Personal Wealth Management / Economics

Hiring Lays an Egg: How Investors Should Approach US Unemployment

Friday's disappointing US unemployment report should have little to no weight in your analysis of stocks' direction.

Many people think there wasn't enough of this in May. Photo by Bloomberg/Getty Images.

"'The jobs report was bad, bad, bad: There is no positive spin to it. Not only was May a particularly weak month - the worst in almost six years - but revisions dragged previous months lower.'"

That is a brief summation of the punditry's general reaction to May's US Employment Situation Report, which showed employers added "only" 38,000 workers, a sharp slowdown from April's (downwardly revised) 123,000 and well below the last 12 months' average of 200,000. But here is the thing: While it's true this was as lackluster a report as jobs reports go, we'd humbly suggest the investment implications of this-as they usually are with jobs reports-are nil. Jobs data are not an indication of where the economy is heading. They aren't even an indication of where the economy is now. They are a late-lagging indicator, a data point alluding to where the economy was.

This is a point we've brought up on probably about 50 occasions since this bull market began. Virtually any time hiring disappointed, pundits would seize on it and an ocean of negative "economic" news would flood the internet. When good jobs news arrived, we'd point out that the rosy sentiment it triggered was equally as misplaced as a bearish take: It is a trap to forecast based on lagging data points.

Now, the data are downwardly skewed by the Verizon strike, which reportedly knocked 35,000-ish jobs from the figure. However, even if we add those back in and make no other adjustments, 73,000 jobs added would still have missed expectations and likely disappointed many. Furthermore, while the unemployment rate fell 0.3 percentage point to 4.7%, it did so almost exclusively because some folks stopped looking for work-a calculation quirk many note has more negative overtones than positive.

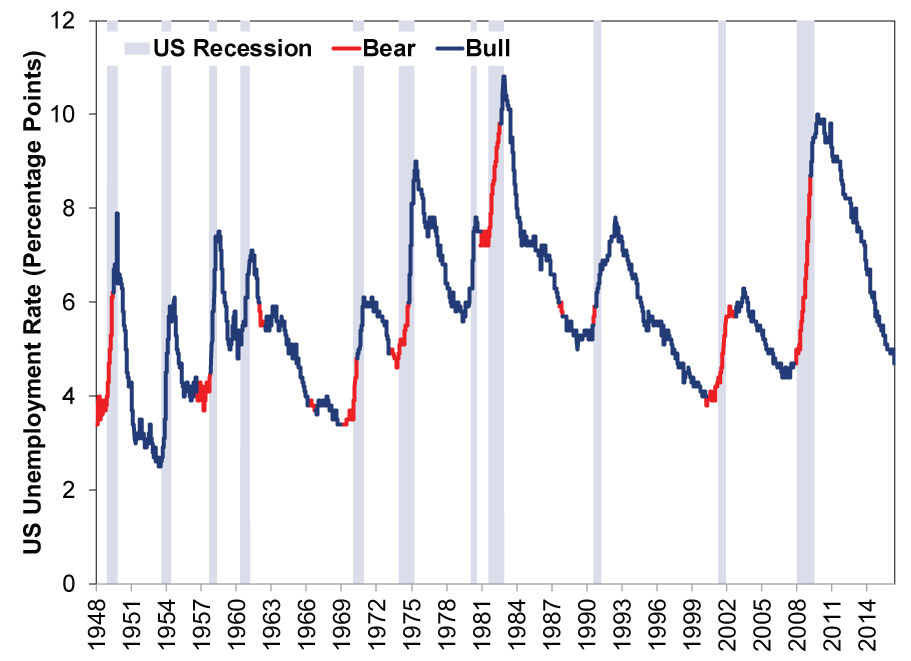

But all in all, whatever your take on these data, don't adjust your forward-looking view of stocks based on it. As Exhibits 1 and 2 show, that is an error. Exhibit 1 plots the post-war US unemployment rate and US recessions. The red segments are S&P 500 bear markets. As you can see, bears typically start before recessions. And unemployment lags both, often materially rising only well after a recession is underway and peaking after it ends.

Exhibit 1: Stocks Lead, Jobs Lag

Source: Federal Reserve Bank of St. Louis, as of 6/3/2016. January 1948 - May 2016. Recession dating is determined by the National Bureau of Economic Research, the official US business-cycle dating arbiters. S&P 500 bear markets.

