Personal Wealth Management / Market Analysis

People Are Saving Their Savings

Those big cash buffers have yet to go anywhere.

At the start of the year, many pundits predicted robust US economic growth. One of the most commonly cited reasons: Businesses and consumers would unleash their pent-up cash. With the year well underway, we can check how that claim holds up. Our research indicates savings remain robust while consumption hasn’t leveled up to a much higher plateau, and we doubt that changes—an important reality check for investors, in our view.

US spending measures did jump earlier in the year. In March, retail sales surged 11.3% m/m while broader personal consumption expenditures (PCE) rose 4.7%.[i] To many pundits, these readings seemed like the start of something bigger. However, although the latest numbers still show high spending, the pop seems to be waning on the retail side as spending shifts to services. Friday’s May consumer spending report will add more color, and analysts currently expect 0.4% m/m growth—a tad slower than April’s 0.5%.[ii] Nothing here is surprising to us—we long anticipated a brief, reopening-related bump, and that appears to be playing out.

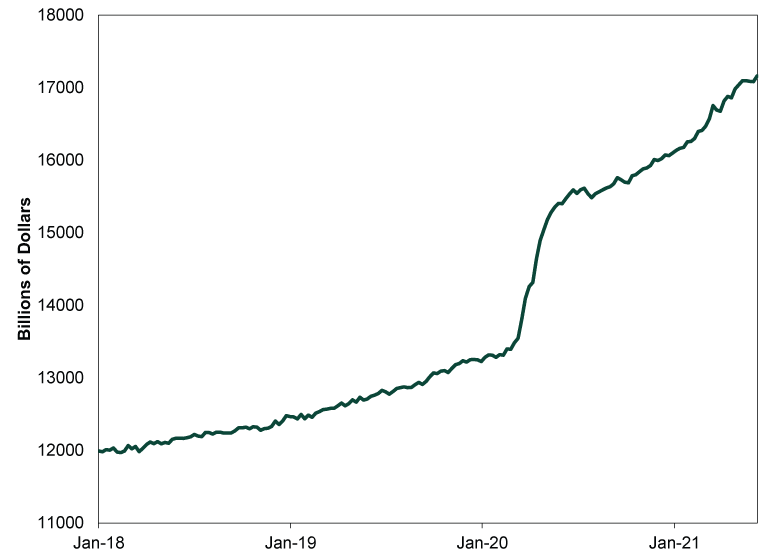

But we also see signs businesses and consumers aren’t drawing down the cash piles they built up over the pandemic, suggesting this is a temporary boom before a return to normal. One piece of evidence: bank deposits. These surged between March and July 2020 as companies and households stashed cash away during the severe economic contraction. Since then, the latest data through June 9 show bank deposits continue to climb at a more modest rate. (Exhibit 1)

Exhibit 1: Bank Deposits Are Still Rising

Source: St. Louis Federal Reserve, as of 6/23/2021. Deposits at all US commercial banks, weekly, 1/3/2018 – 6/9/2021.

Many companies’ chief financial officers and treasurers may prefer to maintain cash buffers right now, especially since pandemic-related uncertainties remain.[iii] In our view, this isn’t a negative. It seems prudent for companies to hold cash in the event of an unexpected rainy day—e.g., government-mandated business restrictions or closures at a moment’s notice. Moreover, businesses’ desire to preserve cash may also cool any itch to spend on a rash of potentially unproductive investments, delaying the excess that usually marks an expansion’s end.

Households, too, seem to want to hold on to savings in the wake of the pandemic’s economic fallout. The New York Federal Reserve has argued American households’ allegedly “excess savings” aren’t actually excessive—many may be saving due to uncertainty surrounding their employment situation and the economy.[iv] Anecdotal evidence bears this out, too: COVID-19 may have motivated many families to contribute to their rainy day funds in a way they never had before.[v]

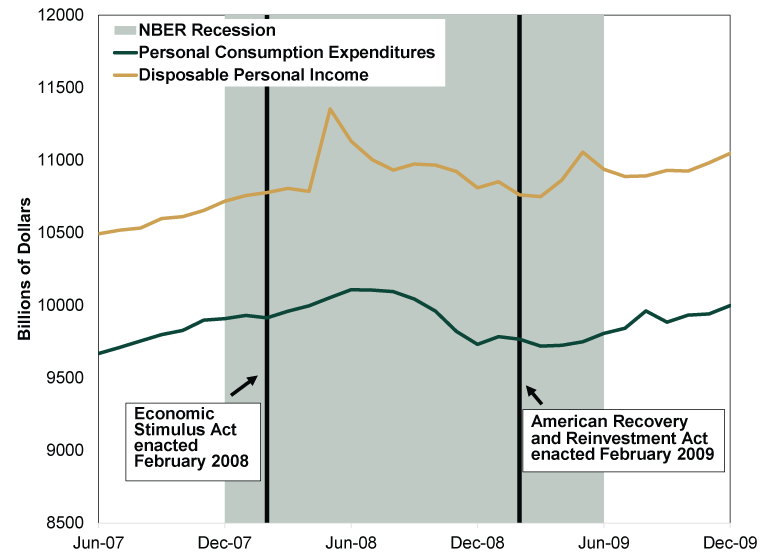

The desire to save may also be influencing what households are doing with their COVID relief checks. Many experts expected consumers to spend those payments. Some are, to an extent, but folks appear to be saving some of that cash, too. The Fed’s quarterly household wealth report showed balances in cash, checking accounts and savings deposits rose by a combined $850 billion in Q1 2021 to a record $14.5 trillion, bolstered in part by COVID relief.[vi] (A separate Fed study, from the New York Branch, showed US credit card balances fell by -13.8% at the same time, suggesting debt repayment was another priority for Americans.[vii]) This isn’t a huge surprise, in our view. As Stanford Economics Professor John Taylor has shown—and as we have highlighted in a chart shared here before—past one-time direct payments from the federal government didn’t meaningfully boost consumer spending. (Exhibit 2)

