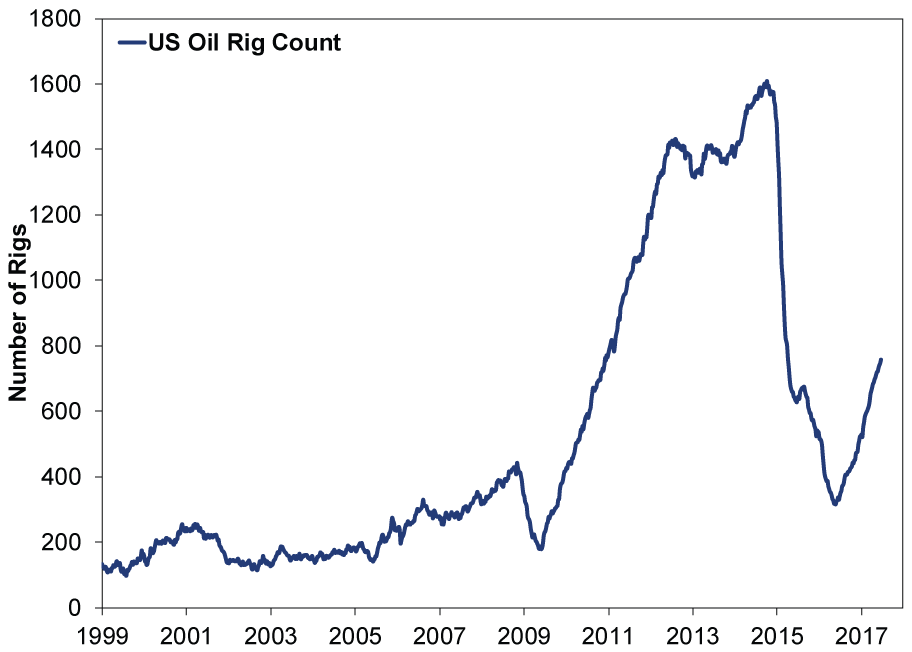

Because oil exploration and production requires high upfront costs that can take time to recoup, US firms didn't start responding to lower prices with supply cuts until mid-2015. They retrenched through mid-2016, as oil stabilized. Meanwhile, OPEC (and friends!) decided late last year to implement long-sought production cuts. Although investors cheered the deal, they overlooked telltale signs of a US rebound as firms took advantage of stable oil prices and their own improved efficiency. Oil-related investment resumed rising in Q3 2016. Rig count started rising last June. Now US oil production is approaching prior highs, entirely offsetting recent OPEC-led production cuts. The oil glut shows no signs of abating.

