Personal Wealth Management / Market Analysis

A Look at Sentiment—Then and Now

A look back at a bull market’s peak just over 19 years ago can put today’s sentiment in important perspective.

Nineteen years ago March 24, the Tech-led bull market reached its zenith, preceding a nasty, two-plus-year long bear market that wiped about 50% off the S&P 500.[i] Today, an even longer bull market is running—with many fearing it will soon meet a similar fate. But comparing sentiment in March 2000 to today highlights how different the two periods are. Investors aren’t currently close to euphoria—one sign this bull market likely has further to run.

So where are we in the lifecycle of a bull? We think bull markets end in two ways: atop the wall of worry or sideswiped by a wallop. Legendary investor Sir John Templeton’s famous maxim encapsulates the wall of worry: “Bull markets are born on pessimism, grow on skepticism, mature on optimism and die on euphoria.” At bull beginnings—typically deep into a recession—almost no one wants to own stocks. As markets and the economy improve, worries gradually fade, enticing more previously timid investors into the market. These lingering fears are the proverbial wall of worry. While they exist, they help keep expectations low, creating room for reality to positively surprise. When worries run out and reality can’t possibly match expectations, the stage may be set for negative surprise and a bear market.

Wallops—huge, unforeseen shocks ending global growth—also kill bulls. Examples of this are the approach of World War II and 2008, when the one-two punch of a (still) little-noticed accounting rule exaggerated banks’ loan losses to a ridiculous extent, inciting a schizophrenic government response. Wallops are always possible, and we are on the lookout, but we don’t see anything looming presently.

Absent a wallop, keeping tabs on sentiment—and comparing it to the likely economic reality—is a good way to assess how mature the bull market is. Measuring sentiment is more art than science. Sentiment surveys aren’t a complete picture. More qualitative indicators matter, too—headlines are a good example, as they reflect and influence how investors feel. But there are other ways to quantify sentiment.

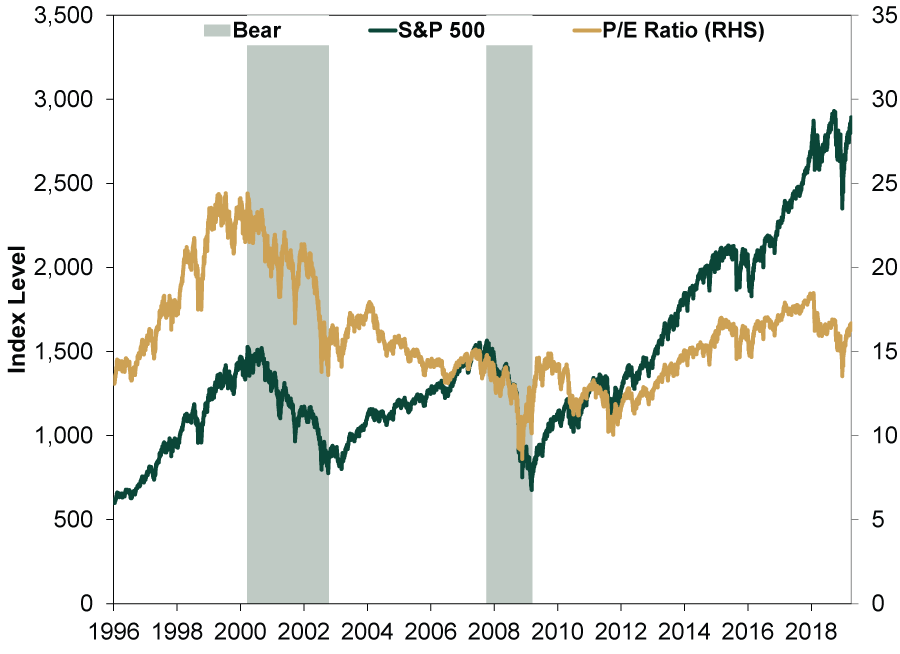

On the data front, valuations can help. We don’t think valuations like price-to-earnings (P/E) ratios—how much investors are willing to pay for corporations’ earnings—are useful forecasting tools. Cheap stocks can always get cheaper, and pricey stocks can always get pricier. But at extremes, we think P/Es and other valuation measures provide a decent sentiment snapshot. As Exhibit 1 shows, compared to 2000, sentiment is nowhere near euphoric. In the run up to 2000’s bull market peak, the S&P 500 (green line) nearly tripled from 1996. Over that time, the S&P 500’s forward 12-month P/E (yellow line) climbed from 13.5 to 24.4 at the bear’s onset—a big, fast jump, signifying outlandish expectations for future profitability by the end. A 24.4 P/E wasn’t inherently bearish on its own, but paired with an inverted yield curve, other faltering leading indicators like credit growth, credit spreads spiking higher and falling corporate profitability, it seemed unrealistically optimistic. Valuations today are nowhere near as stretched, and they are moving more slowly—and not inexorably upward.

Exhibit 1: Stock Valuations Show Investors Aren’t Euphoric

Source: FactSet, as of 4/5/2019. S&P 500 Price Index and next 12 month price-to-earnings (P/E) ratio, 1/1/1996 – 4/5/2019.