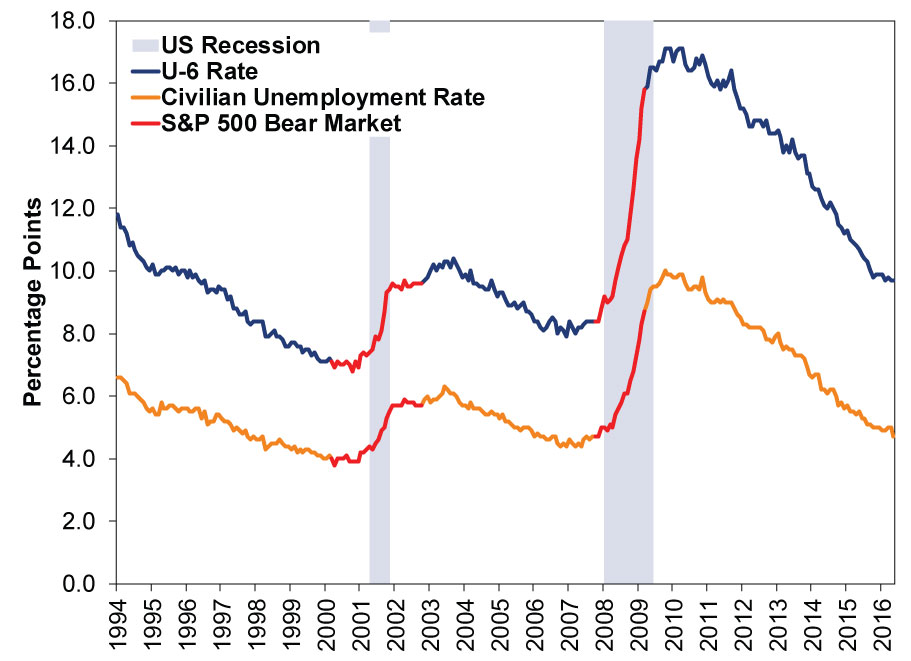

Exhibit 2 shows you the same, but includes the U-6 unemployment rate, which includes discouraged workers and the "underemployed"-those working part-time for economic reasons.[i] This shows you jobs' tendency to lag is not a function of the headline unemployment rate's calculation quirks. It is a function of the fact employers react to changes in demand-they don't hire based on forecasts.

Exhibit 2: Stocks Lead, Jobs Lag Part Deux

Source: Federal Reserve Bank of St. Louis, as of 6/3/2016. January 1994 - May 2016. Recession dating is determined by the National Bureau of Economic Research, the official US business-cycle dating arbiters. S&P 500 bear markets.

One major interpretation we see dotted across the entire internet is that this means the Fed's "planned" June (in some cases, July) hike is off the table. Both 10-year and 2-year Treasury yields, which had drifted higher in recent weeks, possibly influenced by increasing rate-hike chatter, fell a sharp 11 basis points apiece, as folks figured the self-proclaimed "data-dependent" Fed would depend on these data and keep rates on hold. Which, maybe they do, but that is unknowable today and rather needless speculation. A 25 basis point rate hike would not invert the yield curve, and slightly higher short-term interest rates aren't likely to prove problematic.

Two, the Fed has gone to great pains to tell anyone who would dare listen that policy isn't on a pre-set course, a fancy way of saying no rate hike is planned, ever. They (claim to) assess the "data" at each meeting and make a determination based on that assessment. Which brings us to a final Fed point: No one outside the Fed's meeting rooms knows what data they are exactly looking at. We know its 2% inflation target is based on the headline Personal Consumption Expenditures price index, which rose to 1.1% y/y in April-its third reading above 1% in 2016's four reports to date. But they haven't specified employment related matters. They all say it isn't one data point, so does the recent average matter? The slowdown trend? Will they wait for revisions, which are potentially quite large?

Many claim it isn't the headline unemployment rate at all. Or the U-6. In 2014, Fed head Janet Yellen expressed her fondness for the Kansas City Fed's Labor Market Conditions Index, a sort-of meta-backward-looking indicator that mashes together 24 different labor market variables. That is not out yet for May, but through April wasn't showing material weakness. Then again, do Fed officials weigh the level, trend, momentum, an average over some time period? You can't know! Do they weight some of the 24 variables more heavily than others? Do they apply subjective judgments to the data? Do they commit behavioral errors, like using recency bias to extrapolate trends forward? You can't know any of that either!

For all the headline negativity Friday's jobs slowdown triggered, for investors, this is noise. One of the very hardest parts of investing is knowing where to spend your precious time and energy. Sometimes, that's obvious. Other times, it is less apparent, and the media isn't likely to help you divine which is which. (They want you to pay attention to everything!) We'd suggest the evidence shows the jobs report is one investors can spend little time analyzing, letting them focus their energies on more productive, forward-looking matters.

[i] The U6 gauge only goes back to the early 1990s, hence why the two timeframes are different.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Around the World in Central Banking, Iran War Edition2026-03-19

-

Politics Beyond the War: A Political Roundup Covering America, Canada and Denmark2026-03-17

-

Economics Doubts Aplenty After UK January GDP Flatlined2026-03-17

-

Expert Commentary 3 Things You Need to Know This Week | Fed Meeting, Central Banks, Defense Spending

2026-03-16

2026-03-16

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today