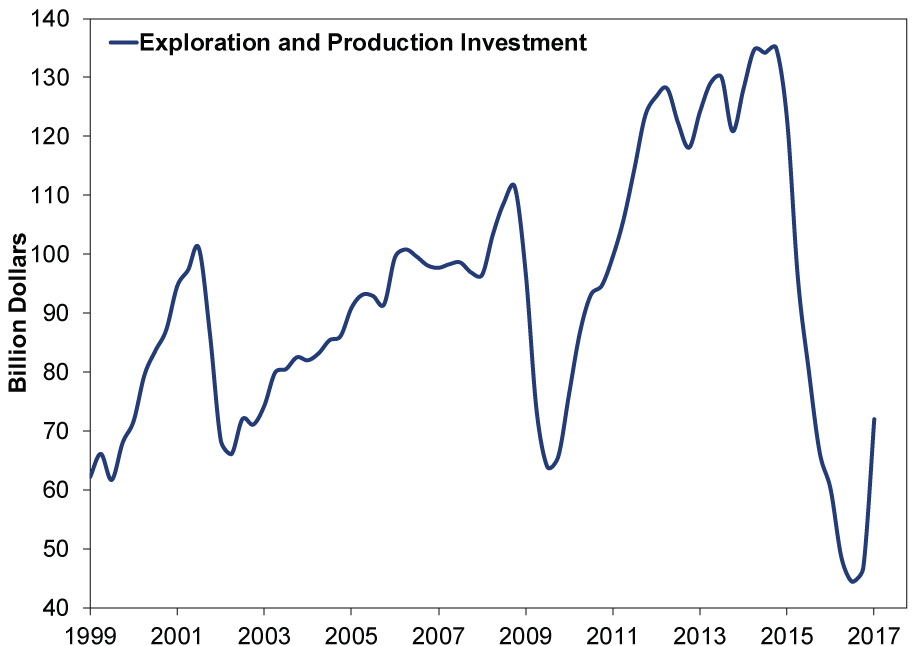

A month ago OPEC (and friends!) decided to prolong cuts, but since they had little effect before, extending them will probably be similarly ineffectual. America has largely replaced Saudi Arabia as the swing factor for global production. As US producers ramp back up, they're doing so with far fewer rigs and less capital. (Exhibits 2 & 3) As of mid-June, the US produced 9.4 million barrels per day (mbpd), just under its 9.6 mbpd peak two years ago and 1970's record-high 10.0 mbpd. Yet firms are using less than half the rigs used in 2015 (and 1970). In 2015, it took 1600 rigs to produce 9.6 mbpd. Now it takes less than 800 for 9.4 mbpd. In 1970 it took over 1000. Costs are down, too. In 2015, producers sank around $130 billion into exploration and production investment. That now stands at $72 billion. With rigs and investment trending upwards, America is unlikely to relinquish its hard-fought swing producer status any time soon.

Exhibit 2: Near-Record Production Despite Halved Rig Count

Source: Baker Hughes' North America Rig Count, as of 6/26/2017. Weekly US Oil Rig Count, 1/8/1999 - 6/23/2017.

Exhibit 3: Near-Record Production Despite Near-Decade-Low Investment

Source: Federal Reserve Bank of St. Louis, as of 6/26/2017. Real private fixed investment: Nonresidential: Structures: Mining exploration, shafts, and wells, Billions of Chained 2009 Dollars, Quarterly, Seasonally Adjusted Annual Rate, Q1 1999 - Q1 2017.

What's behind American shale drillers' surging efficiency and productivity gains? Technology! Big data and automation aren't just reserved for Silicon Valley, but the Permian Basin and everywhere else folks drill for oil. Remote sensors on equipment (measuring everything from well pressure and heat to boring bits' RPM), using data gathered to continually improve techniques, constant monitoring to avoid outages, and computer-directed drilling have made finding and pumping oil far more precise. Companies employing such methods have slashed time to market, labor and the expense needed to get new wells into production. Breakeven production costs vary, but in some US locales are now as low as $15 a barrel and are averaging in the $30s. With crude oil still north of $40 there is incentive aplenty to ramp production, keeping a lid on prices.

Sector sentiment is souring with pricing, but a prolonged Energy upturn probably won't occur without full capitulation and better supply/demand balance. Although US demand is rising (May deliveries were the highest in a decade) and could ramp higher as petrochemical plants sprout, demand growth is waning in China, India and Japan-20% of global oil consumption. Unless global demand picks up a lot or global supply falls much more than OPEC has announced, oil prices-and Energy stocks with them-are likely to remain in the doldrums. Or take Brazil, where recession is sapping demand (6% of global consumption) and contributing to the supply glut as local energy firms offset weak domestic consumption with foreign sales. Record exports are expected to make it the second largest non-OPEC supplier[iv]-after the US.

Even as sentiment is starting to sour, Energy P/E ratios are still far above the rest of the market. Now, a lot of that is due to Energy's 2015 - 2016 earnings implosion, but it could signal that despite Energy's most recent underperformance, investors have yet to capitulate. Last year's countertrend is testament to that. And since a bottom-fishing mentality remains prevalent-"the market's just dying for a reason to buy this thing"-sentiment still appears too high. Lastly, with US drillers working to pay off creditors and oil exporting countries in need of revenue for government coffers, shareholder returns seemingly aren't a top priority.[v]

While falling oil prices are bad for Energy stocks-especially with sentiment yet to fully surrender-markets overall remain unrattled amid hearty global economic and earnings expansion. Energy's time will come, but for now we believe better opportunities lie in other sectors.

[i] Source: FactSet, as of 6/28/2017. MSCI World Energy Sector Index returns with net dividends, 12/30/2016 - 6/27/2016.

[ii] Ibid. MSCI World and MSCI World Energy Sector Index returns with net dividends, 12/31/2015 - 6/27/2016 and 1/20/2016 - 6/27/2016.

[iii]Horizontal drilling and hydraulic fracturing, aka "fracking," pioneered by one George Mitchell.

[iv] By the way, the same dynamic is at work for OPEC members as well. Hello Iraq.

[v] US shale operators' falling breakeven costs and earnings improvement keep them in business of course.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today