Exhibit 2: Cash Payments Don’t Necessarily Boost Spending

Source: St. Louis Federal Reserve, as of 3/30/2021. Personal consumption expenditures and disposable personal income, billions of dollars, monthly, June 2007 – December 2009. NBER recession dating used.

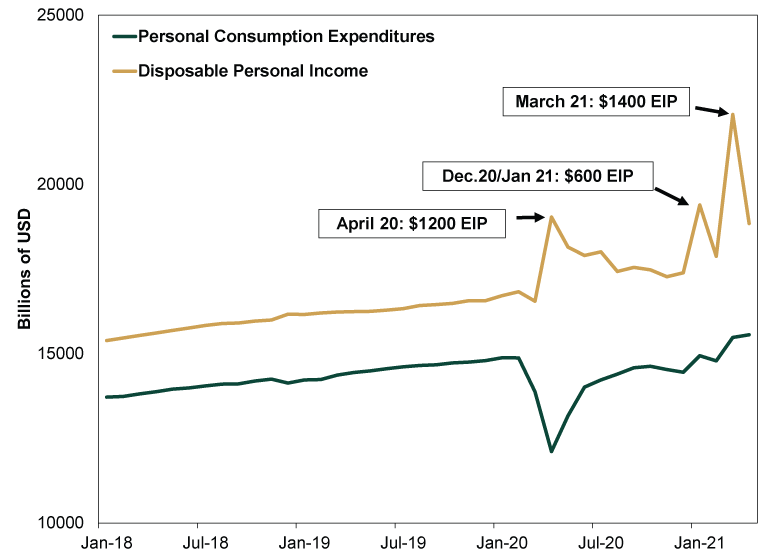

So far, the experience with COVID relief checks seems to be echoing what happened over a decade ago. Recent household spending hasn’t popped the way disposable personal income has after each economic impact payment—a sign, in our view, that folks aren’t solely spending those checks.

Exhibit 3: Economic Impact Payments Still Haven’t Boosted Spending

Source: St. Louis Federal Reserve and USA.gov, as of 6/21/2021. Personal consumption expenditures and disposable personal income, billions of dollars, monthly, January 2018 – April 2021. “EIP” refers to Economic Impact Payment.

History also suggests newly acquired savings can remain around for a long time. Matthew Klein of Barron’s recently showed household saving jumped during World War II—due partly to government encouragement and partly due to rationing because of the war effort.[viii] However, the savings rate didn’t revert to prewar levels after the Allies’ victory. Many Americans chose not to spend down the healthier balance sheets they just acquired. As Klein noted, “In fact, the U.S. household saving rate remained well above the pre–WWII average every single year until the late 1990s. Rather than spend down their hoarded cash, Americans worked hard to preserve the financial gains they had achieved.”[ix] While there are obvious differences in the overall backdrop between then and now, we think consumers’ past actions should temper expectations of an inevitable savings-driven spending boom.

In our view, these data and history toss cold water on the notion higher savings must turn into something else. Now, we don’t think this is a negative that robs the economy of fuel. People and businesses are still spending today and will likely do so for the foreseeable future, albeit eventually at a slower rate, in our view. However, those anticipating households and businesses to unleash their buffers may be waiting for a long, long time.

[i] Source: FactSet, as of 6/21/2021.

[ii] Source: FactSet, as of 6/23/2021.

[iii] “Banks to Companies: No More Deposits, Please,” Nina Trentmann and David Benoit, The Wall Street Journal, June 9, 2021.

[iv] “‘Excess Savings’ Aren’t Excessive,” Florin Bilbiie, Gauti Eggertsson, Giorgio Primiceri, and Andrea Tambalotti, Liberty Street Economics, April 5, 2021.

[v] “Here’s How Parents Are Spending Stimulus Checks Sent to Their Kids,” Carmen Reinicke, CNBC, June 9, 2021.

[vi] “Household Wealth Jumps to Record $136.9 Trillion, Fed Says,” Ann Saphir, Reuters, June 10, 2021.

[vii] Source: Federal Reserve Bank of New York, as of 6/23/2021. Quarterly Report on Household Debt and Credit, Q1 2021.

[viii] “On the Crisis and Inflation, Barron’s Shows How the Past Can Be Prologue,” Matthew Klein, Barron’s, June 10, 2021.

[ix] Ibid.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Expert Commentary This Week in Review | Q1 Recap, Earnings Guidance, Elections

2026-04-03

2026-04-03 -

Market Analysis A Forward-Looking Lesson One Year After Liberation Day2026-04-02

-

Market Volatility Some Timeless Counsel After March’s Volatility2026-04-01

-

Market Analysis Countertrends and Corrections: Banks in 2026’s Early Selloff2026-04-01

Learn More

Learn why 200,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 3/31/2026

New to Fisher? Call Us.

Contact Us Today