Personal Wealth Management / Market Analysis

Lagging Wages Won’t Slow the Expansion

What to make of July’s negative real wage growth in the US.

By one measure, July US inflation outpaced July wage growth. Uh-oh! This leads some financial pundits to theorize that, despite faster GDP growth, consumers are also facing higher prices—and their paychecks aren’t keeping up. Their conclusion: Something bad is brewing. In our view, this worry is off, and not just because most wage discussion is sociology and the data themselves are backward-looking. There are also some quirks that render them an inaccurate snapshot of most households’ actual purchasing power.

Earlier this month, the Bureau of Labor Statistics (BLS) announced its Consumer Price Index (CPI) rose 2.9% y/y (0.2% m/m), ticking up from June’s 2.8%. The BLS also shared average hourly earnings rose 2.7% y/y. That means real average hourly earnings—i.e., earnings adjusted for inflation—fell -0.2% y/y. In dollar terms, the average real wage fell from July’s $10.78 an hour to $10.76 an hour. Cue the financial media’s sirens! The Wall Street Journal fretted consumer prices “eroding wage gains.”[i] A Washington Post headline painted an even bleaker picture, declaring “wage growth is being wiped out entirely by inflation.”[ii] All sounds pretty worrisome!

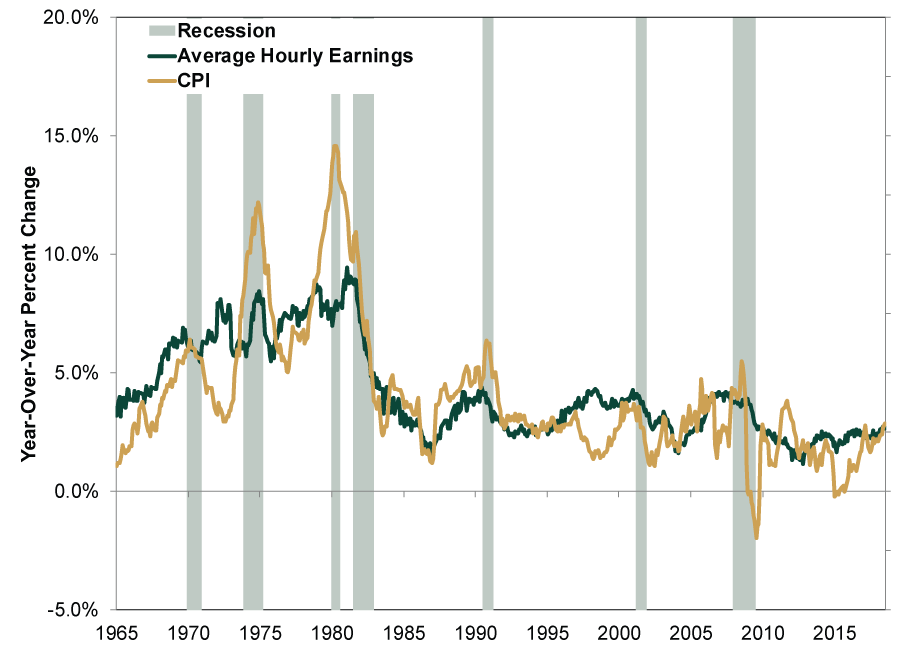

But wage growth’s trailing inflation—known as “negative real wage growth”—doesn’t mean broader trouble looms. First, consider history. (Exhibit 1)

Exhibit 1: Negative Real Wage Growth Doesn’t Spell Trouble

Source: St. Louis Federal Reserve, as of 8/16/2018. Average hourly earnings of production and nonsupervisory employees (total private) and Consumer Price Index for All Urban Consumers: All Items, monthly, January 1964 – July 2018.

The US experienced negative real wage growth numerous times over the past 50 years—see the 1980s, the first half of the 1990s and even different points during the current expansion. Yet the economy didn’t crash, and many of these periods were a terrific time to own stocks.

Moreover, this isn’t just a US phenomenon. Across the pond, our friends in the UK have similarly fretted higher inflation and slower wage growth would crimp consumption. Yet as we wrote back on March 28 in our commentary, What Rising Real Wages Say About the UK Economy:

Even as real wages fell for a long spell during this economic expansion’s first five years, consumer spending grew. While it bounced around a good deal the first couple years, consumer spending growth turned consistently positive in late 2011—over two years before real wages started their recovery.