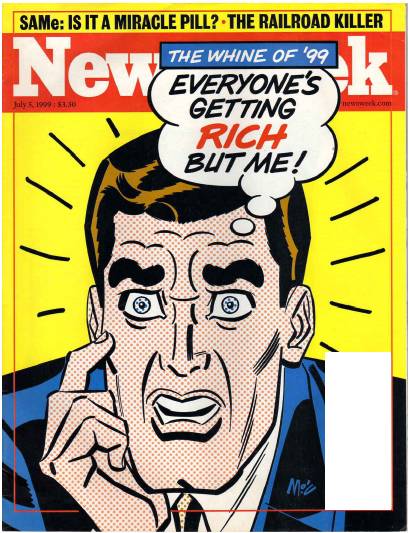

Squishier measures of sentiment show an even starker contrast. Headlines were outlandish leading to 2000’s peak. To get a better sense of what market mania looks and feels like, take a glimpse back at some cover stories from the time:

-

Newsweek’s July 1999 cover story, “Everyone’s Getting Rich But Me!,” documented the travails of those with a severe case of FOMO.[ii]

-

On December 20, 1999, The New York Times ran a 2000 outlook titled, “It’s a Bird! It’s a Plane! Yes, and It’s Also the Latest IPO!” It argued recent IPO activity “provide[d] indisputable evidence that the stock market has entered a thrilling new era where the old rules do not apply.”

-

BusinessWeek had a twofer in early 2000, with January’s “The New Economy” and February’s “The Boom.”

Everyone was all in on the craze. Naysayers were pilloried as fuddy-duddies. As the Wall Street Journal wrote in March 2000 about a fund manager who “hit the brakes” in September 1999:

Too many investors had fallen too deeply in love with too many technology stocks, he decided. It was time, he said, “to put the seat belt on.” The veteran stock picker quickly trimmed positions, raised the portfolio’s cash level -- and watched the stocks he’d just pared soar in the biggest tech run-up of all.

While his $15 billion-in-assets mutual fund still finished up a super-charged 101% in 1999, it trailed the 134.8% gain of the average science-and-technology fund tracked by data firm Lipper Inc., not to mention the several dozen funds that delivered more than 200%. [Boldface ours.]

“We got smoked,” Mr. Morris now says.

FOMO in action! It was a “new paradigm” after all. And don’t forget the IPOs! The frenzy of getting in on them. Issuing them. Flipping them. For flower companies.[iii] For free music and internet-access companies selling advertising.[iv] For pet supply companies.[v] Of course, there were some (eventual) winners. But the IPO machine crumpled under the weight of expectations. The paper gains from blockbuster mergers undertaken assuming heady new economy logic evaporated. When the sentiment tide turned, the aftermath wasn’t pretty.

Many new-era claims now look silly in retrospect, but in punch-drunk times “irrational exuberance” seems sane. Most dismiss or ridicule objections otherwise, despite concrete warning signs of trouble ahead. They included an unnoticed, persistent yield curve inversion and a negative Leading Economic Index trend, extremely high valuations, credit spread spikes and falling earnings. That is a recipe for euphoric poison to kill a bull.

Nowadays, nearly the reverse is true. While the bull has matured on optimism over a 10-year climb, sitting presently just 1.3% from all-time highs,[vi] skepticism—bolstered by last year’s late volatility—remains. Glancing at headlines the past few days:

-

“Beware the Market Where Everything Goes Up”[vii]

-

“Will Today’s Global Trade Wars Lead to World War III?”[viii]

-

“All the Reasons to Fret About the Global Economy, in Charts”[ix]

-

“Global Growth Faces Fresh Threat as Industrial Downturn Spreads”[x]

-

“One of the Most Important Recession Indicators Is Beginning to Flash. Is It Time to Worry Yet?”[xi]

Recession and bear market fears lurk around every corner. Yet earnings are rising and forward-looking economic indicators project they will continue doing so. Recent IPOs are well-established corporations with large and growing client bases—if perhaps not yet profitable—and skepticism towards them is running quite high. Meanwhile, the global yield curve is positive, supporting worldwide credit and money supply growth.

Bull markets don’t die of old age. Most often, unrealistic expectations kill them—euphoria, as Templeton counseled. With euphoria absent and a wallop unlikely, we think this bull has plenty of room to run.

[i] Source: FactSet, as of 3/29/2019. S&P 500 Price Index, 3/24/2000 – 10/9/2002.

[ii] FOMO: Fear of Missing Out.

[iii] “1-800-Flowers.com’s IPO Lesson: It’s Never Easy Coping With Wilt,” Erin White, The Wall Street Journal, 8/19/1999. Selling tulips.

[iv] “MP3.com Sees Stock Price Double Following IPO,” Jim Carlton, The Wall Street Journal, 7/22/1999 and “Free-Access Firm NetZero Surges 82% After Offering,” Staff, The Wall Street Journal, 9/25/1999.

[v] “Pets.com Will Shut Down, Citing Insufficient Funding,” Pui-Wing Tam and Mylene Mangalindan, The Wall Street Journal, 11/8/2000.

[vi] Source: FactSet, as of 4/5/2019. S&P 500 Price Index, 9/20/2018 – 4/5/2019.

[vii] Mike Bird, The Wall Street Journal, 4/2/2019.

[viii] Daniel W. Drezner, Reason, May 2019.

[ix] Michelle Jamrisko, Bloomberg, 4/2/2019.

[x] Paul Hannon, The Wall Street Journal, 4/1/2019.

[xi] Jordan Weissmann, Slate, 3/26/2019.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis The New Tariffs in Town Are Still Old News2026-07-24

-

Expert Commentary This Week in Review | Market Volatility, Tariffs, SpaceX

2026-07-24

2026-07-24 -

Expert Commentary Why Ken Fisher Is Optimistic About European Stocks

2026-07-23

2026-07-23 -

Economics A Summertime Check-in on US Consumers2026-07-23

{kind=link}

{kind=link}

Learn More

Learn why 210,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 6/30/2026

New to Fisher? Call Us.

Contact Us Today