As in the US, the UK expansion chugged along despite falling real wages.

No single metric or dataset is all-telling. All data have their limits, and the BLS’s wage and inflation measures are no exception. For example, aggregate hourly pay can get skewed by shifts in the workforce. As highly paid, long-tenured workers retire and lower-paid, inexperienced folks enter the workforce, the average might not move much—and may even fall—but workers aren’t necessarily worse off. At the risk of stating the obvious, younger, less experienced workers typically get paid less.[iii] Gauges like the Atlanta Fed’s Wage Growth Tracker (which examines the wage changes of the same workers over time) suggest workers may be doing better than the BLS’s numbers indicate. We aren’t saying one wage metric is superior to the other. Rather, be aware of the nuance and what exactly each measures.

The same goes for inflation gauges. Financial media commonly cite the BLS’s CPI when discussing inflation, but that isn’t the only metric available. The BLS also produces a Chained Consumer Price Index—an effort to be “a closer approximation to a cost-of-living index than other CPI measures.” The BEA tracks prices via its personal consumption expenditures (PCE) price index. To varying degrees, both measures show a slower rate of rising prices than CPI. Folks can argue about which is most accurate to measure broad inflation, but none is more “right” than the other. This is especially true when trying to measure one’s cost of living, which will vary depending on one’s personal situation. And even if you assume all growth rates are accurate, inflation isn’t necessarily eating away at one’s wages. Employee earnings typically exceed expenses, and a smaller growth rate off a higher pay base can easily result in a bigger dollar increase than a slightly larger growth rate off a much lower base.

Finally, we caution against assuming inflation is only headed higher from here on out. Broadly speaking, inflation is a monetary phenomenon. With a flatter yield curve likely tamping down a bit on banks’ willingness to lend, money supply growth doesn’t look likely to meaningfully accelerate for the foreseeable future—suggesting inflation shouldn’t gallop higher. Amid benign inflation and solid economic drivers, US growth doesn’t look like it’ll end any time soon. That remains true even if one measure of average wages continues to lag the change in one measure of a broad basket of goods and services prices.

[i] Source: “Rising U.S. Consumer Prices Are Eroding Wage Gains,” Josh Mitchell, The Wall Street Journal, 8/10/2018. https://www.wsj.com/articles/u-s-consumer-prices-rose-0-2-in-july-1533904402?mod=hp_lead_pos9

[ii] Source: “In U.S., Wage Growth Is Being Wiped Out Entirely by Inflation,” Heather Long, Washington Post, 8/10/2018. https://www.washingtonpost.com/business/2018/08/10/america-wage-growth-is-getting-wiped-out-entirely-by-inflation/?utm_term=.dda14fedf8ef

[iii] Except for those younger workers themselves.

If you would like to contact the editors responsible for this article, please message MarketMinder directly.

*The content contained in this article represents only the opinions and viewpoints of the Fisher Investments editorial staff.

Get a weekly roundup of our market insights

Sign up for our weekly e-mail newsletter.

You Imagine Your Future. We Help You Get There.

Are you ready to start your journey to a better financial future?

Where Might the Market Go Next?

Confidently tackle the market’s ups and downs with independent research and analysis that tells you where we think stocks are headed—and why.

Related Resources

-

Market Analysis Beyond Iran: A Non-Conflict March Mailbag Q&A2026-03-30

-

Weekly Wrap-Up Fisher Investments Reviews: Last Week in Markets—March 23 - March 272026-03-30

-

Expert Commentary US Jobs, Eurozone Inflation, Private Credit | 3 Things You Need to Know This Week

2026-03-30

2026-03-30 -

Expert Commentary This Week in Review | Iran Conflict Volatility, March PMIs, Gold’s Recent Sell-Off

2026-03-27

2026-03-27

Learn More

Learn why 195,000 clients trust us to manage their money and how Fisher Investments and its affiliates may be able to help you achieve your financial goals.

As of 12/31/2025

New to Fisher? Call Us.

Contact Us Today